How to structure a multi-entity holdco

A holding company sounds like an advanced move, but most founders who keep building eventually end up with one: a parent corporation that owns the shares of one or more operating companies. The structure unlocks tax planning, creditor protection, and clean separation between businesses. It also multiplies the corporate records you have to keep, because every entity in the group is a separate legal person with its own minute book, registers, and obligations. This guide explains what a holdco structure is, why founders use one, and how to keep the records across the group clean enough to survive diligence.

| What | A parent corporation that owns operating subsidiaries |

|---|---|

| Why | Tax deferral, creditor protection, multiple businesses, estate planning |

| Records | Each entity keeps its own minute book, registers, and ISC register |

| Common tool | Section 85 rollover to move shares into the holdco tax-deferred |

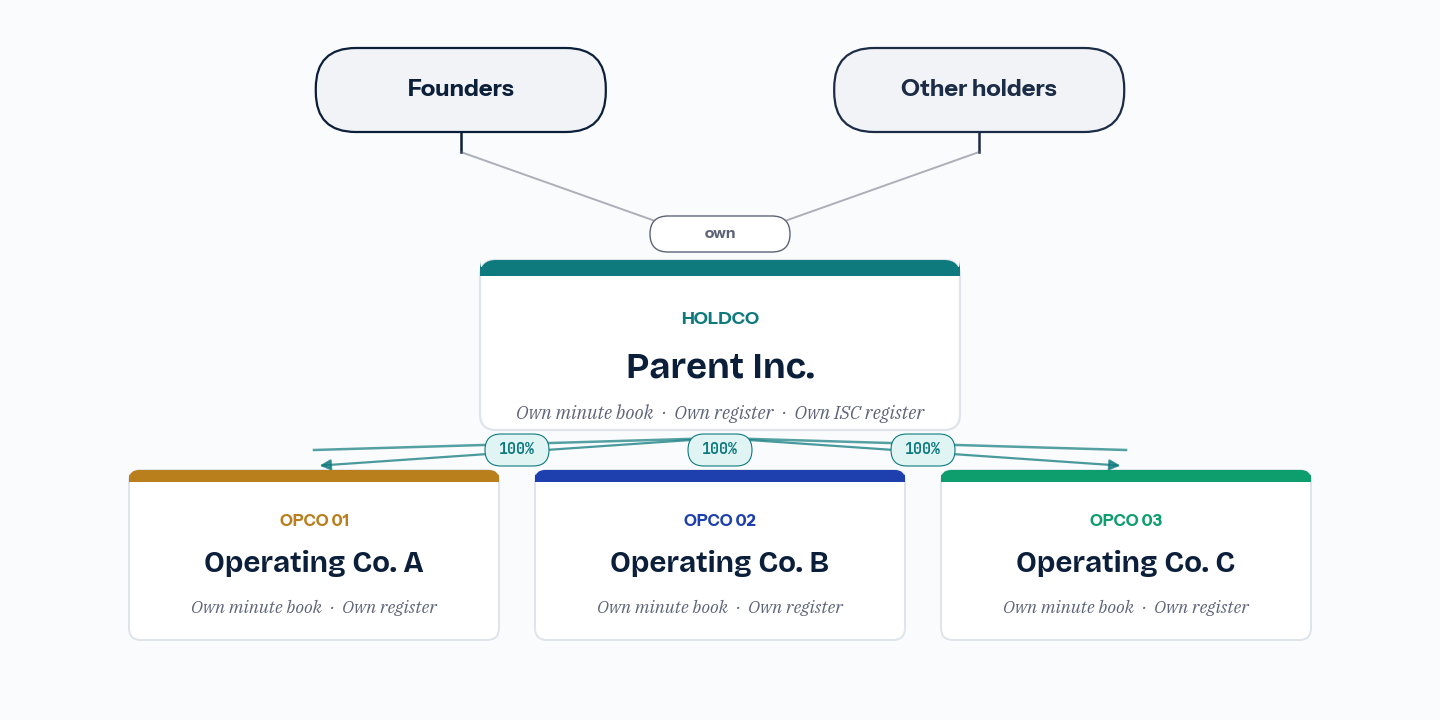

- A holdco owns the shares of one or more operating companies; the group is several corporations, not one

