Cross-Jurisdiction Governance Comparison

Structured comparison of the three corporate-law regimes most relevant to cross-border private corporations: the Canada Business Corporations Act, the Delaware General Corporation Law, and the UK Companies Act 2006. Nine governance dimensions, side-by-side, with the operational consequence of each difference.

Executive summary

Private corporations operating across borders run into the corporate-law differences between their jurisdictions more often than any other governance issue. A US-incorporated Delaware C-corp with a Canadian operating subsidiary, a UK-incorporated limited company with US investors, or a federal CBCA corporation with US directors: each lives across two or three regimes simultaneously, and the regimes disagree on details that matter operationally.

This comparison covers the three regimes most often involved: the Canada Business Corporations Act (CBCA), the Delaware General Corporation Law (DGCL), and the UK Companies Act 2006. Nine governance dimensions are compared. The goal is a single reference that resolves the most-frequently-asked cross-regime questions without requiring three separate sources.

The comparison is structural, not exhaustive. Provincial Canadian statutes (OBCA, BCBCA, QBCA) generally follow the CBCA pattern with provincial variations; major US states (California, New York, Texas) follow the DGCL pattern with state variations. The CBCA / DGCL / UK Companies Act tri-comparison captures the dominant differences for cross-border governance work.

1. Written consent of shareholders

Whether shareholders can act by written consent instead of holding an annual meeting, and at what threshold.

| Dimension | CBCA | DGCL | Companies Act 2006 |

|---|---|---|---|

| Threshold for shareholder written consent | Unanimous (s. 142) | Majority sufficient (§ 228) | Unanimous for private companies (s. 296) |

| Annual meeting required if written consent used? | Annual meeting still required under s. 133 unless waived | Annual meeting required under § 211 but can be entirely substituted by § 228 written consent | Private companies not required to hold AGMs at all (s. 336) |

| Operational effect | Closely-held corporations can avoid AGM mechanics if all shareholders sign | Even with dissenting minority shareholders, majority can act without a meeting | UK private companies typically operate without AGM ceremony |

The Delaware position is operationally the most permissive: a majority of shareholders can act without holding a meeting at all. The CBCA and Companies Act both require unanimity, which means a single dissenting shareholder forces the meeting path. The UK adds a structural simplification (no AGM requirement for private companies) that the other regimes don't share.

