How to transfer shares in Ohio

A share transfer is mechanically simple but procedurally easy to get wrong. Under Ohio Revised Code Chapter 1701, the procedure follows the universal pattern with the jurisdictional specifics noted below.

| Statute | Ohio Revised Code Chapter 1701 |

|---|---|

| Short citation | ORC Ch. 1701 |

| Relevant sections | state corporation statute (transfer and restriction provisions) |

| Registry | Ohio Secretary of State |

- Transfers are effective against the corporation only when the register is updated

- Most private corporations have transfer restrictions in the bylaws or shareholders' agreement (ROFR, board approval, prohibition on transfers to competitors)

- The old certificate is cancelled and stapled into the minute book; a new certificate issues to the transferee

- Transfers may trigger tax filings (TD F 90-22.1, T2057, etc.) depending on the parties and the structure

- Informal transfers (between shareholders without involving the corporation) corrupt the record and surface in diligence

In Ohio

In Ohio, the procedure to transfer shares operates under Ohio Revised Code Chapter 1701. The substantive steps mirror the universal pattern, with the applicable provisions found in state corporation statute (transfer and restriction provisions). The Ohio Secretary of State is the primary public-record destination for any filings flowing from the procedure. Diligence counsel will reconcile the corporation's internal records against the public record at Ohio Secretary of State as part of the standard review.

Steps

Check the transfer restrictions

Before any transfer, the transferor checks the corporation's bylaws and any shareholders' agreement for transfer restrictions. The most common are: right of first refusal (the corporation or other shareholders have a right to buy the shares at the proposed price before an outside transfer), board approval requirement, prohibition on transfers to competitors, and permitted-transferee carve-outs (transfers to family trusts, holdcos, or estate planning vehicles may be exempt). If a restriction applies, it must be satisfied (or waived in writing) before the transfer.Execute the transfer instrument