- Each corporation keeps its own minute book, share register, and significant-control register

- Every intercompany transfer, dividend, and reorganization creates records in two sets of books

- The Section 85 rollover is the usual tax-deferred way to move shares into a holdco

- Diligence on a group runs entity by entity; one broken subsidiary book stalls the whole deal

On this page

What a holdco structure is

A holding company, or holdco, is a corporation whose main asset is the shares of other corporations rather than an operating business of its own. The companies it owns are the operating companies, or opcos. In the simplest version, a founder owns a holdco, and the holdco owns the opco that actually sells the product or service. From there the structure can grow: one holdco over several opcos, a holdco owning another holdco, or a family of subsidiaries under a single parent. The defining feature is that ownership flows in a chain, and each link in that chain is a separate corporation governed by its own statute and its own records.

This guide is not tax or legal advice; the right structure depends on your circumstances and should be set up with an accountant and a lawyer. What this guide covers is the part that is constant across every holdco: the corporate records the structure generates, and how to keep them clean.

Why founders use a holdco

There are four reasons a holdco shows up again and again.

- Tax deferral. Retained earnings can often be moved from an operating company up to a holdco as an intercorporate dividend, frequently on a tax-deferred basis between connected Canadian corporations, so profits are not exposed to personal tax until the founder takes them out. The holdco becomes the place where surplus accumulates and is invested.

- Creditor protection. Cash and investments held in the holdco are one step removed from the operating company's trade creditors and litigation risk. The opco runs the risky business; the holdco holds the value.

- Multiple businesses. A founder running more than one venture can put each in its own opco under a common holdco, keeping liabilities and cap tables separate while consolidating ownership at the top.

- Estate and succession planning. A holdco is the usual vehicle for an estate freeze and for bringing in a family trust or the next generation, because share classes in the holdco can be structured to separate growth from control.

The anatomy of the group

A typical group has a parent (the holdco), one or more operating subsidiaries (the opcos), and sometimes intermediate holdcos. Each is its own corporation: it was incorporated under a statute (the CBCA federally, or a provincial Act), it has articles and bylaws, a board, officers, a share register, and a minute book. The ownership chain is recorded twice at every link: the parent's minute book shows that it holds the subsidiary's shares, and the subsidiary's register shows the parent as the holder. When those two views agree at every level, the structure is clean. When they drift, the group's ownership becomes a question rather than a fact.

