The complete guide to corporate minute books

A corporation does not really exist on paper until its minute book proves it. The book is the indexed, dated record of every constitutional and governance act a company takes, from the first organizing resolution to the last share transfer. This guide explains what a minute book is, what belongs inside, how the requirements differ across Canada, the United States, and the United Kingdom, why digital is now the norm, how to keep one current, and the specific ways minute books fail when a financing or acquisition puts them under scrutiny.

| What | The statutory record of a corporation's governance and ownership acts |

|---|---|

| Required by | CBCA s. 20, OBCA s. 140, DGCL § 224, Companies Act 2006 Part 21 |

| Begins | At incorporation, with the organizing documents and first resolutions |

| Retention | Life of the corporation, plus the statutory period after dissolution |

- The minute book is the corporation's primary evidence that its actions were validly authorized

- It is required by statute from the day of incorporation, not a year-end formality

- Standard sections cover incorporating documents, shareholders, directors, meetings, resolutions, and filings

- Requirements are similar across jurisdictions, but inspection rights and transparency registers differ

- Most diligence problems trace back to a minute book that was reconstructed after the fact

On this page

What a minute book is

A minute book is the official, organized record of a corporation's governance. It holds the documents that prove the corporation was properly formed and that every significant decision since formation was properly made: the articles of incorporation, the bylaws, the minutes of directors' and shareholders' meetings, the resolutions passed between meetings, the share register, and the registers of directors and officers. The term is historical. Corporations once kept these records in a literal bound book with tabbed sections. The legal substance has outlived the binding: today the same records are kept in any form the statute permits, including entirely digital systems.

The minute book is not marketing material or an internal wiki. It is the corporation's evidentiary backbone. When a court, an investor, an auditor, a lender, or a tax authority asks whether a given share was validly issued or whether a given director had authority to sign, the answer comes from the minute book. For a plain-language definition of the individual components, see the glossary entries for the minute book, the share register, and board resolutions.

Why the minute book matters

The minute book is the difference between a corporation that can prove its history and one that can only describe it. That distinction stays invisible for years and then becomes decisive in a single moment, usually when money or control is changing hands.

Financing and acquisitions. Diligence does not begin with the pitch deck. It begins with the corporate records. An investor's counsel will confirm that the company is in good standing, that each round of shares was authorized by the board and reflected in the register, that options were granted under a plan the board adopted, and that the people signing the deal are the directors and officers the records say they are. When the minute book confirms all of this quickly, the deal moves. When it does not, the gaps become representations the founders cannot make, conditions to closing, escrow holdbacks, or a lower price. Our guide on how to prepare for due diligence walks through exactly what a diligence team pulls from the book.

Disputes and liability. When shareholders disagree, when a director is removed, or when a transaction is challenged, the minute book is the contemporaneous record that decides whose account is correct. Decisions that were never minuted are difficult to defend, and resolutions that were never signed are difficult to rely on.

Compliance and standing. Annual returns, registered-office changes, and director changes all flow from and back into the minute book. A corporation that lets these lapse can lose its good standing or, in extreme cases, be dissolved by the registrar. The blog post on the cost of missed corporate filings covers what happens when the cadence breaks.