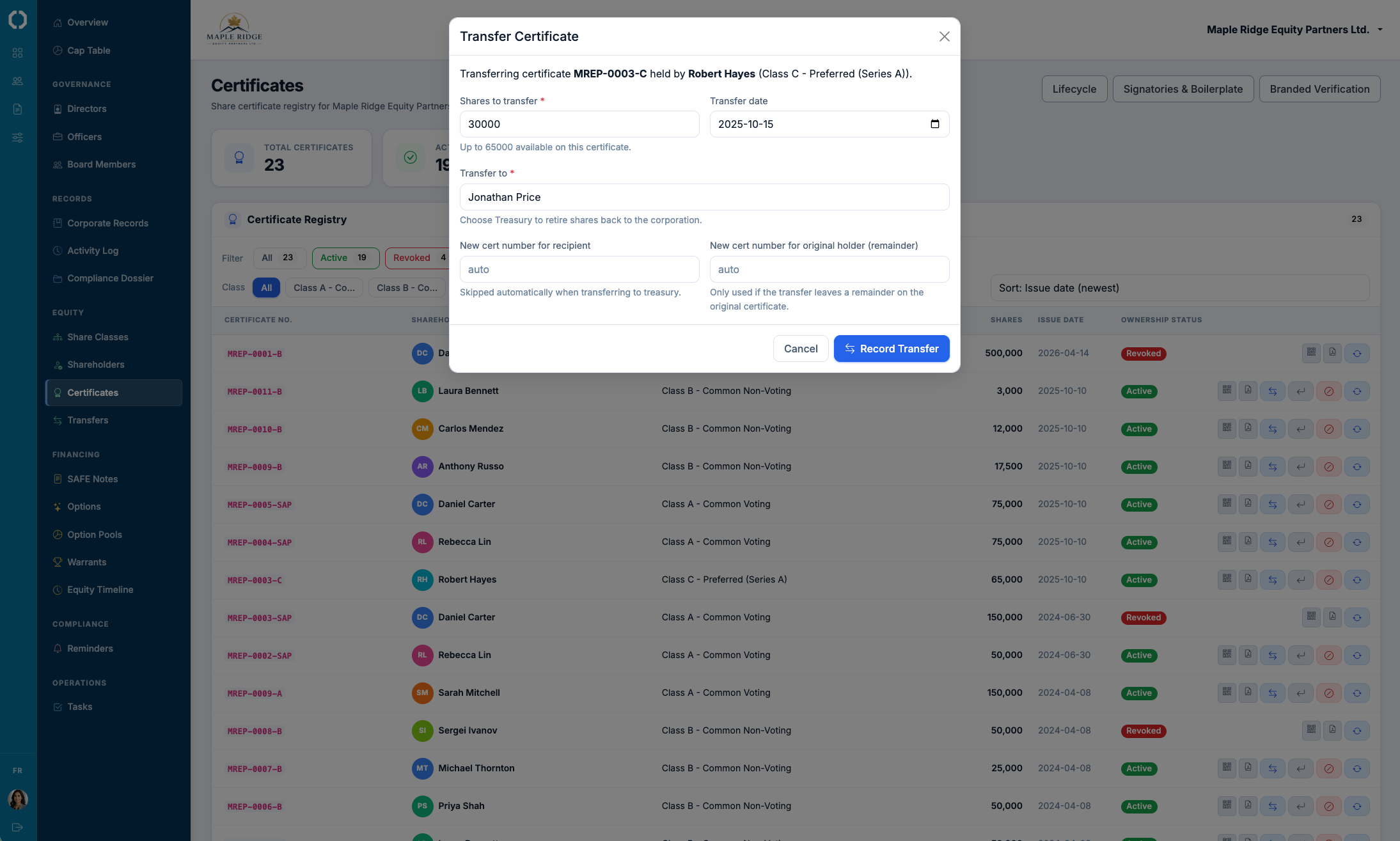

The transferor and transferee execute a stock power (US convention) or share transfer form (Canadian and UK convention). The instrument identifies the certificate being transferred, the share count and class, the transferor and transferee, and the consideration. The transferor's signature must be guaranteed (medallion signature guarantee in the US, witnessed signature in Canada and the UK). The transferee signs to acknowledge receipt and any continuing obligations under the shareholders' agreement.Obtain board approval if required

If the bylaws or shareholders' agreement require board approval of the transfer, the board passes a resolution approving it. The resolution identifies the transferor, the transferee, the share count, and the consideration. The resolution may also waive any right of first refusal held by the corporation. Unanimous written consent is the practical substitute for a meeting. If approval is denied, the transfer cannot be registered.Cancel the old certificate

The transferor's original certificate is delivered to the corporation. The corporation marks the certificate cancelled (with a stamp, perforation, or written annotation), records the cancellation date, and retains the certificate. Stapling the cancelled certificate into the minute book at the corresponding register entry is the standard practice for paper-based records. For uncertificated shares, the cancellation is a register-level update with no physical document to retain.Issue the new certificate to the transferee

A new certificate is issued in the transferee's name, with a new sequential certificate number, the same class and count of shares, and the signatures of the officers permitted to sign under the bylaws. The new certificate may bear restriction legends if the shareholders' agreement requires them. If the transferee elects uncertificated form (where permitted), the issuance is recorded in the register but no physical certificate is produced.Update the share register

The share register records the transfer on the transfer date: cancellation of the prior certificate number and issuance of the new certificate number, with the transferor and transferee names, the share count and class, and the consideration. Both register entries (cancellation and issuance) share the same date, which is the date the corporation registers the transfer. The cap table regenerates from the updated register.File the transfer instrument and supporting documents

The executed stock power, the board resolution approving the transfer (if applicable), the cancelled certificate (or uncertificated cancellation record), and the new certificate copy all go into the minute book in chronological order. If beneficial ownership changes triggered by the transfer require an ISC, PSC, or FinCEN BOI update, those filings are completed in parallel.

Common mistakes

- Transfer registered without checking the shareholders' agreement. The transfer goes through, but the shareholders' agreement has a right-of-first-refusal that wasn't honoured. The other shareholders' claim surfaces in diligence and may force a rescission.

- Old certificate not cancelled. The corporation issues a new certificate but doesn't cancel the old one. The transferor's original is still in circulation, creating the possibility of a double transfer or fraudulent presentation.

- Transfer agreed but never registered. The transferor and transferee execute the transfer and exchange consideration, but the corporation is never notified. The register still shows the old shareholder. The transferee has no rights against the corporation, and the corporation continues to send distributions and notices to the wrong person.

- Stock power signed without medallion guarantee. An institutional transferor's stock power is signed but lacks the medallion signature guarantee. The transfer cannot be processed and the closing is delayed.

- Beneficial-ownership filings not updated. The transfer changes who has significant control of the corporation, but the ISC register, PSC register, or FinCEN BOI report isn't updated. The filings become out of date, which is itself a compliance failure.

Octelligence runs share transfers as a single workflow: transfer-restriction check, stock power generation, board approval (if required), certificate cancellation, new certificate issuance with verifiable QR link, and register update. The minute book entries are produced automatically and the cap table refreshes from the register.

See Cap Tables & FinancingCommon questions

Restriction checks, cancellation of the old certificate, sequential issuance of the new, and a register that always reflects current ownership.