How to issue shares in a private corporation

Issuing shares is the single most consequential governance action a private corporation takes. Done correctly, it produces a clean record that ties the share register, the issued certificate, the authorizing resolution, and the cap table together at a single date. Done incorrectly, it leaves a gap that surfaces years later in diligence.

| When | Founding issuance, financing rounds, option exercises, conversion of SAFEs or notes |

|---|---|

| Who authorizes | Board of directors (or shareholders for certain class changes) |

| Documents produced | Authorizing resolution, subscription agreement, share certificate, register entry, cap-table update |

| Statutory anchor | Issuance is governed by the corporation statute (DGCL, CBCA, OBCA, etc.) and the corporation's own articles and bylaws |

- Authorization comes first: no shares are issued without a board resolution or written consent

- Consideration must be real, identified in the resolution, and received by the corporation before issuance

- Every issuance produces a certificate (or uncertificated record) tied to the share register at the same date

- The cap table updates from the register, never the other way around

- Founder issuances follow a distinct procedure with vesting and (in the US) an 83(b) election, see issue founder shares

On this page

Steps

Confirm authorized capital and class

Before any issuance, confirm that the corporation has authorized capital available in the class you intend to issue. Authorized capital is set in the articles. If the proposed issuance exceeds authorized capital, an amendment to the articles is required first, which is a shareholder action under most corporation statutes. Confirm the share class (common, preferred series, special) and that the rights attached to that class (voting, dividend, liquidation) align with what the subscriber expects.Pass an authorizing resolution

