The Governance Maturity Framework

A four-tier model for evaluating private-corporation governance across seven dimensions, with a published scoring methodology and observable signals at each tier. Open methodology, citation-ready, applicable across CBCA, DGCL, and Companies Act 2006 jurisdictions.

Why a maturity framework

Governance discipline in private corporations is uneven by default. The standard reference is the corporation statute (CBCA, DGCL, OBCA, Companies Act 2006), which prescribes the minimum requirements but does not describe what mature governance practice looks like above the minimum. Between the statutory floor and the audit-grade institutional standard, there is no widely-used yardstick.

The Governance Maturity Framework is that yardstick. It defines four tiers of governance discipline across seven measurable dimensions, with a transparent scoring methodology so that any corporation can be placed in a tier on the basis of observable signals. The framework is intended to be used in three ways: as a self-assessment for founders, counsel, and boards to identify where to focus; as a benchmark for investors and acquirers conducting diligence; and as a citable reference for analysts, journalists, and academics writing about private-corporation governance.

This is version 1.0. The methodology is published openly. Subsequent versions will incorporate feedback from practitioners, additional jurisdictions, and the results of the annual benchmark study that builds on aggregated self-assessment data.

The four tiers

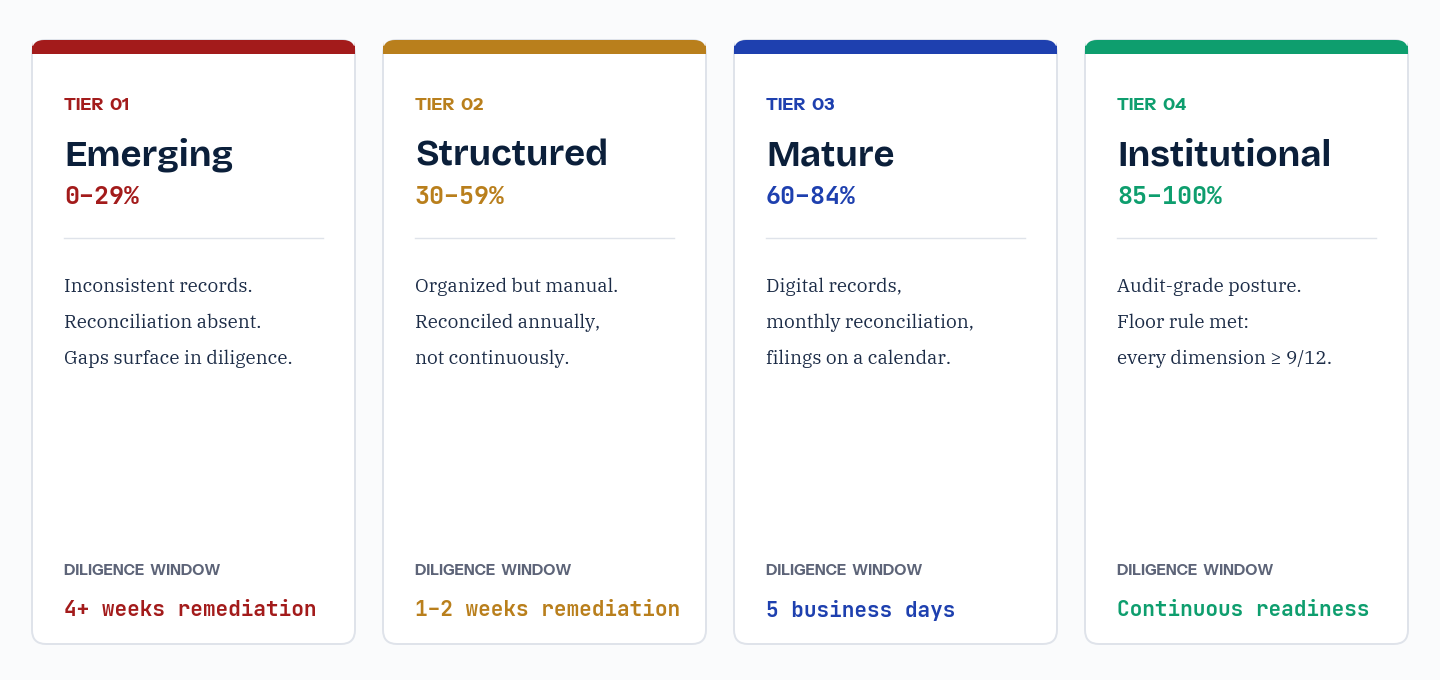

Each corporation is placed in one of four tiers based on its aggregate score across the seven dimensions. The tiers describe observable governance posture, not the corporation's stage, sector, or capitalization. A pre-seed corporation with disciplined founders can be Structured; a Series C corporation with broken records can still be Emerging.

