How to file an annual return

The annual return (called the confirmation statement in the UK, the annual report in many US states, and the annual return in CBCA and OBCA jurisdictions) is the corporate registry's snapshot of basic information about the corporation, filed each year. It is not a financial statement or a tax return. Missing it does not cause headlines, but missing it persistently leads to administrative dissolution and the loss of corporate status.

| When | Each year by the deadline set by the registrar (anniversary, year end, or review period) |

|---|---|

| Who files | The corporation, signed by a director or officer |

| Content | Name, directors, registered office, share structure (where required), beneficial ownership |

| Consequence of non-filing | Late fees, then administrative dissolution after extended non-compliance |

- The return is a registry filing, distinct from tax filings and statutory accounts

- Deadlines run from the anniversary date, the financial year end, or the review period

- Information filed is governance data: directors, registered office, share structure

- Late filing fees apply immediately; persistent non-filing causes administrative dissolution

- The acknowledgment is retained in the minute book under statutory filings

On this page

Steps

Confirm the corporation's anniversary date and filing deadline

The annual return is filed each year by reference to the corporation's anniversary date (the date the certificate of incorporation was issued) under most regimes, or by reference to the financial year end in others. Under the CBCA, the return is due within 60 days of the anniversary date (s. 263). Under the OBCA, due within six months of the financial year end. Under Companies Act 2006, the confirmation statement is due within 14 days of the review period end (s. 853A). Use the annual filing lookup to confirm the deadline for the corporation's jurisdiction.Reconcile the corporate record to the registrar's data

Before filing, the corporate secretary reconciles the corporation's records (directors, registered office, share structure, beneficial ownership) to the data the registrar holds. Changes that occurred during the year that should have been filed separately (a director change, a registered-office change, an articles amendment) are reviewed to confirm they were filed at the time and not deferred to the annual return.Prepare the return with the required information

The annual return reports the corporation's current information as at the filing date: corporate name and number, registered office, mailing address, directors (names, addresses, dates of appointment), officers in some jurisdictions, share structure (in Companies House filings), and beneficial ownership where the regime requires. The return is not a financial statement; it is the registry's snapshot of the corporation's basic registration data.File the return through the registrar's channel

The return is filed through the registrar's online portal in most jurisdictions (Corporations Canada Online Filing Centre for CBCA, ServiceOntario for OBCA, Companies House WebFiling or software filing for UK companies, the relevant Secretary of State for US states). Paper filing is accepted in many jurisdictions but increasingly uncommon. The filing fee is paid at the time of filing.Confirm acceptance and retain the acknowledgment

On acceptance, the registrar issues an acknowledgment or filing receipt. The acknowledgment is retained in the minute book under the statutory filings section. The corporation's filing history is updated in the public registry and (where the registry is integrated) flows through to corporate registry searches that third parties run during diligence. See how to maintain a minute book.Update internal calendars and reminder systems

