Delaware vs Canadian corporate records

Most startup advice assumes Delaware. Most Canadian founders, and any company with a parent or subsidiary on the other side of the border, live in two regimes at once. Delaware's General Corporation Law and Canada's federal and provincial statutes both require a corporation to keep records, but they differ on what must be kept, who can see it, which beneficial-ownership register applies, and how long it all has to survive. This guide compares the two, then translates the differences into what they mean for cross-border structures.

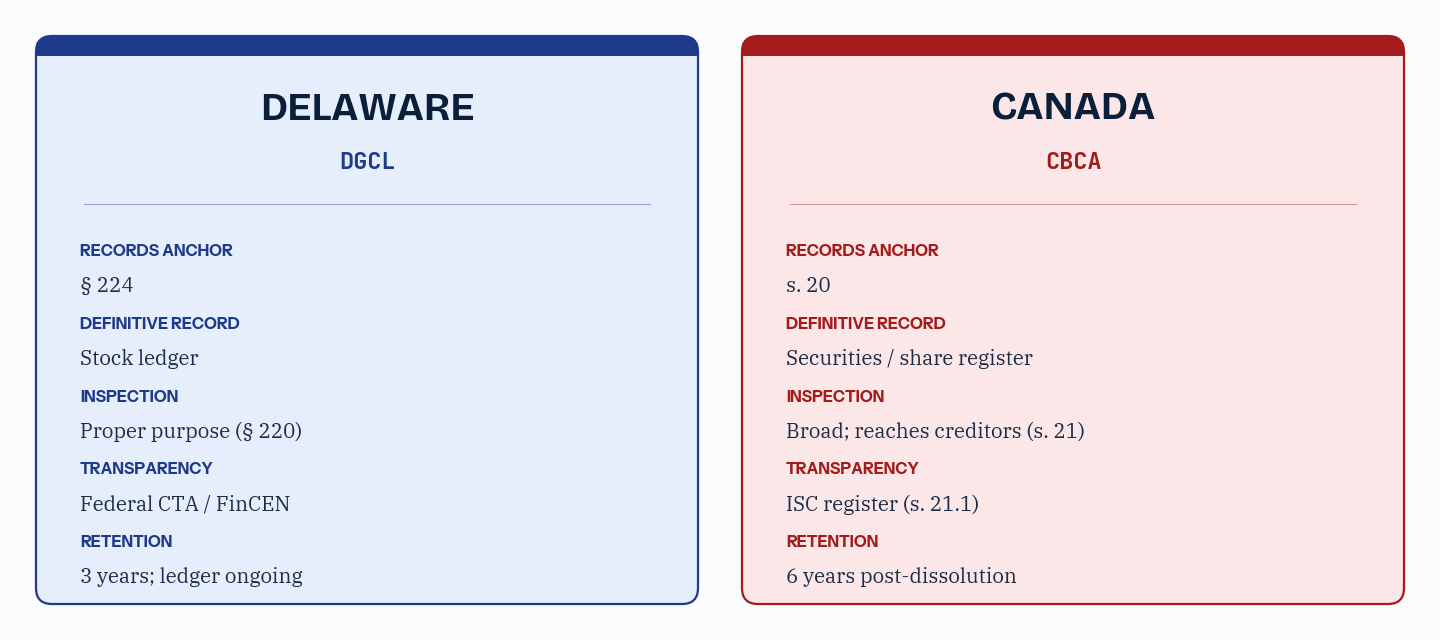

| US anchor | DGCL § 224 (records), § 220 (inspection) |

|---|---|

| Canada anchor | CBCA s. 20 (records), s. 21 (inspection), s. 21.1 (ISC register) |

| Biggest gaps | Inspection breadth, transparency registers, retention period |

| Cross-border rule | Each entity keeps its own records under its own statute |

- Both regimes require corporate records from incorporation; the obligation is not optional in either

- Delaware limits shareholder inspection to a stated proper purpose; Canada's right is broader and reaches creditors