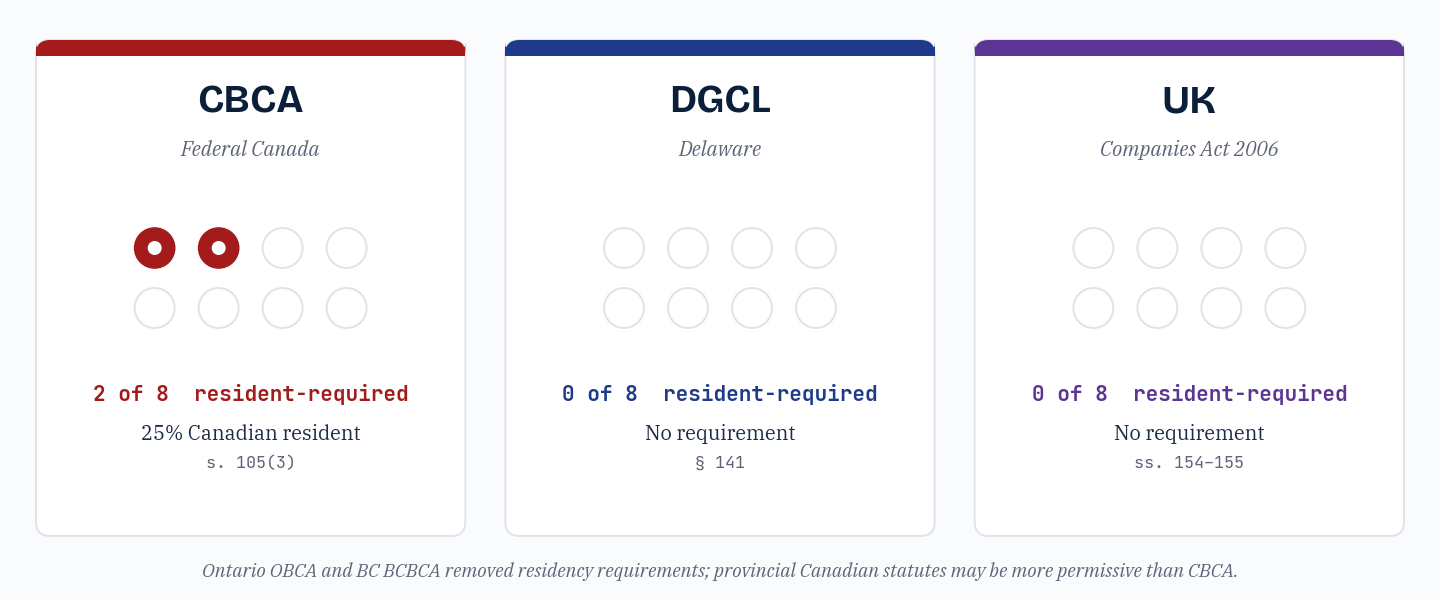

2. Director residency requirements

Whether the corporation's directors must include a minimum proportion of residents of the jurisdiction.

| Dimension | CBCA | DGCL | Companies Act 2006 |

|---|---|---|---|

| Resident director requirement | 25% of directors must be resident Canadian (s. 105(3)); majority for regulated industries | No residency requirement | No residency requirement |

| Exception | Corporations with fewer than 4 directors require 1 resident Canadian; some provincial statutes (Ontario OBCA, BC BCBCA) have no residency requirement | None applicable | None applicable |

| Operational effect | International founder teams choosing CBCA need at least one Canadian director; choosing OBCA, BCBCA, or ABCA removes that constraint | Delaware is the most flexible US jurisdiction for international boards | UK is the most flexible major jurisdiction overall |

Director residency is the single biggest operational difference for international founder teams. The CBCA's 25% requirement (with majority for regulated industries) drives many cross-border corporations to provincial Canadian statutes that removed residency requirements after 2021 (Ontario in particular), or to Delaware where no requirement exists at all.

3. Inspection rights of shareholders

What shareholders can inspect and what they must demonstrate to gain access.

| Dimension | CBCA | DGCL | Companies Act 2006 |

|---|---|---|---|

| Inspection right | Broad access to records under s. 21; available to shareholders, creditors, and their personal representatives | Right to inspect under § 220 but limited to "proper purpose reasonably related to the person's interest as a stockholder" | Anyone (not just members) may inspect the register of members under s. 116 on payment of a fee |

| Threshold to inspect | None; no proper-purpose requirement | Proper purpose must be demonstrated and is litigated regularly in the Court of Chancery | Five working days' response time required |

| Operational effect | Open access by default; corporations must keep records inspection-ready | The proper-purpose requirement gives Delaware corporations more control over who can inspect what | UK register of members is functionally public; PSC register is publicly searchable |

The UK is the most open regime: the register of members is inspectable by anyone, full stop. The CBCA is open to a defined class (shareholders, creditors, representatives) without requiring proper purpose. Delaware's proper-purpose requirement is the most restrictive of the three; it has produced a substantial body of case law and is a real consideration for corporations with potentially adversarial shareholders.