What goes inside the minute book

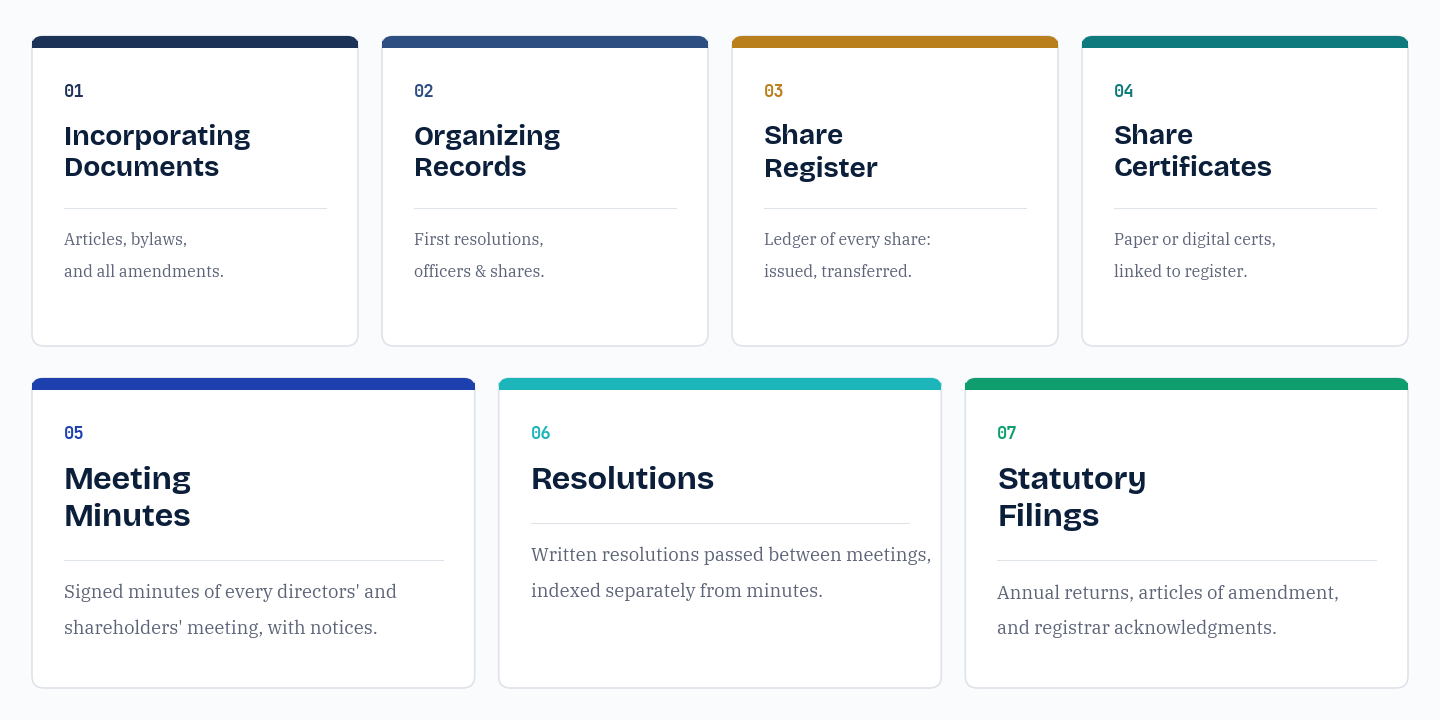

A complete minute book is organized into standard sections, each internally indexed. The exact tab names vary by template and jurisdiction, but the substance is consistent.

- Incorporating documents. The certified articles of incorporation (or certificate of incorporation), the bylaws as adopted, and every subsequent amendment to either. These define what the corporation is and what it is allowed to do.

- Organizing records. The first directors' organizing resolutions, the consents to act as director, the appointment of officers, the adoption of the bylaws, the banking resolution, and the initial issuance of shares to founders with the supporting subscription documents.

- Shareholder records. The share register, share certificates and their transfers, the securities register, and the beneficial ownership or significant-control register where required.

- Director and officer records. The register of directors and officers, with appointments, resignations, and elections, each dated.

- Meeting records. Minutes of directors' and shareholders' meetings, with notices, waivers, proxies, and scrutineer reports where relevant.

- Resolutions. Written resolutions of the board and of the shareholders passed between meetings, indexed separately from meeting minutes.

- Statutory filings. Annual returns, articles of amendment, and the registrar's acknowledgments, so the public record and the internal record agree.

Each entry should link to the instrument it refers to. A resolution authorizing a share issuance is only half a record without the subscription agreement, the certificate, and the matching register entry beside it. If you are assembling these from scratch, the bylaws template and the broader share issuance procedure are good starting points.

Minute book requirements by jurisdiction

The duty to keep a minute book is near universal across common-law corporate statutes. What changes between jurisdictions is the breadth of the shareholder inspection right, the specific transparency register required, and the retention period. The table below summarizes the anchors; each links to the full jurisdiction guide.