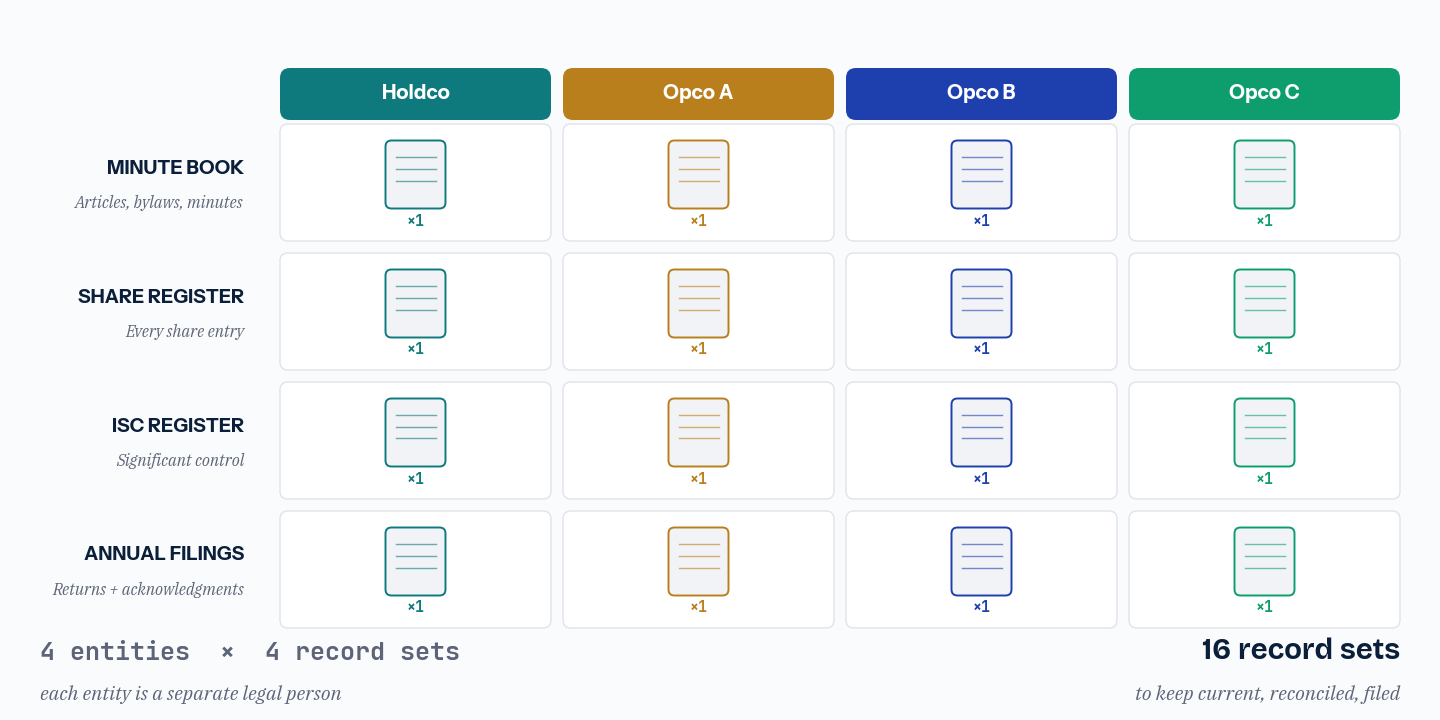

Records obligations multiply

The single most underestimated cost of a holdco is that the records do not add up, they multiply. Each corporation independently owes the full set of obligations: it maintains its minute book, keeps its registers of directors, officers, and shareholders, maintains its beneficial-ownership or significant-control register where the jurisdiction requires it, holds its annual meetings, and files its annual return. A group of one holdco and three opcos is four minute books, four sets of registers, four significant-control registers, and four filing calendars. Our complete guide to corporate minute books covers what belongs in each one; the holdco challenge is doing it consistently across all of them at once.