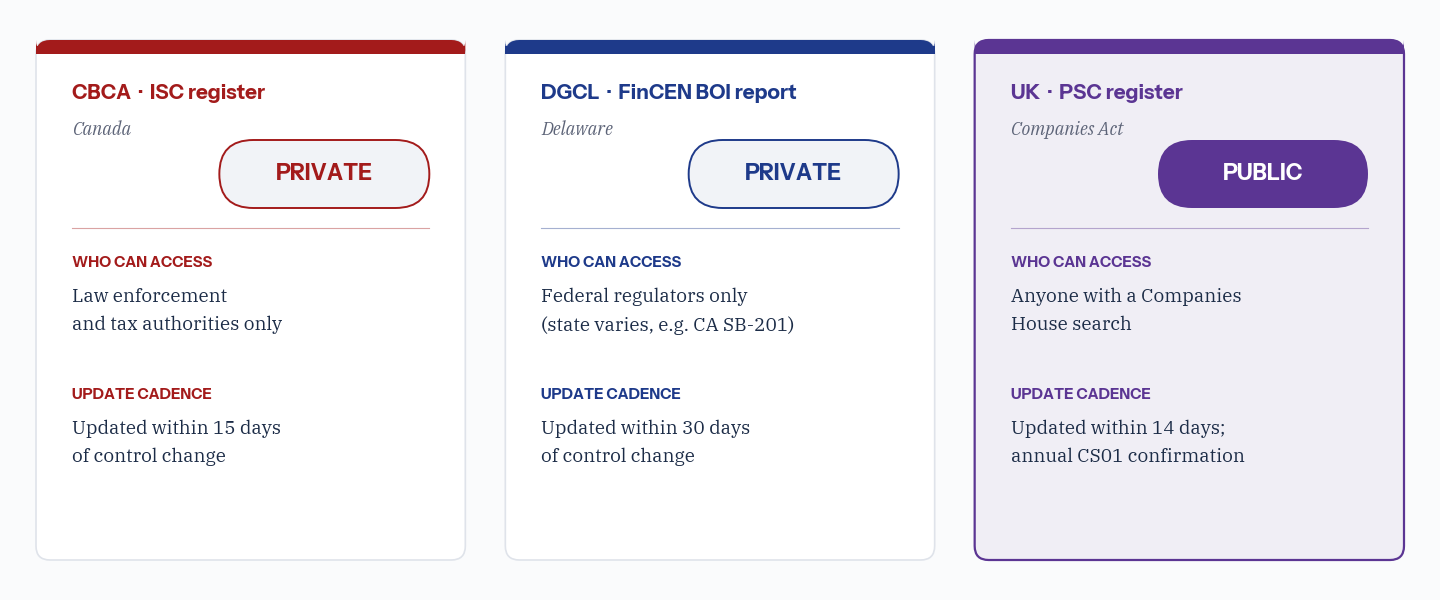

4. Beneficial ownership disclosure

What the corporation must record and disclose about who actually controls the corporation, beyond the registered legal owners.

| Dimension | CBCA | DGCL | Companies Act 2006 |

|---|---|---|---|

| Beneficial-ownership regime | Individuals with Significant Control (ISC) register under s. 21.1; private (accessible to law enforcement and tax authorities, not public) | FinCEN BOI reports under the federal Corporate Transparency Act (state-level varies; CA SB-201 layers state disclosure) | People with Significant Control (PSC) register under Part 21A; publicly searchable |

| Threshold of "control" | 25% or more of voting shares or shares by value; control in fact | 25% or more of ownership or substantial control | 25%+ ownership, voting rights, board appointment power, or significant influence/control |

| Update frequency | 15 days from change | 30 days from change | Within 14 days of change; annual confirmation via CS01 |

| Operational effect | Annual review of the ISC register is standard; failure to maintain attracts material penalties | Federal CTA enforcement is recent and developing; penalties for non-compliance are significant | The publicly-searchable nature of the PSC register makes UK BO compliance visible to the public |

All three regimes have adopted beneficial-ownership disclosure in the last decade. The substantive thresholds are similar (25% as the floor). The principal operational difference is public visibility: the UK's PSC register is searchable by anyone, while Canadian ISC and US FinCEN BOI records are accessible only to authorities. UK companies must consider PSC accuracy as a public-facing matter; Canadian and US corporations treat it as a compliance matter with private records.

5. Share certificates and uncertificated stock

Whether share certificates must be issued in physical form and whether uncertificated alternatives are available.

| Dimension | CBCA | DGCL | Companies Act 2006 |

|---|---|---|---|

| Certificate issuance | Permitted under s. 49 in any form; uncertificated explicitly allowed | Permitted under § 158; uncertificated stock fully permitted under § 158 and § 159 | Required within 2 months of allotment (s. 769) unless shares are uncertificated; private companies generally use paper |

| Uncertificated form | Permitted; register entry alone serves as ownership record | Permitted; widely used in modern Delaware corporations | CREST-eligible for public-market shares; private companies typically use paper or in-book uncertificated |

| Required certificate content | Must include "Canada Business Corporations Act" or French equivalent; corporate name; class and number; signatures | Required content minimal; bylaws control specifics | Required content under articles; statutory references must appear |

| Operational effect | Mixed certificated/uncertificated corporations are common in Canada | Modern Delaware startups commonly issue uncertificated stock to institutional investors and certificates to individual founders | UK private companies remain predominantly paper-certificated despite uncertificated availability |

All three regimes permit both paper certificates and uncertificated stock. The DGCL and CBCA are operationally similar; UK private companies have lagged in adopting uncertificated form despite legal permission, largely from path dependence on Companies House registration patterns.