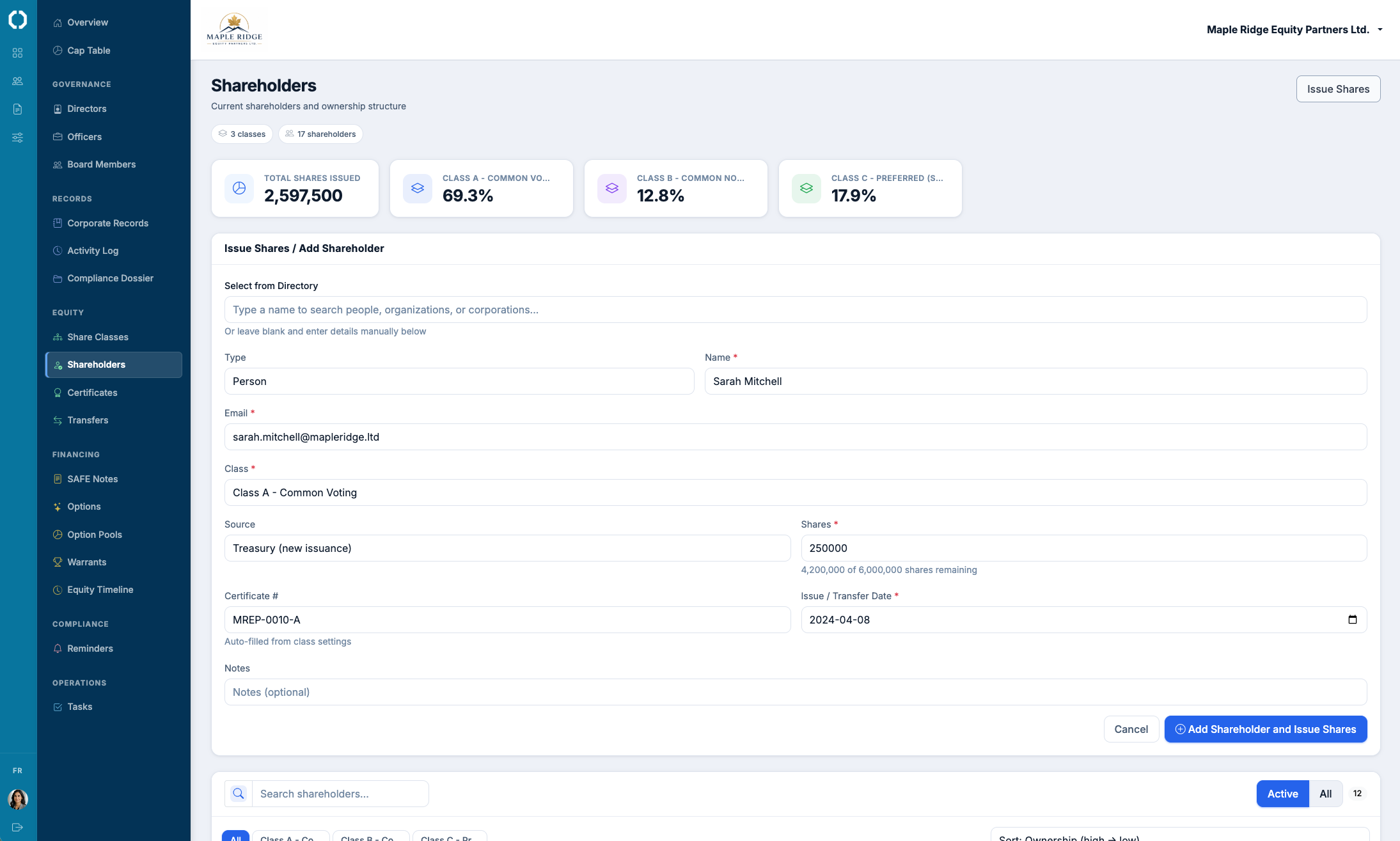

Issuance is authorized by the board of directors, almost always. The resolution must identify the subscriber, the class and number of shares, the consideration to be received, the conditions of issuance, and the effective date. In jurisdictions that permit it (and most do), unanimous written consent of the directors substitutes for a meeting. The resolution goes into the minute book immediately after execution. If the issuance triggers any preemptive rights, right of first refusal, or anti-dilution adjustment in an existing shareholders agreement, the resolution should reflect that those rights have been waived or addressed.Receive the consideration

Shares cannot be issued before consideration is received. Consideration may be cash, property, past services, or the conversion of an existing instrument (SAFE, convertible note, option exercise). For non-cash consideration, the resolution must identify the fair value and the basis for that valuation. For cash consideration, the funds must clear the corporation's account before the issuance date. The subscription agreement records the subscriber's acknowledgement of the consideration paid.Update the share register

The share register (called the stock ledger in the US) records the issuance: subscriber name, address, class, number of shares, certificate number, consideration, and issuance date. The register is the corporation's statutory record of issued shares. Every issuance must be entered in the register on the issuance date, with no gaps and no back-dating.Issue the certificate (or uncertificated record)

A share certificate is issued in the subscriber's name, bearing a sequential number, the share class and count, the corporation's name, and the signatures of the officers permitted to sign under the bylaws. In jurisdictions that permit uncertificated shares (most US states under DGCL § 158 and similar provisions), an uncertificated record may substitute for a paper certificate, with the same content. The certificate or uncertificated record traces back to the register entry by certificate number.Reconcile the cap table

The cap table updates from the share register, not in parallel to it. After the issuance is recorded in the register, the cap table is regenerated to reflect the new ownership percentages on both an issued-shares and a fully-diluted basis. The reconciliation date matches the issuance date. Any discrepancy between the register and the cap table is a sign that one or the other is wrong, and the register controls.File the resolution and supporting documents in the minute book

The authorizing resolution, the subscription agreement, the proof of consideration received (cleared cheque, bank confirmation, or equivalent), the issued certificate (or uncertificated record), and the updated register page all go into the minute book in chronological order. Diligence counsel will reconstruct the issuance from these documents; they must be complete.

Jurisdiction notes

The procedure above applies across all common-law corporation statutes. The jurisdictional differences are in the share-classification rules and the specific filings required:

- Delaware (DGCL). Issuance is governed by DGCL §§ 151-161. Stock ledger entry under § 219 and certificate issuance under § 158. Uncertificated shares are fully permitted. No public filing for the issuance itself. View jurisdiction guide

- California. Issuance under California Corporations Code §§ 400-422. Notice of Issuance of Securities (Form 25102(f)) is required for most private issuances, due within 15 days. View jurisdiction guide

- Canada (CBCA). Issuance under CBCA ss. 25 and 27. The corporation must maintain a securities register under s. 50. No public filing for the issuance, but any change in directors or shareholders may trigger a Form 6 (Notice of Change of Directors) filing. View jurisdiction guide

- Ontario (OBCA). Issuance under OBCA ss. 23 and 25. Securities register under s. 140. Director changes filed with the Ontario Business Registry. View jurisdiction guide

- United Kingdom. Allotment under Companies Act 2006, Part 17. SH01 (Return of allotment of shares) must be filed with Companies House within one month of the allotment, even though the allotment itself is internal. View jurisdiction guide

Common mistakes

- Issuance before the resolution. Shares are recorded in the register before the authorizing resolution is executed. The resolution is then drafted retroactively. In diligence, the date inconsistency reads as poor governance at best, and an unauthorized issuance at worst.

- Consideration not actually received. The resolution recites consideration that was never paid, or that was paid but cannot be evidenced. For founder issuances, a missing cleared cheque or transfer record is the most common version of this.

- Certificate issued without a register entry. A certificate exists in the subscriber's hand, but the register has no corresponding entry, or the entry shows different numbers. The certificate is the evidence; the register is the record. They must agree.

- Cap table maintained in parallel to the register. The cap table is updated independently when convenient, and the register lags behind. Over time the two drift apart. The cap table is then unverifiable because the underlying record (the register) is incomplete.

- Preemptive rights or ROFR ignored. An existing shareholders agreement gives current shareholders preemptive rights, but the issuance is closed without offering the shares to them. This creates a contractual breach that surfaces in diligence and may require unwinding the issuance.

Octelligence walks the issuance procedure: the resolution is drafted from the issuance details, the subscriber is added to the register, the certificate is issued with a verifiable QR link, and the cap table updates from the register automatically. The minute book entries are produced in chronological order, ready for diligence.

See Cap Tables & FinancingCommon questions

Live share register, certificates that verify against the register, board resolutions in the minute book, and a cap table that ties to the register every day.