How to maintain a minute book

The minute book is the corporation's statutory record of its constitutional and governance acts. Every board action, every shareholder meeting, every share issuance, every articles amendment leaves a trace there, indexed and dated. Maintaining it is the discipline of entering each event when it happens and reconciling the records to one another on a regular cadence.

| When | On every board action, shareholder action, issuance, transfer, or filing |

|---|---|

| Who maintains | The corporate secretary or person acting in that role |

| Statutory anchor | CBCA s. 20, DGCL § 224, Companies Act 2006 Part 21 |

| Retention | For the life of the corporation plus the statutory post-dissolution period |

- The minute book is the index of every constitutional and governance act of the corporation

- Each entry is dated on the date of the action and signed by the corporate secretary

- Standard sections: incorporating documents, shareholders, directors, meetings, resolutions, filings

- Digital minute books are permitted everywhere; the substantive obligations are the same

- Inspection rights vary by jurisdiction; the records must be producible on valid request

On this page

Steps

Set up the minute book at incorporation

At incorporation, the minute book is established as the central repository of the corporation's statutory records. The opening contents are the certified articles of incorporation, the bylaws as adopted by the initial directors, the organizing resolutions of the first directors, the consent to act as a director from each first director, the initial registered office address, and the initial share issuances to founders with the supporting subscription documents. Each section is indexed.Maintain the standard sections of the minute book

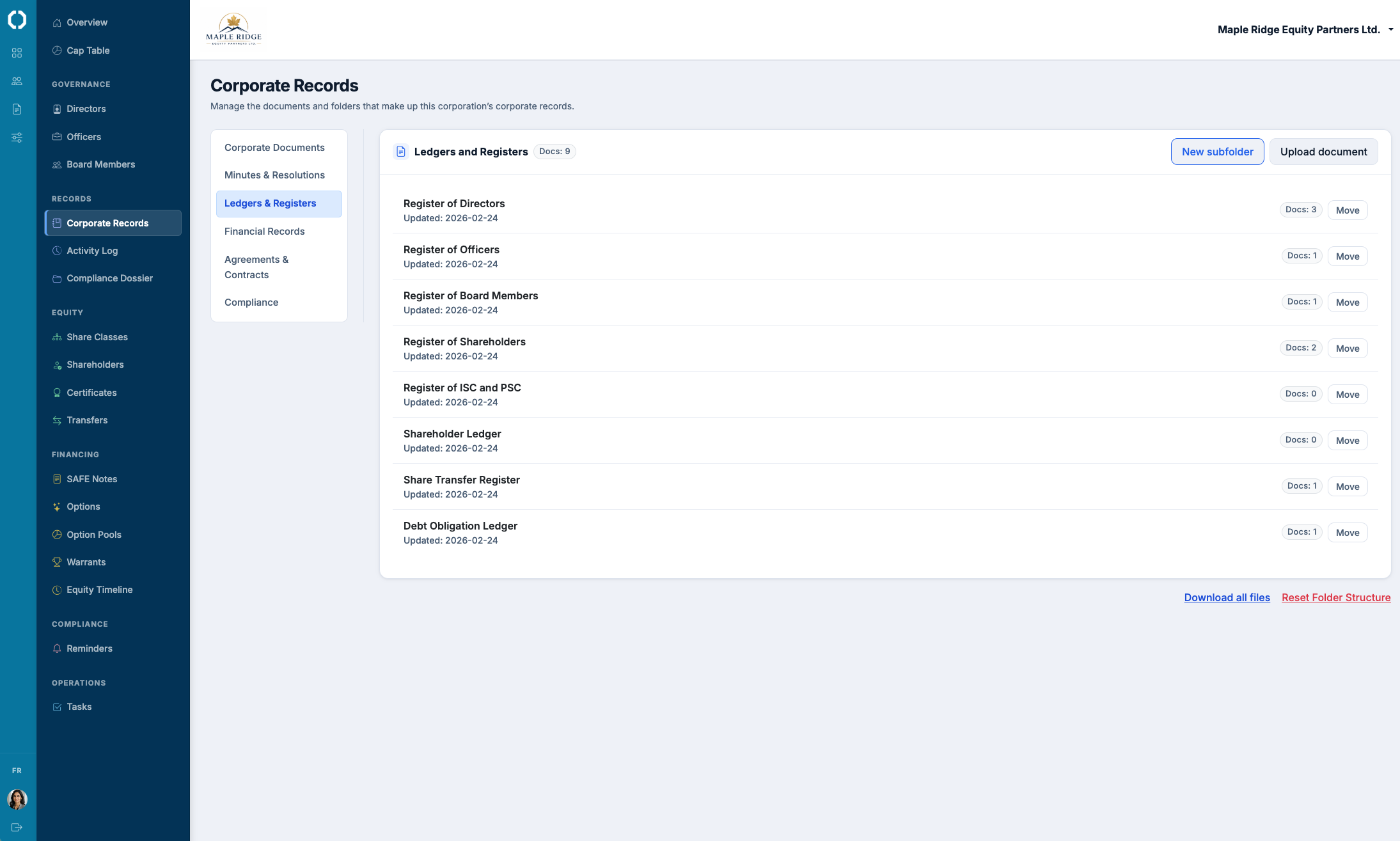

The minute book is organized into the standard sections: incorporating documents (articles, bylaws, amendments), shareholder records (share register, certificates, transfers, beneficial ownership register), director records (consents, resignations, elections), meeting records (minutes of director and shareholder meetings, notices, proxies, scrutineer reports), resolutions (board resolutions and shareholder resolutions, separately indexed), and statutory filings (annual returns, articles of amendment, registrar acknowledgments). Each section has an internal index.Record every corporate action on the date of the action