6. Conflicts of interest and related-party transactions

What disclosure is required when a director has an interest in a corporate transaction, and what approval is needed for the transaction to be effective.

| Dimension | CBCA | DGCL | Companies Act 2006 |

|---|---|---|---|

| Disclosure requirement | Disclosure under s. 120 required for any material interest in a contract; conflicted director may not vote unless the matter relates to remuneration, indemnity, or insurance | Disclosure under § 144 required; transaction is not voidable if disclosed and approved by disinterested directors, by shareholders, or shown to be fair to the corporation | Disclosure under s. 177 (proposed transactions) and s. 182 (existing transactions); declaration to other directors required |

| Approval mechanism | Disinterested directors approve, or shareholders ratify, or proven fair | Disinterested directors approve, or shareholders ratify, or proven fair | Member approval required for some transactions (substantial property, loans to directors); board approval after disclosure for others |

| Voting after disclosure | Conflicted director cannot vote in most cases | Conflicted director can vote in most cases (subject to fiduciary duty) | Conflicted director cannot vote on the matter |

| Operational effect | Strict no-vote rule means closely-held corporations with overlapping directorships face procedural friction on every related-party transaction | Relatively permissive; Delaware case law is well-developed on what counts as adequate disclosure and approval | Strict no-vote rule plus member-approval requirement for major related-party transactions adds friction |

Delaware's regime is the most permissive on conflicts: a conflicted director can vote on the transaction, provided full disclosure and either disinterested-director or shareholder approval or proven fairness. The CBCA and Companies Act both prohibit the conflicted director from voting. For closely-held corporations with overlapping directorships and management ownership, the Delaware regime is materially simpler to operate.

7. Annual meeting requirements

Whether the corporation must hold an annual general meeting, the timing, and the alternatives.

| Dimension | CBCA | DGCL | Companies Act 2006 |

|---|---|---|---|

| AGM required? | Yes (s. 133); within 15 months of prior meeting and within 6 months of fiscal year end | Yes (§ 211) | No for private companies; yes for public companies (s. 336) |

| Notice period | 21 to 60 days (s. 135) | 10 to 60 days (§ 222) | 21 days for private; 28 days for public; variable for traded |

| Substitute via written consent? | Unanimous (s. 142) | Majority sufficient (§ 228); functionally substitutes for the AGM | For private companies, written resolutions can be used in lieu of meetings (s. 288) |

| Operational effect | Practical for closely-held corporations to substitute written consent annually; required documentation differs from a meeting record | Delaware corporations frequently operate without holding actual annual meetings, using § 228 consent | UK private companies generally avoid the AGM ceremony altogether |

The UK regime is structurally the simplest: private companies have no AGM requirement at all. Delaware is functionally similar in practice because majority written consent can substitute. The CBCA requires unanimous consent for written substitution, which is more restrictive in corporations with even one dissenting shareholder.

8. Audit and financial-statement requirements

Whether the corporation must have its financial statements audited, and at what scale.

| Dimension | CBCA | DGCL | Companies Act 2006 |

|---|---|---|---|

| Audit requirement | Audited financial statements required (s. 159) unless waived by unanimous shareholder consent under s. 163 | No state-level audit requirement for private corporations | Required if turnover > £10.2M, balance-sheet > £5.1M, or > 50 employees; small companies exempt |

| Waiver path | Unanimous shareholder consent waives audit annually | Not applicable | Small-company exemption applies automatically if thresholds met |

| Operational effect | CBCA corporations routinely waive audit through unanimous consent until growth or external shareholders make audit valuable | Audit is investor-driven, not statute-driven, in Delaware | UK private companies cross into mandatory audit at definable revenue/size thresholds |

The Delaware regime imposes no statutory audit requirement; audited financials are required only by investor agreements (typical in venture-backed corporations). The CBCA requires audit by default, with unanimous-shareholder waiver as the practical opt-out. The UK applies a size threshold, making the requirement automatic at scale.