- Canada requires a significant-control register; the US uses federal beneficial-ownership reporting instead

- Canadian retention (six years post-dissolution) is generally longer than Delaware's

- In a cross-border group, each entity keeps its own records under its own statute, no shared binder satisfies both

On this page

Why the comparison matters

Delaware is the default jurisdiction for venture-backed companies, and most playbooks, templates, and investor expectations are written for it. Canadian founders inherit a different reality. They incorporate federally under the Canada Business Corporations Act or provincially under a statute like the Ontario Business Corporations Act, they often hold assets through a holdco, and when they raise from US investors they frequently flip into a Delaware top-co with the original Canadian company surviving underneath. The result is that the same founder is responsible for two sets of corporate records under two regimes that look similar and differ in ways that surface at the worst possible moment.

Those differences are not academic. They decide whether a shareholder can demand to see your records, which beneficial-ownership register you must maintain, how long you must keep everything, and what a diligence team finds when it reviews a cross-border structure. Getting the comparison right early is far cheaper than reconstructing it during a financing.

The two regimes at a glance

Delaware corporations are governed by the Delaware General Corporation Law (DGCL). Canadian corporations are governed either federally by the CBCA or provincially by statutes such as the OBCA in Ontario or the BCBCA in British Columbia. The provincial statutes are close cousins of the CBCA, so the meaningful comparison is usually Delaware against the CBCA model, with provincial variations noted where they matter. For a dimension-by-dimension treatment beyond records, our cross-jurisdiction governance comparison sets the CBCA, the DGCL, and the UK Companies Act side by side.

The vocabulary differs too. What Canadians and the UK call a minute book, US practitioners usually call a corporate records book. The artifact is the same: the organized record of the corporation's constitutional and governance acts. Our complete guide to corporate minute books covers that artifact in depth; this guide focuses on where the two regimes diverge.