| Jurisdiction | Records anchor | Inspection right | Transparency register |

|---|---|---|---|

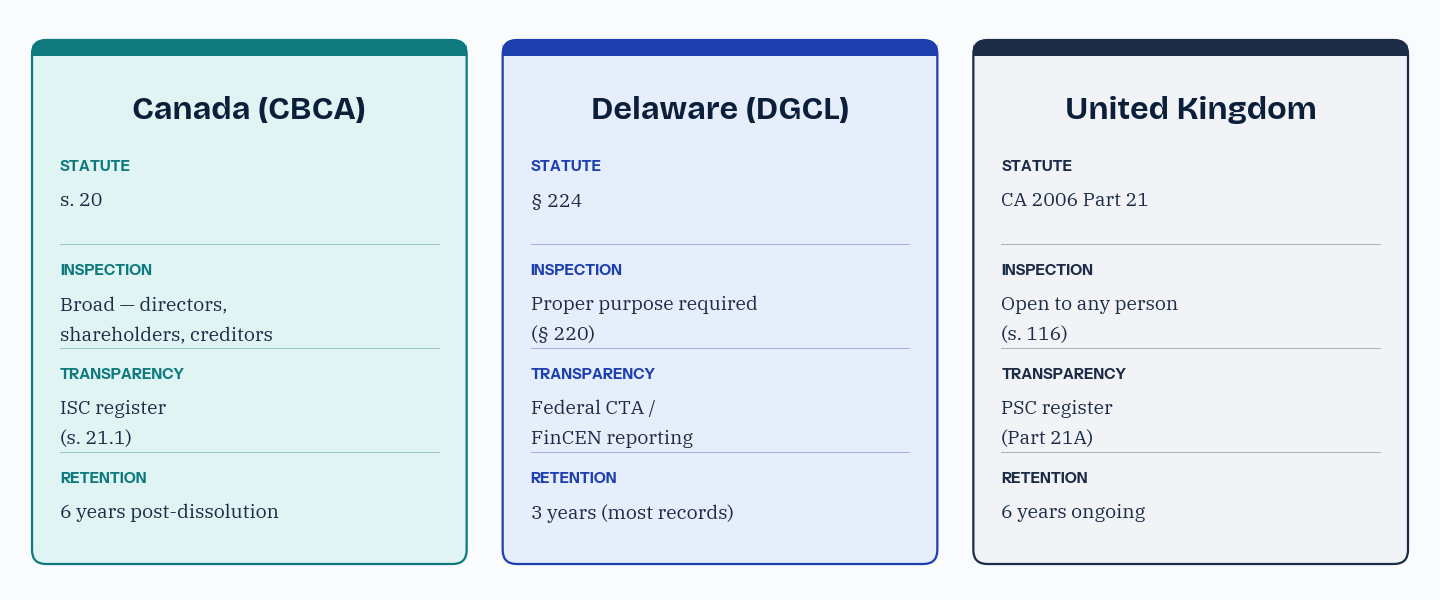

| Canada (CBCA) | s. 20 | Broad (s. 21), extends to creditors | ISC register (s. 21.1) |

| Ontario (OBCA) | s. 140 | Broad, similar to CBCA | Transparency register (s. 140.2) |

| British Columbia | BCBCA Part 3 | Members and the public, with limits | Transparency register |

| Delaware (DGCL) | § 224 | Proper purpose required (§ 220) | Federal CTA reporting (FinCEN) |

| California | Corp. Code §§ 1500, 1501 | Broad, no proper purpose needed | State and federal disclosure |

| United Kingdom | Companies Act 2006 Part 21 | Open to any person (s. 116) | PSC register (Part 21A) |

The practical lesson for cross-border groups is that one template does not satisfy every entity. A Delaware C-corp with a Canadian parent has to satisfy the DGCL for the subsidiary and the CBCA or a provincial statute for the parent, including the Canadian significant-control register that has no Delaware equivalent. Our cross-jurisdiction governance comparison goes deeper on these differences, and the full set of jurisdiction guides covers each one individually. For a focused comparison of the two regimes most Canadian founders deal with, see Delaware vs Canadian corporate records.

Beneficial ownership and significant-control registers

Over the last decade, transparency rules have added a register that sits alongside the traditional minute book: a record of the real human beings who ultimately own or control the corporation, not just the registered shareholders. The names differ by jurisdiction but the intent is the same.

- Canada (CBCA s. 21.1). The register of Individuals with Significant Control, listing those who own or control 25 percent or more of the shares, or who otherwise exercise significant influence.

- Ontario (OBCA s. 140.2) and other provinces. A transparency register on the same 25 percent threshold.

- United Kingdom (Companies Act 2006 Part 21A). The register of People with Significant Control, filed with Companies House.

- United States (Corporate Transparency Act). Beneficial ownership information reported to FinCEN, distinct from any state-level record.

This register is updated on every change of beneficial ownership and is part of the records the corporation must produce. A common failure, covered below, is a competent minute book with no significant-control register at all. For the underlying concept, see the glossary entry on the beneficial owner.

Paper versus digital minute books

Every modern corporation statute permits records to be kept in electronic form. The DGCL allows any form. The CBCA allows any form that can be converted to written form within a reasonable time. The Companies Act 2006 permits electronic records under s. 1135. The substantive obligations, accuracy, completeness, integrity, and the ability to produce the records on a valid inspection request, do not change with the format.