9. Dissolution and winding up

How a corporation is dissolved or wound up, and what procedural steps are required.

| Dimension | CBCA | DGCL | Companies Act 2006 |

|---|---|---|---|

| Voluntary dissolution | Articles of dissolution filed after winding up (s. 210); shareholder special resolution required | Dissolution by certificate filed with Delaware Division of Corporations; shareholder approval required (§ 275) | Members' voluntary liquidation under Insolvency Act 1986; special resolution to wind up |

| Administrative dissolution | Corporations Canada may dissolve for failure to file annual return (s. 212) | Delaware may declare a corporation void or forfeit for non-payment of franchise tax | Companies House may strike off for failure to file accounts or confirmation statements (s. 1000) |

| Restoration / reinstatement | Available; procedure under s. 209 within specified timeframes | Available via reinstatement filing with associated fees | Administrative restoration available for up to 6 years after strike-off; court restoration possible later |

| Operational effect | Administrative dissolution for missed filings is common; restoration is procedural but takes weeks | Delaware corporations forfeited for unpaid franchise tax are routinely reinstated upon payment | UK strike-off and restoration is a frequent operational concern for dormant companies |

All three regimes provide voluntary dissolution mechanics and administrative dissolution for non-filing. The operational difference is the threshold at which administrative dissolution triggers: Delaware is the most aggressive (unpaid franchise tax forfeits the corporate existence), the UK is the most pattern-based (strike-off for repeated filing failures), and the CBCA is in the middle (registry action for sustained non-filing).

Operational implications

The comparison surfaces several patterns relevant to cross-border governance:

Delaware is operationally the most permissive on shareholder meetings, conflicts, and director residency. This is the structural reason for Delaware's dominance among US-incorporated corporations and the increasing share of cross-border startups choosing Delaware C-corp domicile.

The UK is structurally the most permissive on private-company formalities (no AGM requirement, no resident director requirement, broad written-resolution availability) but pays for that flexibility with the most public-facing beneficial-ownership regime (PSC publicly searchable).

The CBCA sits between the two on most dimensions, with a few notable strictnesses (Canadian resident director requirement, unanimous written consent threshold, default audit requirement). Provincial Canadian statutes (Ontario OBCA, BC BCBCA, Alberta ABCA) have moved toward the Delaware position on several dimensions, particularly director residency.

For cross-border founders evaluating jurisdiction of incorporation, the comparison generally favours Delaware for governance flexibility, the UK for private-company ease and tax planning, and the CBCA / OBCA / BCBCA for operating-in-Canada compliance and the qualified small business corporation tax framework. The right choice depends on where the corporation actually operates, where its investors are, and what its exit pattern is likely to be.

Methodology and limitations

This comparison covers structural features of the three corporate-law regimes as of May 2026. Statutes evolve; recent amendments (UK's PSC regime extensions, Canadian provincial residency removals, US Corporate Transparency Act implementation) are reflected. Industry-specific overlays (regulated financial services, healthcare, defense) are out of scope. State-level US variations are noted but the DGCL is taken as representative; provincial Canadian variations are noted but the CBCA is taken as representative.

The comparison does not address tax treatment (federal or provincial/state), securities law overlays (NI 45-106, federal Securities Act, FSMA 2000), employment law differences, or litigation regimes (Court of Chancery vs. Ontario Superior Court vs. UK High Court). These layers add additional cross-border considerations that any specific transaction will need to address with counsel in each jurisdiction.

Treat this comparison as a starting reference for cross-border governance decisions, not a substitute for jurisdiction-specific legal advice on any specific transaction.

Suggested citation: Octelligence Research, Cross-Jurisdiction Governance Comparison, May 2026. Available at octelligence.com/global/en/research/cross-jurisdiction-governance-comparison/.

Octelligence supports 41 jurisdictions including all three regimes covered here, with jurisdiction-aware templates, statutory citations, and compliance tracking built in.