What records each requires

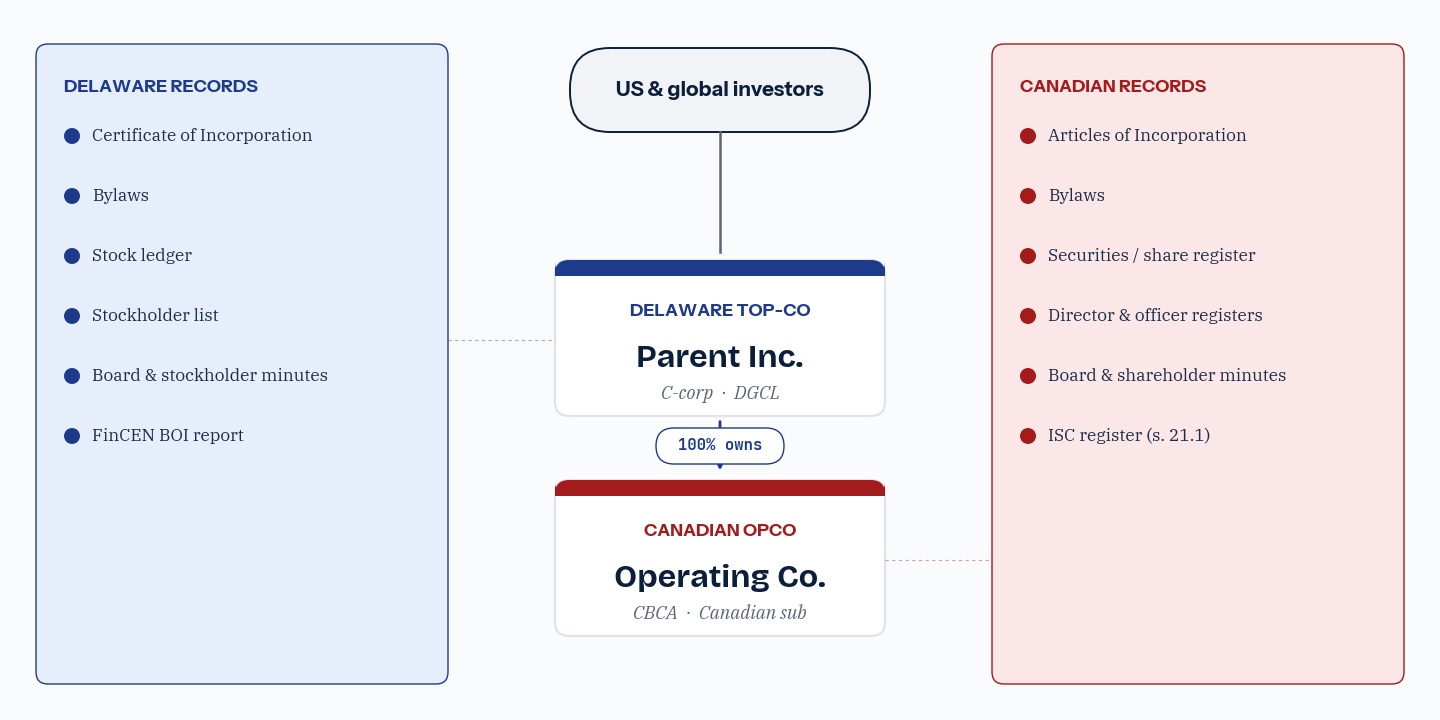

Delaware. DGCL § 224 permits records to be kept in any form, including electronic, provided they can be converted into clearly legible paper form within a reasonable time. The core records are the stock ledger (the definitive record of who owns the stock), the list of stockholders, and the books and records of account, alongside the certificate of incorporation, the bylaws, and the minutes of stockholder and director meetings. The stock ledger has special status in Delaware: it is the record that governs who may vote and who may inspect.

Canada. CBCA s. 20 requires the corporation to keep the articles and bylaws, minutes of meetings and resolutions of shareholders, the directors' register, the securities register (the Canadian equivalent of the stock ledger and the share register), and accounting records. Provincial statutes mirror this. Layered on top is the s. 21.1 register of Individuals with Significant Control, which has no direct Delaware analogue. The practical content of a Canadian minute book is therefore slightly broader than a Delaware records book, mainly because of the significant-control obligation.

Where the records are kept

Delaware corporations keep their registered office through a registered agent located in Delaware, but the books and records themselves may be kept elsewhere; the stockholder list and stock ledger must be available at the registered office or the principal place of business for inspection in connection with a meeting. Canadian corporations keep their records at the registered office or another place in Canada designated by the directors, and the records must be producible there on reasonable notice. For a digital records system, both regimes accept cloud storage as long as access can be provided from the required location. The jurisdiction-specific detail is in the Delaware and Canada (CBCA) records guides.

Who can inspect

This is the sharpest difference. Under DGCL § 220, a stockholder who wants to inspect the books and records must make a written demand stating a proper purpose, meaning a purpose reasonably related to their interest as a stockholder. If the company refuses, the dispute is decided by the Court of Chancery, and the stockholder bears the burden for records beyond the stock ledger and stockholder list. The proper-purpose requirement is a real gate.

Under CBCA s. 21, the inspection right is broader. Shareholders and creditors may examine the records during business hours and take extracts, and the right extends to the securities register without the proper-purpose hurdle that Delaware imposes. Provincial statutes are similar. For a cross-border group, this means a Canadian entity's records are more exposed to inspection than its Delaware sibling, which is worth knowing before a dispute arises.

Beneficial ownership registers

Both countries now require transparency about who really controls a corporation, but they do it differently.

- Canada. A CBCA corporation maintains a register of Individuals with Significant Control under s. 21.1, listing individuals who own or control 25 percent or more of the shares or who otherwise exercise significant influence. Provinces have parallel registers, such as the OBCA transparency register under s. 140.2. The corporation maintains the register, and federal CBCA corporations now also file the information with Corporations Canada.

