Stock ledger requirements in Connecticut (CBCA-CT)

What a Connecticut corporation must know about stock ledger requirements under Connecticut Business Corporation Act, C.G.S. § 33-600 et seq..

| C.G.S. § 33-945 | Records of shareholders |

|---|---|

| C.G.S. § 33-946 | Inspection rights |

| C.G.S. § 33-679 | Stock ledger entries |

| C.G.S. § 33-947 | Court enforcement |

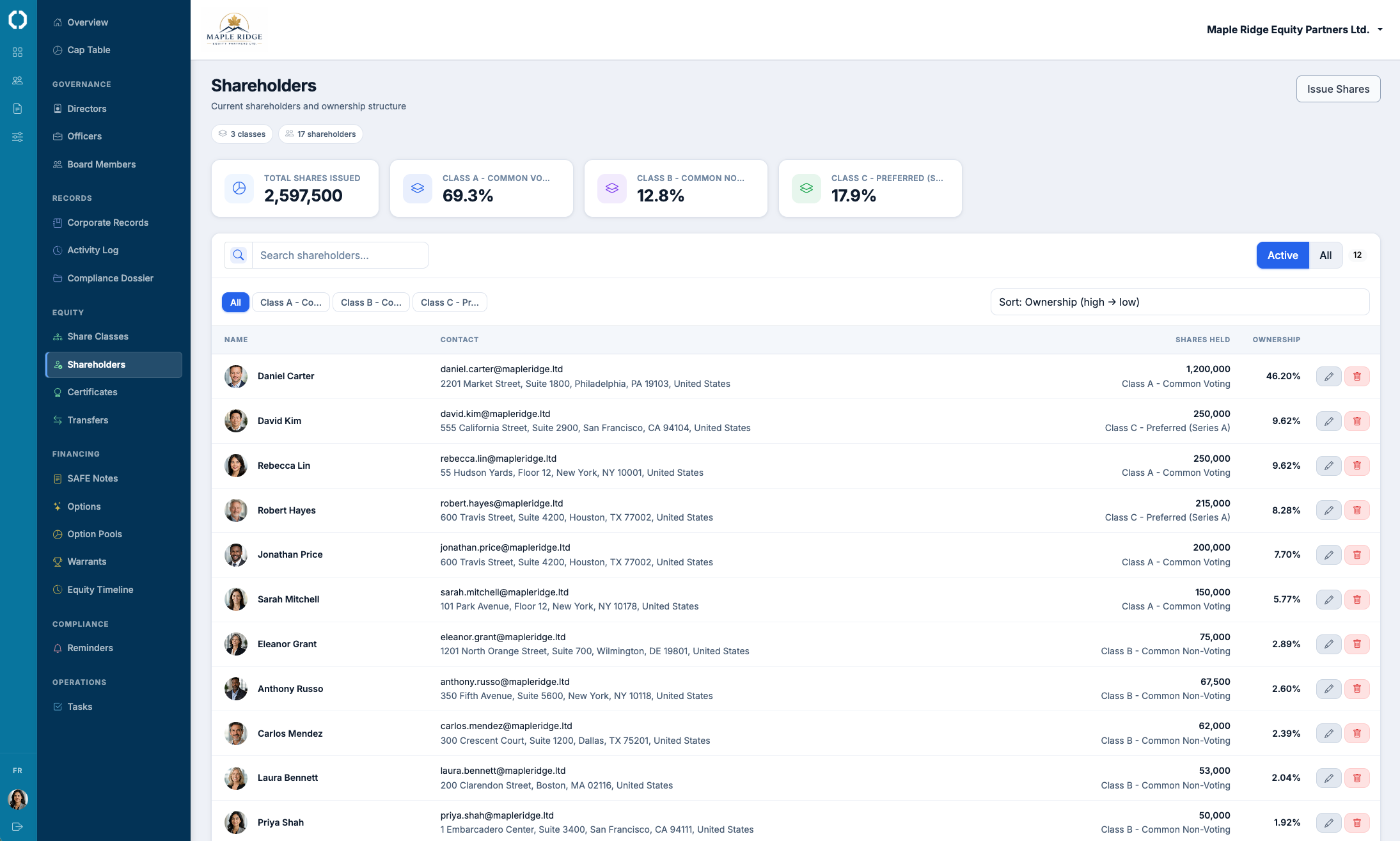

- Records each shareholder's name, address, number and class of shares, and date acquired

- Maintained at the principal office; electronic form permitted

- Inspection rights granted to shareholders under state-specific 'proper purpose' standards

- Transfers, issuances, and cancellations recorded chronologically

- Legal source of truth on ownership; the cap table is the operational analytical view

What the CBCA-CT requires

Connecticut General Statutes § 33-945 requires every Connecticut corporation to maintain a record of shareholders.

- Shareholder name and address

- Number and class of shares held

- Date each shareholder became a holder

- Certificate numbers and dates

- Complete transfer history

Difference from the cap table

The stock ledger is the statutory document — the legal source of truth on ownership. The cap table is the operational analytical view that models current and fully-diluted ownership. When they diverge, it is almost always the cap table that has drifted.

Inspection rights

Shareholders have a statutory right to inspect the stock ledger. The exact standard varies by state but generally requires a 'proper purpose' demonstration.

In Octelligence, every issuance, transfer, and cancellation updates both the statutory stock ledger and the cap table simultaneously.

See Digital Corporate RecordsIssuances, transfers, cancellations recorded in real time. Cap table synchronized.