How to maintain a minute book in Ontario

OBCA's records regime closely tracks the CBCA but with Ontario-specific features: the transparency register under s. 140.2 (since January 2023) replaces the CBCA ISC equivalent for OBCA corporations, with Ontario-specific definitions and reporting. Records are kept at the registered office or another Ontario-authorized location.

| Statutory records | Corporate records (registered office) |

|---|---|

| Inspection right | Broad inspection right under s. 145; similar to CBCA |

| Retention period | 6 years after dissolution (CBCA-pattern) |

| OBCA s. 140 | Corporate records: location and contents |

| OBCA s. 140.2 | Transparency register (Individuals with Significant Control) since January 2023 |

| OBCA s. 141 | Securities register |

| OBCA s. 145 | Inspection rights |

| OBCA s. 159 | Form of records |

| OBCA s. 244 | Retention of records after dissolution |

- OBCA s. 140 prescribes records inventory and location (registered office in Ontario or authorized location)

- OBCA s. 145 broad inspection right (similar to CBCA s. 21)

- OBCA s. 140.2 transparency register since January 2023: similar to CBCA ISC

- 6-year retention after dissolution (CBCA-pattern)

- OBCA s. 159 permits records in any form including digital

Records inventory and location under OBCA s. 140

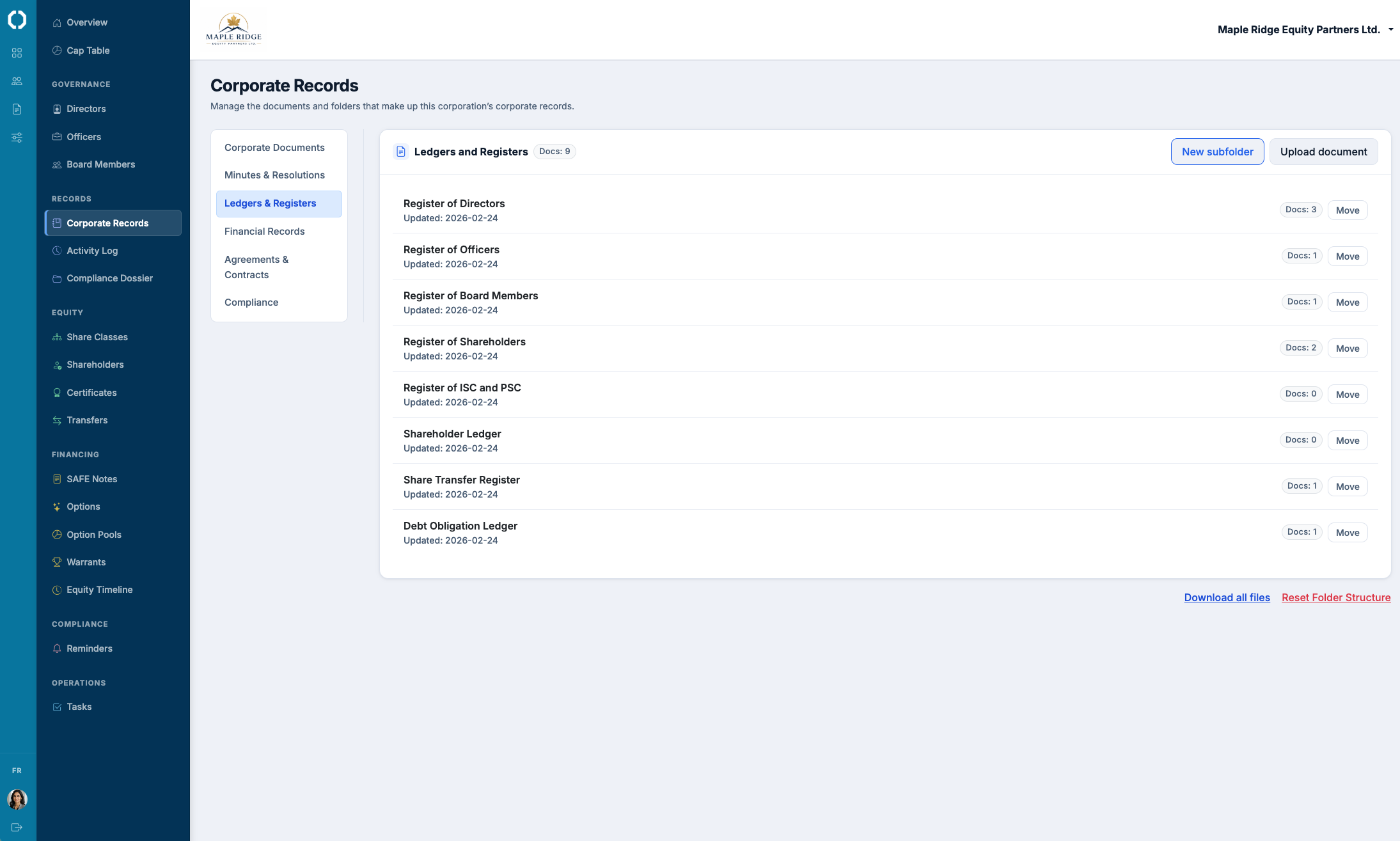

OBCA s. 140 requires every Ontario corporation to maintain at its registered office in Ontario (or another Ontario location authorized by the directors): articles, bylaws and amendments, unanimous shareholder agreements, minutes of shareholder meetings and shareholder resolutions, the securities register (s. 141), and the transparency register (s. 140.2). Subsidiary records (board minutes, accounting records) are also required.

Inspection rights under OBCA s. 145

OBCA s. 145 grants broad inspection rights similar to CBCA s. 21. The inspection right extends to securityholders, creditors, and (in some circumstances) other interested persons. No proper-purpose requirement equivalent to DGCL § 220.

Transparency register under s. 140.2 (since January 2023)

OBCA s. 140.2, effective January 1, 2023, requires every Ontario private corporation to maintain a transparency register of Individuals with Significant Control. The Ontario register tracks the CBCA ISC requirement (s. 21.1) but with Ontario-specific definitions and filing channels. The transparency register is internal; certain information is filed with the Ontario Business Registry through the corporate annual return.

Form of records under s. 159 and 6-year retention

OBCA s. 159 permits records in any form including digital. Retention after dissolution: 6 years (CBCA-pattern), under provisions tracking CBCA s. 226. The retention obligation falls on directors and officers at dissolution.