- United States. Rather than a state-held register, the US uses federal beneficial-ownership reporting under the Corporate Transparency Act, filed with FinCEN. A Delaware corporation reports its beneficial owners to FinCEN; Delaware itself does not hold an equivalent state register in the corporate records.

The two obligations are independent. A FinCEN filing for the Delaware entity does not satisfy the Canadian significant-control register for the Canadian entity, and vice versa. Cross-border groups carry both.

Directors and residency

One difference that catches founders by surprise is director residency, because it shapes who can sit on the board and therefore whose appointments and resignations fill the directors' register. Delaware imposes no residency or citizenship requirement on directors: a Delaware corporation can have a board composed entirely of non-US residents. Federal Canada is stricter. Under CBCA s. 105(3), at least 25 percent of the directors must be resident Canadians, and where a corporation has fewer than four directors, at least one must be a resident Canadian.

The provinces have moved in different directions. Ontario removed its resident-director requirement in 2021, and British Columbia has never imposed one, while other jurisdictions retain or have only recently dropped theirs. For a cross-border group this is a practical constraint on structure: a Delaware top-co can be governed by a board of non-residents, but a federal Canadian subsidiary still needs the resident-Canadian quarter on its own board, and the directors' register has to show it. The records consequence is that director appointments cannot be treated as interchangeable across the two entities, and each board's composition has to be evidenced in that entity's own minute book.

Annual maintenance and filings

Delaware corporations file an annual report and pay the Delaware franchise tax each year; the franchise tax can be calculated two ways, and the default method often produces an alarming number that the alternative method reduces sharply. Canadian corporations file an annual return with the relevant registry (Corporations Canada for CBCA, the provincial registry otherwise), which is an information filing distinct from the corporate income tax return. Both feed back into the records: the filing and its acknowledgment belong in the minute book, and a lapse can put the corporation offside or, eventually, lead to dissolution. The mechanics are in how to file an annual return, and deadlines and fees by jurisdiction are in the free annual filing lookup.

Retention periods

Canada keeps records longer. The CBCA requires retention for six years after dissolution under s. 226, and ongoing records persist for the life of the corporation. Delaware generally requires most books and records to be kept for three years, while the stock ledger is maintained on an ongoing basis because it governs voting and inspection. For a cross-border group, the clean operating rule is to apply the longer Canadian retention period across the whole structure rather than tracking two clocks.

Cross-border structures

The comparison becomes concrete in the structures Canadian founders actually use.

The Delaware flip. When a Canadian company raises from US investors, it often creates a Delaware top-co and exchanges shares so the Delaware entity owns the Canadian one. After the flip there are two corporations and two sets of records. The Delaware top-co begins its records at incorporation; the Canadian company keeps maintaining its CBCA or provincial records and its significant-control register as a subsidiary. The share exchange itself must be documented in both entities' records, and a diligence team will check that the two reconcile.

The holdco. A Canadian holdco owning operating subsidiaries maintains its own minute book and significant-control register, and each subsidiary maintains its own. Consolidating these in one place, reconciled, is the difference between a clean diligence and a multi-week scramble. Our guide on preparing for due diligence covers what reviewers expect across a multi-entity group, and how to structure a multi-entity holdco covers the group itself in depth.

In every cross-border case the principle is the same: each corporation is a separate legal person and keeps its own records under its own statute. The work is not choosing one regime; it is satisfying both at once without letting the records drift apart.