Records and governance discipline exist in some form but are inconsistent across dimensions. Spreadsheets and PDFs spread across drives, no reconciliation cadence, beneficial-ownership filings often missed or partial. Diligence preparation typically takes four weeks or more of focused remediation.

Records are organized and maintained manually with predictable gaps. Reconciliation happens annually, not monthly. Beneficial-ownership filings are current but only because someone remembers them. Diligence preparation typically takes one to two weeks.

Digital corporate records with monthly or quarterly reconciliation between share register, certificates, and cap table. Beneficial-ownership registers maintained alongside the share register. Statutory filings on a calendar. Diligence-ready within five business days.

Audit-grade governance posture. Every dimension scored at least 9 out of 12 (the floor rule). Multi-stakeholder governance (board, audit, legal, finance) participates in the records discipline. Diligence-ready at any time without notice.

Floor rule: Institutional placement requires every dimension to score at least 9 out of 12, regardless of aggregate score. A corporation that scores 88% overall but has one dimension at 6 places in Mature, not Institutional. The floor rule prevents single-dimension excellence from masking weakness elsewhere.

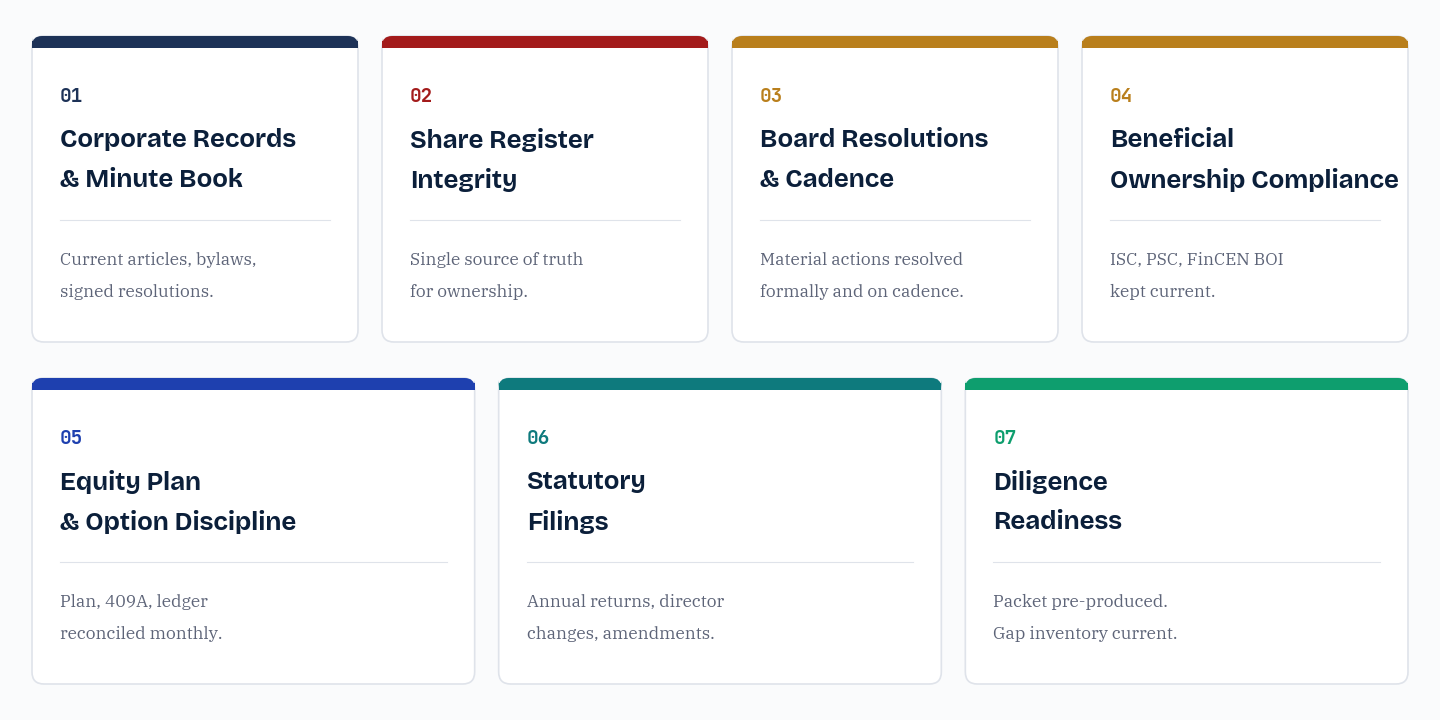

The seven dimensions

Each dimension is scored independently on four criteria, each worth 0 to 3 points (maximum 12 per dimension, maximum 84 across all seven). The criteria are observable, not aspirational: each can be answered yes / no / partial by someone with access to the corporation's records.