Records location: Ontario requirement

Unlike the CBCA (which permits another location anywhere in Canada authorized by directors), OBCA requires records to be kept at the registered office in Ontario or at another Ontario location. Records may not be primarily located outside Ontario without specific director authorization, though copies may be replicated elsewhere.

Procedure

The minute book maintenance routine as it applies in Ontario, in seven steps:

Establish records at the Ontario registered office under OBCA s. 140

At incorporation, establish records at the registered office in Ontario or at another Ontario location authorized by the directors. Records inventory: articles, bylaws, USA, shareholder minutes and resolutions, securities register (s. 141), and transparency register (s. 140.2).Maintain the securities register and transparency register together

Securities register lists securityholders. Transparency register (since January 2023) lists Individuals with Significant Control. Update both on ownership changes.Record corporate actions on the date of the action

Board and shareholder actions on the date they occur.Respond to s. 145 inspection demands

Broad inspection regime, similar to CBCA. No proper-purpose requirement.Maintain the transparency register under s. 140.2 and file with the Ontario Business Registry

Update the transparency register within statutory windows. Certain information is filed with the Ontario Business Registry through the corporate annual return.File the Ontario corporate annual return

Since 2022, the Ontario corporate annual return is filed through the Ontario corporate tax return process (not as a separate filing).Retain records 6 years after dissolution

OBCA-pattern retention, tracking CBCA s. 226.

Common mistakes

Common OBCA failure points in maintaining corporate records:

- Not maintaining the s. 140.2 transparency register since January 2023

- Keeping primary records outside Ontario without director authorization

- Refusing s. 145 inspection on proper-purpose grounds (OBCA does not require proper purpose)

- Not retaining records for the 6-year post-dissolution period

Octelligence keeps the minute book, the share register, the certificates, and the cap table in one record. Every resolution, meeting, issuance, and transfer is dated, indexed, and linked to its supporting documents. The OBCA inspection right, the retention period, and the beneficial-ownership register requirement are jurisdiction-aware. Diligence can reproduce the corporate record at any past date.

See Digital Corporate RecordsCommon questions in Ontario

Octelligence keeps the minute book, the share register, and the cap table reconciled together with full OBCA awareness of inspection rights and retention periods.