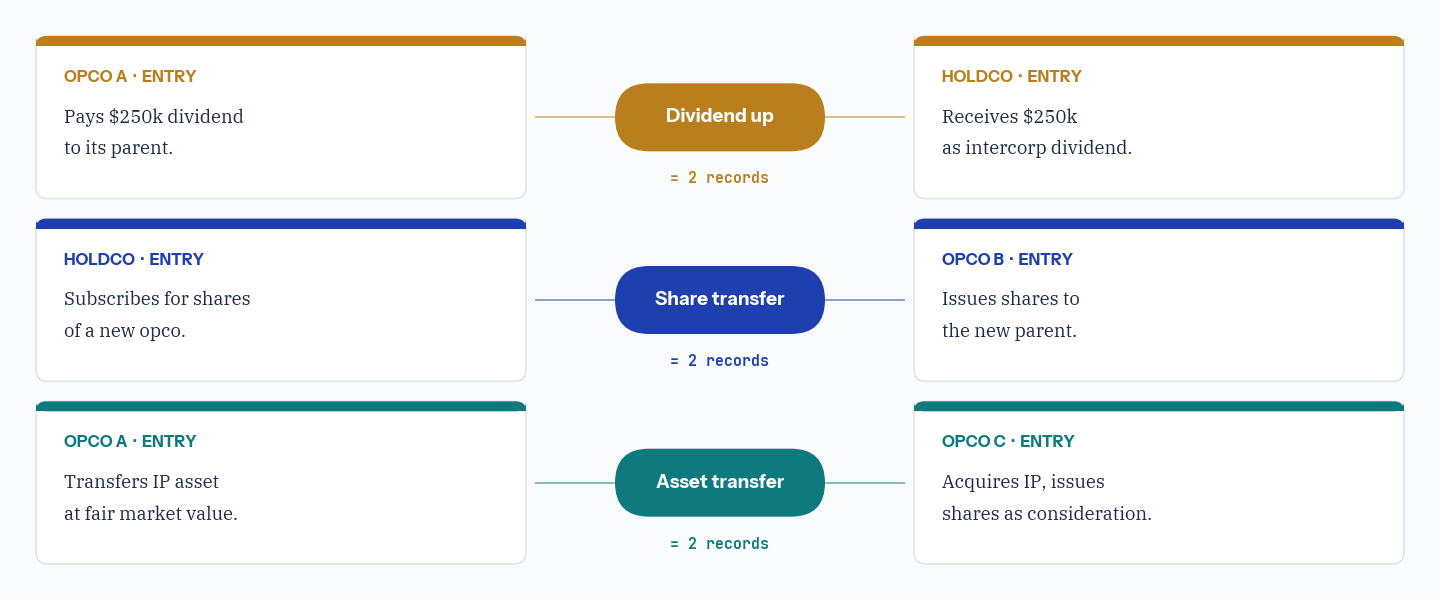

Intercompany transactions

The transactions that hold a group together are themselves records events, and they hit two sets of books each time. When the holdco subscribes for shares of a new opco, the opco records the issuance and the holdco records the investment. When an opco pays a dividend up to the holdco, both boards' resolutions and both minute books reflect it. When assets or shares move between entities, each side documents the transfer. The discipline is the same as a single company, applied in pairs: the authorizing board resolution, the supporting agreement, and the matching register entry, on both sides, on the date of the transaction. Skipping the paperwork on intercompany moves is the most common way a group's records fall out of sync.