Each corporate action (board meeting, shareholder meeting, written resolution, share issuance, transfer, redemption, articles amendment, director change, registered-office change) is recorded in the minute book on the date the action occurs. The minutes or resolution are signed and dated, indexed in the relevant section, and linked to the underlying supporting documents (subscription agreement, certificate, filing acknowledgment). Backdated entries are not permitted.Reconcile the minute book to the share register and cap table monthly or quarterly

At a monthly or quarterly cadence, the share register (in the minute book) is reconciled to the cap table and to the physical certificates. Every share certificate must have a register entry with the same date, class, and share count. Every board resolution authorizing an issuance must trace to a register entry. The reconciliation is documented and signed by the corporate secretary so that the reconciliation date is verifiable.Update the registered office address and the inspection-ready format

The minute book is kept at the corporation's registered office (or another location authorized by the board) and is available for inspection by the directors, the shareholders, and (in some jurisdictions) creditors and the public registrar. The format is whatever the statute permits, including digital, provided the records are accurate, complete, and accessible. A change of registered office triggers a filing to the registrar and a corresponding minute-book entry.Maintain the beneficial-ownership and significant-control registers alongside the minute book

Where the jurisdiction requires it, the corporation maintains a register of beneficial owners or significant controllers (ISC register under CBCA s. 21.1, transparency register under OBCA s. 140.2, PSC register under Companies Act 2006 Part 21A, federal beneficial-owner reporting under the US Corporate Transparency Act). The register is updated on every change of beneficial ownership and is kept with the minute book (or at the registered office where statute permits).Produce the minute book on inspection or diligence

On inspection by an authorized person (a director, a shareholder under the statutory inspection right, the registrar, a diligence team in a financing or acquisition), the minute book is produced. The book is the foundational evidence of every corporate action: a missing minute is unverifiable, an unsigned resolution is unconfirmed, and an out-of-order entry is challengeable. Diligence runs from the minute book back to the share register, the cap table, the financial records, and the registry filings. See how to prepare for due diligence.

Jurisdiction notes

Minute-book obligations are similar across jurisdictions; the inspection right and the form requirements vary:

- Delaware (DGCL). Records required under DGCL § 224 (any form, convertible to clearly legible written form). Inspection under § 220 requires the shareholder to demonstrate proper purpose. Beneficial-ownership reporting under the federal Corporate Transparency Act (FinCEN BOI). View jurisdiction guide

- California. Records required under California Corporations Code §§ 1500 and 1501. Inspection right is broad and does not require proper purpose. State-level beneficial-owner disclosure under SB-201. View jurisdiction guide

- Canada (CBCA). Records under CBCA s. 20 plus the ISC register under s. 21.1 (Individuals with Significant Control). Inspection right under s. 21 is broad and includes creditors. Retention six years after dissolution under s. 226. View jurisdiction guide

- Ontario (OBCA). Records under OBCA s. 140 plus the transparency register under s. 140.2. Inspection right similar to CBCA. View jurisdiction guide

- United Kingdom. Records required under Companies Act 2006 Part 21 (registers, minutes, resolutions). PSC register under Part 21A (People with Significant Control). Inspection right under s. 116 is broad and available to any person. View jurisdiction guide

Common mistakes

- "We'll catch up the minute book at year end." The corporation accumulates a year of board resolutions, share issuances, transfers, and meetings that aren't documented. The year-end "catch-up" reconstructs the records from memory, the certificates, and a few emails. Diligence detects the reconstruction immediately because the resolutions are formatted identically and signed in the same hand.

- Records spread across multiple locations. The articles are in counsel's filing cabinet. The minutes are in the founder's drive. The share register is in a spreadsheet on a different drive. The certificates are in a safe at the registered office. Producing the minute book on inspection requires coordinating four custodians, and no one is sure which document is current.

- No ISC, PSC, or BOI register. The corporation maintains a competent minute book but has not set up the beneficial-ownership register required by the jurisdiction. The general minute book is compliant; the specific transparency obligation is not. Penalties for non-compliance can be significant (CBCA fines up to $200,000 for the corporation and $200,000 for directors; UK criminal penalties under Part 21A).

- Signature pages without supporting documents. Resolutions are signed and filed in the minute book, but the supporting documents (the contract being approved, the certificate referred to in the resolution, the subscription agreement) are not retained with the resolution. The resolution is unactionable in diligence because the underlying instrument can't be confirmed.

- Unsigned, undated minutes. A meeting takes place, draft minutes circulate, but the minutes are never finalized and signed. The verbal record of the meeting (recollections of attendees) is the only record of what happened. The minutes are unverifiable for diligence.

Octelligence stores each resolution, meeting minute, register entry, and filing acknowledgment in its proper section on the date of the action, with cross-links to the underlying supporting documents. The reconciliation between the minute book, the share register, the cap table, and the registry filings is automatic, and the diligence export produces the entire book as a single, indexed PDF or live-link package.

See Digital Corporate RecordsCommon questions

The corporation's constitutional and governance acts kept in one place, reconciled between the minute book, share register, cap table, and registry on demand.