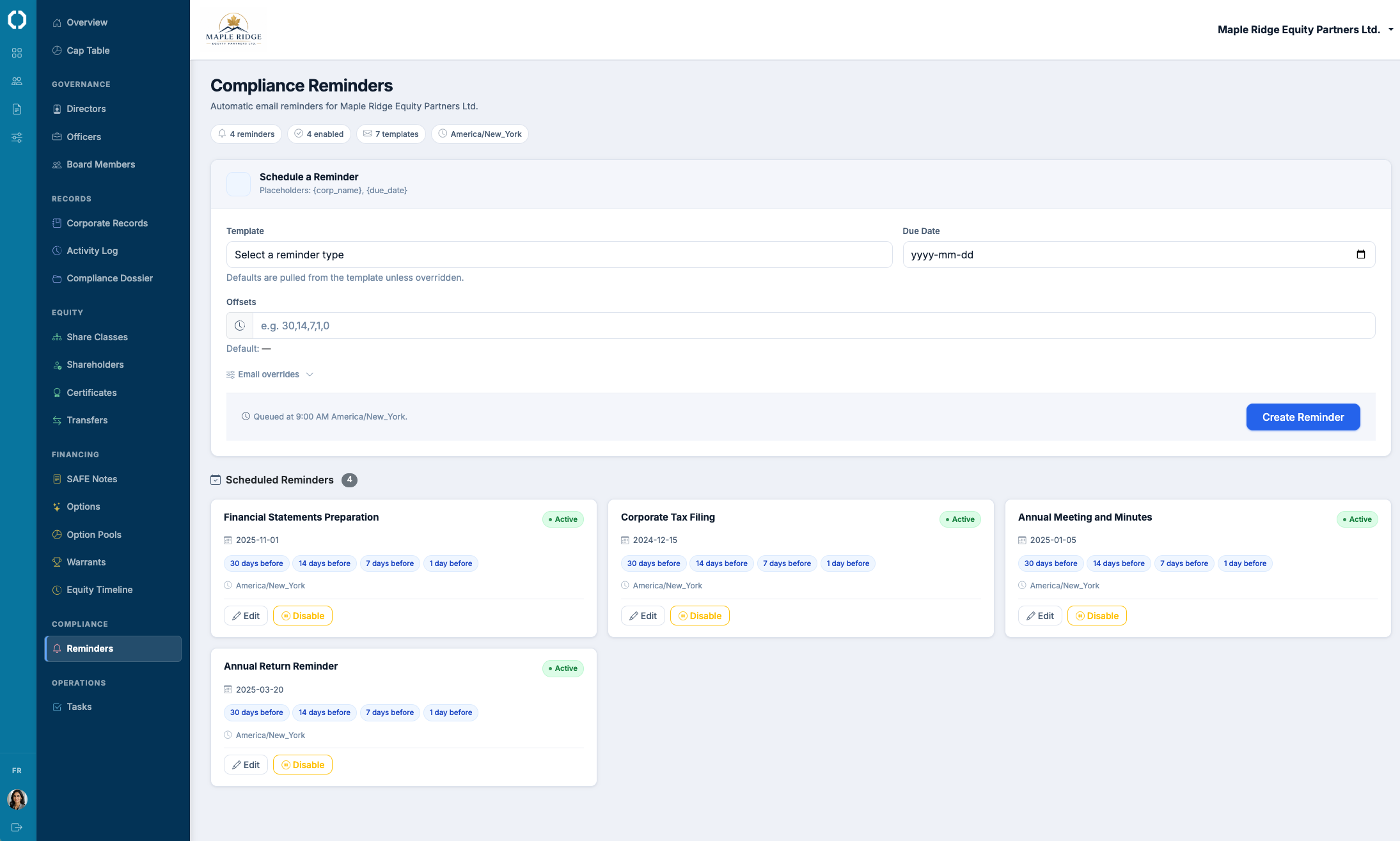

The next year's filing deadline is set in the corporation's annual compliance calendar. The reminder system (calendar, software, external corporate services provider) is verified to fire 30 to 60 days before the next deadline. Cumulative missed filings escalate quickly: a single missed annual return is a fix; multiple missed filings can lead to administrative dissolution and the loss of corporate status.Coordinate with other annual statutory filings

The annual return is distinct from the corporation's tax filings (T2 in Canada, Form 1120 in the US, CT600 in the UK), its employment-related filings (T4, W-2, P11D, P60), and its statutory financial statements where applicable. Coordinating the deadlines and the data sources prevents one filing from reporting information inconsistent with another. Most corporations consolidate the annual filings into a single calendar that runs each year on the same cadence.

Jurisdiction notes

The return content and deadline differ by jurisdiction; the procedural shape is consistent:

- Delaware (DGCL). Annual franchise tax report under DGCL § 502 due by March 1 each year. The report includes the names and addresses of directors and the corporation's authorized share count, and the franchise tax is calculated either by the authorized-shares method or the assumed-par-value method. Late filing penalty is $200 plus interest. View jurisdiction guide

- California. Statement of Information (Form SI-550) under California Corporations Code § 1502 due within 90 days of incorporation and annually thereafter. Filing fee $25. Failure to file may lead to suspension of corporate powers. Separate franchise-tax filing with the FTB by the 15th day of the third month following the year end. View jurisdiction guide

- Canada (CBCA). Annual return under CBCA s. 263 due within 60 days of the anniversary date. Filing fee $12 online. Includes corporate name, directors, registered office, and confirmation of compliance. Failure to file for one year may trigger administrative dissolution under s. 212. View jurisdiction guide

- Ontario (OBCA). Annual return integrated with the corporate tax return (filed through CRA) since 2022. Includes director information and registered office. Annual return filing for non-share-capital and certain other corporations through the Ontario Business Registry. View jurisdiction guide

- United Kingdom. Confirmation statement under Companies Act 2006 s. 853A due within 14 days of the review period end (each anniversary of incorporation or the last confirmation statement). Filing fee £13 online. Confirms registered office, directors, secretaries, SIC codes, share capital, shareholders, and PSC information. View jurisdiction guide

Common mistakes

- Confusing the annual return with the tax return. The corporation files the T2 or 1120 on time and assumes the annual return is covered. It isn't; the corporate-registry filing is separate from the tax filing in most jurisdictions, with different deadlines and different content.

- Using the annual return to make substantive changes. A director change is included in the annual return without filing the dedicated director-change form. The change is technically recorded in the registry data but is not properly dated and may not be effective for third-party reliance until the dedicated filing is made.

- No reminder system. The first annual return is filed manually on the anniversary. The reminder for the next year is never set. The deadline passes silently. Two years later, the corporation discovers it is in default and is now subject to late fees and potential administrative dissolution proceedings.

- Stale director addresses. A director moved three years ago. The corporation's annual returns since then have reported the old address. The registry data is out of sync with the corporation's actual records. Service of process on a director at the registered address fails.

- Filing fee unpaid. The online filing is submitted but the fee fails (expired card, declined payment). The corporation assumes the filing is complete because the form was submitted. The registrar treats the filing as not made until the fee clears.

Octelligence tracks every corporation's filing deadline, prepares the return from the corporation's existing record, files through the registrar's channel, retains the acknowledgment in the minute book, and sets the next year's reminder automatically. Portfolio law firms and accountants use the same workflow to file at scale across every corporation under their care.

See For Law Firms & AccountantsCommon questions

Deadline tracking, pre-filled returns from the corporate record, filing through the registrar's channel, acknowledgment retained in the minute book.