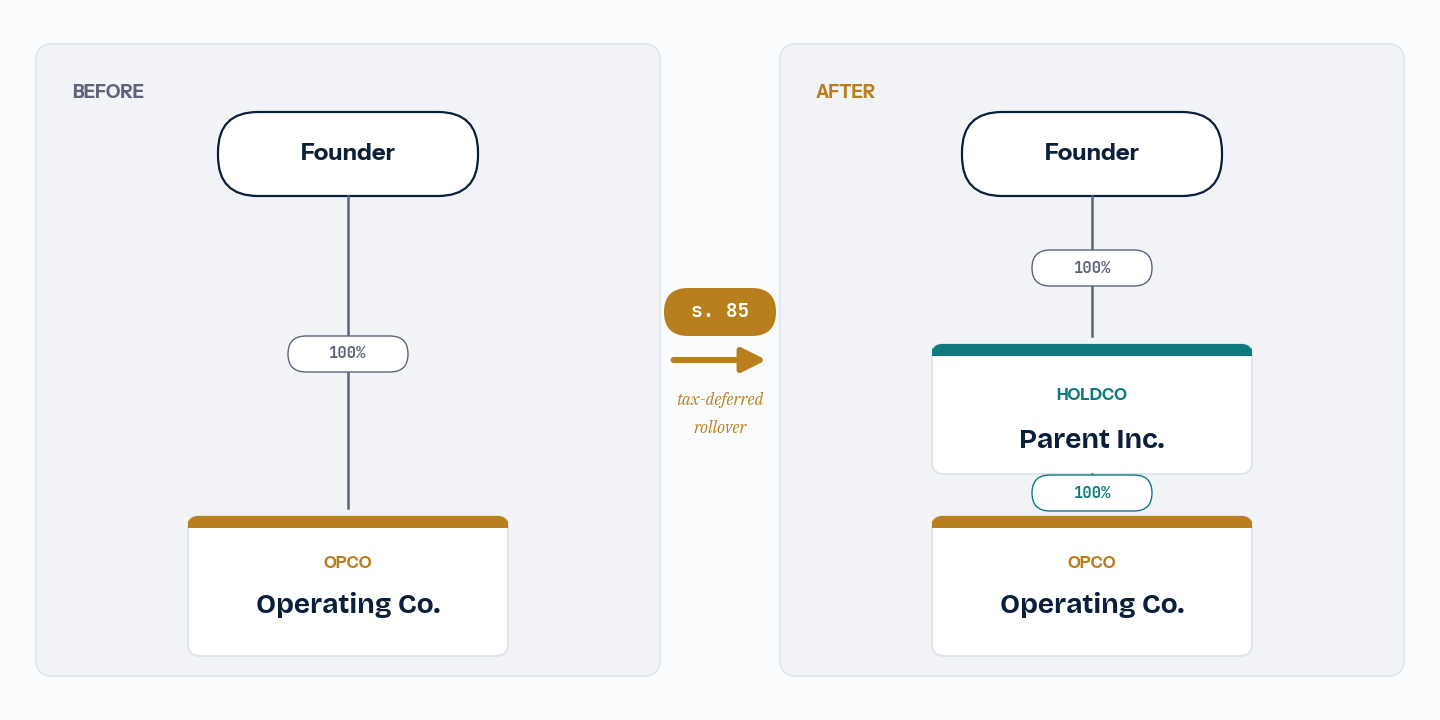

The Section 85 rollover

Most holdcos are created after the opco already exists, which means the founder's opco shares have to move up into the new holdco. Doing that as a straight sale would trigger a capital gain. The usual solution is a rollover under Section 85 of the Income Tax Act, which lets the founder transfer the opco shares to the holdco on a tax-deferred basis in exchange for holdco shares, by filing a joint election that sets the transfer price. The rollover is a tax mechanism, but it is also a records event: the holdco issues shares to the founder, the opco register is updated to show the holdco as the new holder, and the s. 85 election and the related agreements are filed in both minute books. A rollover that is correct on the tax return but missing from the corporate records is a gap a diligence team will find. Related reorganizations, such as an amalgamation, create the same dual-records obligation.

Governance across the group

Each board governs its own corporation, even when the same people sit on all of them. Decisions are made and minuted at the right level: an opco's dividend is authorized by the opco board, the holdco's investment decisions by the holdco board. Where the same individuals are directors of both parties to a transaction, the related-party nature of the deal should be noted and the appropriate approvals documented. Group-wide, a board governance checklist helps keep each entity's meetings, resolutions, and filings on cadence, and the annual compliance calendar tracks the multiplied filing deadlines so none of the entities quietly lapses.

Where holdco groups fail in diligence

When a group is acquired or raises at the top, diligence runs through every entity. The reviewer confirms the ownership chain link by link, checks that each intercompany transfer was authorized and recorded, and verifies that each corporation is in good standing with its filings current. The failures are predictable: a subsidiary whose minute book was never maintained after incorporation, an intercompany share transfer that appears on one register but not the other, a dividend with no authorizing resolution, or an opco that lapsed because its annual return was forgotten in the shuffle of managing several entities. Our guide to preparing for due diligence covers what reviewers expect, and the free corporate records health check is a fast way to baseline each entity before a process starts.

Cross-border holdcos

Many Canadian groups end up with a foreign entity in the chain, most often a Delaware top-co added in a financing flip, with the Canadian holdco and opcos surviving underneath. That adds a second statutory regime to the records picture: the Delaware entity follows the DGCL while the Canadian entities follow the CBCA or a provincial Act, including the significant-control register that Delaware has no equivalent for. The differences are covered in Delaware vs Canadian corporate records, and the broader regime comparison is in our cross-jurisdiction governance comparison. The principle does not change: each entity keeps its own records under its own statute, and the chain has to reconcile across borders.

Setting it up right

The cheapest time to get a holdco's records right is at the moment each entity is created. Incorporate cleanly, open the minute book with the organizing documents and the founding share issuance, and record the ownership link to the parent on both registers immediately. Set the filing calendar for every entity from day one. Document every intercompany transaction in pairs as it happens, not at year end. Treat the group as what it is, several corporations that have to tell one consistent story, and the structure that looked like a compliance burden becomes the thing that lets you raise, sell, or reorganize without a scramble. For groups and the firms that manage them, portfolio licensing covers many entities under one workspace.

Octelligence keeps a separate minute book, share register, and significant-control register for every entity in the group, and reconciles the ownership chain across them, so the parent's holdings always match each subsidiary's register. Intercompany transfers, dividends, and reorganizations are recorded on both sides, and a diligence export produces the entire group as one indexed package.

See firm and portfolio solutionsCommon questions

Keep a minute book, register, and significant-control register for every entity, with the ownership chain reconciled across the group and ready for diligence.