What changes is reliability. A paper book depends on a single physical copy held by one custodian, which is exactly the arrangement that produces gaps when that person is busy, leaves, or simply forgets. A digital system can timestamp each entry, cross-link a resolution to the certificate and register entry it refers to, and reconcile the register against the cap table automatically. The historical shift is worth understanding on its own terms; the blog post on the evolution of the corporate minute book traces it. The point for a guide like this is narrow: digital is permitted everywhere, and the real question is not paper versus digital but current versus reconstructed.

Setting up and maintaining the book

A minute book is set up at incorporation and maintained continuously after that. The discipline is simple to state and easy to neglect: record each corporate action on the date it happens, sign it, index it, and reconcile the records to one another on a regular cadence.

The setup populates the incorporating and organizing sections: the articles and bylaws, the first directors' resolutions, the consents to act, the officer appointments, and the founding share issuances. From there, every board meeting, shareholder meeting, written resolution, issuance, transfer, redemption, articles amendment, and director change is entered when it occurs, with the supporting documents attached. Backdated entries are not acceptable and are easy to detect.

The reconciliation is what keeps the book trustworthy. On a monthly or quarterly cadence, the share register is checked against the cap table and the issued certificates: every certificate has a matching register entry, and every authorizing resolution traces to an issuance. The step-by-step mechanics are in our procedure for how to maintain a minute book and the companion guide on maintaining a share register. Before any action requires it, you can baseline where you stand with the free Corporate Records Health Check.

How minute books fail in diligence

Minute books rarely fail because a corporation did something wrong. They fail because the right things were never written down at the time. The patterns are consistent.

- The year-end catch-up. A year of resolutions, issuances, and meetings is reconstructed from memory and a few emails just before a financing. Diligence detects it instantly, because a year of records is suddenly formatted identically and signed in one sitting.

- Records scattered across custodians. Articles with counsel, minutes on a founder's drive, the register in a spreadsheet, certificates in a drawer. No single source is authoritative and producing the book means coordinating four people.

- No significant-control register. A clean traditional minute book with no ISC, PSC, or beneficial ownership register. The general obligation is met; the specific transparency obligation is not, and the penalties are real.

- Resolutions without their instruments. A signed resolution approving a contract or an issuance, with the underlying contract, subscription, or certificate missing. The resolution cannot be relied on because the thing it approves cannot be confirmed.

- Unsigned, undated minutes. A meeting happened, drafts circulated, nothing was finalized. The only record of what was decided is recollection, which is not evidence.

The throughline is that a record created after the fact is worth far less than the same record created at the time. The blog posts on corporate records versus the minute book and what a corporate minute book actually is develop these cases further. To pressure-test a specific company, the Diligence Readiness Assessment walks the same checks an investor's counsel would run.

Retention and inspection rights

A corporation keeps its minute book for as long as it exists and for a statutory period after dissolution: six years under CBCA s. 226, generally three years for most records under the DGCL, and six years under the Companies Act 2006 for ongoing companies, with some records kept longer. The obligation runs from the date of the underlying action and, for the final period, from dissolution.

Inspection rights are broader than many founders expect. Directors can inspect at all times. Shareholders have a statutory right that is broad in Canada and the UK and conditioned on a proper purpose in Delaware under DGCL § 220. Creditors and, in some jurisdictions, the public can see parts of the record, and the registrar and the auditor can inspect for their statutory functions. The corporation can impose reasonable conditions such as notice and copying fees, but it cannot refuse a valid request. Records kept at a registered office, or at another board-authorized location, must be producible on reasonable notice regardless of whether they are paper or digital.

Minute book versus corporate records

The two terms are often used interchangeably, but they are not the same. The minute book is the governance core that the corporation statute specifically requires: articles, bylaws, minutes, resolutions, the share register, and the registers of directors and officers. Corporate records is the wider set that also includes financial statements, tax filings, material contracts, and employment records. Every minute book is part of the corporate records; not every corporate record belongs in the minute book. Keeping the distinction clear matters because the statutory duties, the inspection rights, and the retention rules attach specifically to the minute book, while the broader records are governed by tax, employment, and contract law. For a practical treatment of where the line sits, see corporate records or minute book.

Octelligence keeps each resolution, meeting minute, register entry, certificate, and filing acknowledgment in its proper section on the date it happens, cross-linked to the supporting documents. The minute book, the share register, the cap table, and the registry filings reconcile automatically, and a diligence export produces the entire book as one indexed package.

See Digital Corporate RecordsCommon questions

Keep the corporation's constitutional and governance acts in one place, reconciled between the minute book, share register, cap table, and registry on demand.