Side-by-side comparison

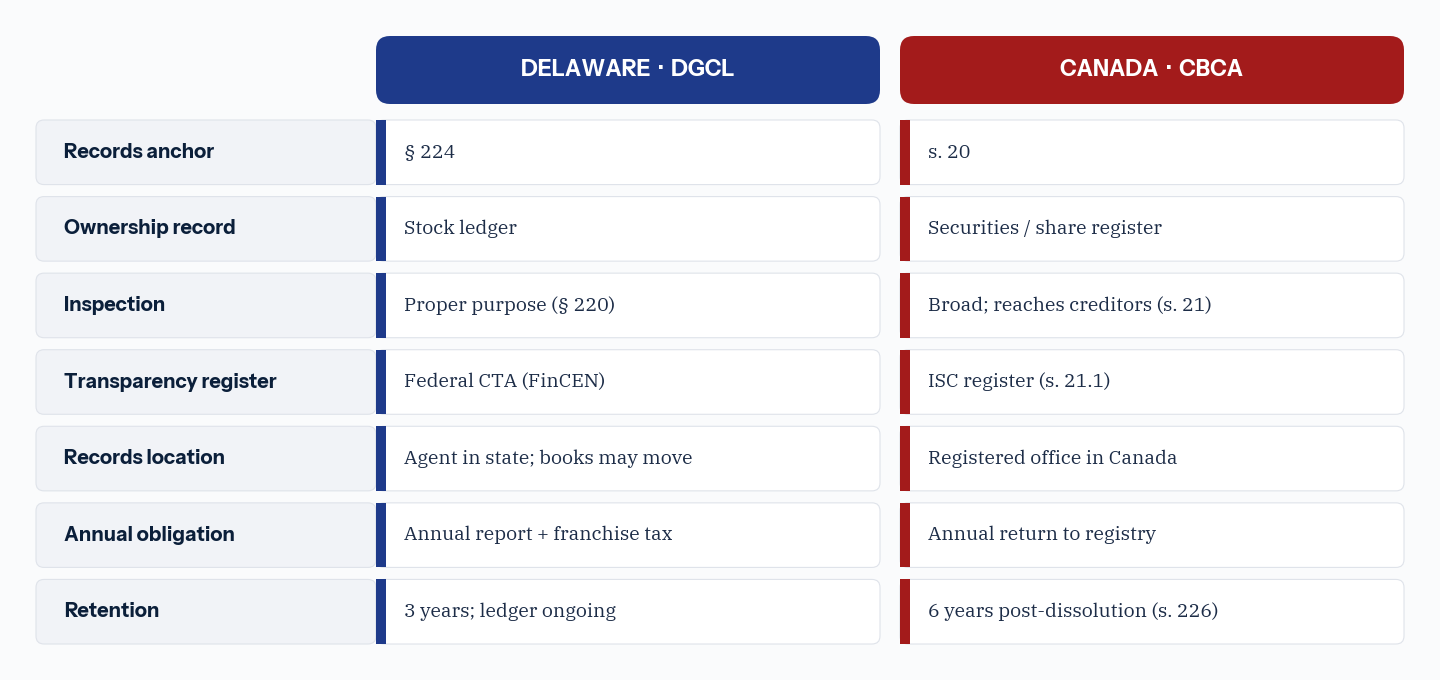

| Dimension | Delaware (DGCL) | Canada (CBCA) |

|---|---|---|

| Records anchor | § 224 | s. 20 |

| Definitive ownership record | Stock ledger | Securities / share register |

| Shareholder inspection | Proper purpose required (§ 220) | Broad; reaches creditors (s. 21) |

| Transparency register | Federal CTA reporting (FinCEN) | ISC register (s. 21.1) |

| Records location | Registered agent in state; books may be elsewhere | Registered office or other place in Canada |

| Annual obligation | Annual report + franchise tax | Annual return to the registry |

| Retention | Generally three years; ledger ongoing | Six years after dissolution (s. 226) |

For the individual jurisdictions, see the records guides for Delaware, Canada (CBCA), Ontario, and the full set of jurisdiction guides.

Octelligence keeps a statute-aware records set for each entity in a cross-border group, the Delaware records book, the Canadian minute book, and the significant-control register, each in its own structure, reconciled to the share register and cap table. A diligence export produces the whole group as one indexed package, so the Delaware top-co and the Canadian subsidiary tell the same story.

See Digital Corporate RecordsCommon questions

Keep the Delaware records book, the Canadian minute book, and the significant-control register aligned, reconciled to the share register and cap table, and ready for diligence.