The minute book is current and complete: articles, bylaws, all board and shareholder resolutions, signed and dated. Detailed coverage of this dimension is in the companion Corporate Records Maturity Framework; this dimension scores the same observable signals on a four-criterion scale.

- Articles and bylaws current, with all amendments in chronological order and indexed

- Board resolutions filed promptly and signed by the date of the action (no gaps, no backdating)

- Shareholder resolutions retained with the notice, proxies, and voting record

- Minute book accessible from a single location, producible on inspection within one business day

The share register (or stock ledger) is the source of truth for ownership, reconciled to issued certificates and the cap table on a regular cadence.

- Single share register exists; cap table is generated from it, not maintained in parallel

- Every issuance, transfer, redemption, and cancellation recorded on the date of the action with the authorizing resolution and the certificate number

- Register reconciled to certificates and cap table monthly or quarterly, with a documented reconciliation date

- Certificate numbering sequential, no skipped or reused numbers, cancelled certificates retained

The board meets or acts by written consent at the cadence the corporation actually requires, with all material actions resolved formally and conflicts disclosed.

- Board meets or acts by written consent at least quarterly, with a documented agenda and minutes

- Every material action (issuance, financing, contract above signing-authority threshold, director change) authorized by a dated resolution

- Conflict-of-interest disclosures recorded and the conflicted director's vote handled per statute

- Written consent resolutions signed by all directors entitled to vote, with no missing signatures

The corporation maintains and files the beneficial-ownership registers required in its jurisdiction (ISC under CBCA, PSC under UK Companies Act 2006, FinCEN BOI under US Corporate Transparency Act, transparency register under OBCA, equivalent provincial registers).

- Beneficial-ownership register exists for every required jurisdiction

- Register is updated within the statutory deadline of every ownership change (typically 15 to 30 days)

- Initial and updated filings made with the relevant regulator (FinCEN, Companies House, Corporations Canada)

- Register reconciles to the share register and to the actual beneficial-ownership picture

The equity incentive plan is shareholder-approved, current, and operated with proper grant authorization, valuation discipline, and ledger reconciliation.

- Equity plan shareholder-approved, with current pool capacity tracked against grants and exercises

- Every grant supported by a current 409A (US) or equivalent fair-market-value evidence (non-US)

- Option ledger reconciled to the cap table with vesting accrual, exercises, and forfeitures current

- ISO/NSO designation (US) or EMI/CSOP/unapproved designation (UK) or section 7 status (Canada) correctly classified and reflected in year-end tax reporting

All required regulatory filings (annual returns, director changes, articles amendments, registered-office changes) are filed on time, with acknowledgments retained.

- Annual returns filed on time for the past three years, with acknowledgments retained

- Director changes filed within the statutory window (typically 14 to 15 days) and reflected in the public record

- Articles amendments filed with the registrar and certificate of amendment retained

- Registered office and registered agent (where applicable) current and consistent across jurisdictions of registration

A complete diligence packet can be produced within the corporation's stated readiness window, with a current schedule of historical transactions and an explicit gap inventory.

- Diligence packet (corporate records, share register, cap table, option ledger, statutory filings, material contracts) producible within the corporation's stated readiness window

- Schedule of historical transactions (issuances, transfers, financings, option grants, articles amendments) maintained as a single document

- Gap inventory tracks any known defects and their remediation status (ratification status, court validation, settled, accepted risk)

- Diligence-readiness review conducted at least annually with a documented date and findings

Scoring methodology

Each criterion is scored on a four-point scale:

| Score | Meaning | Example |

|---|---|---|

| 0 | Not in place | Criterion is absent; the corporation does not perform the practice |

| 1 | Inconsistent or partial | Criterion is met some of the time, in some form, but without discipline; gaps observable on close inspection |

| 2 | In place, manual | Criterion is consistently met but maintained manually; reconciliation periodic rather than continuous; effective but fragile to staff change |

| 3 | In place, reconciled, automated where possible | Criterion is met systematically with controls, reconciliation, and (where practicable) automation; resilient to staff change; audit-traceable |

Dimension score = sum of the four criterion scores (maximum 12 per dimension).

Aggregate score = total across all seven dimensions, expressed as a percentage of the maximum (84). Expressed as a whole number 0 to 100.

Tier placement follows the aggregate score, subject to the floor rule for Institutional:

| Aggregate | Tier | Floor rule |

|---|---|---|

| 0 to 29% | Emerging | None |

| 30 to 59% | Structured | None |

| 60 to 84% | Mature | None |

| 85 to 100% | Institutional | Every dimension ≥ 9 out of 12 |

A corporation that scores 88% overall but has any single dimension below 9 out of 12 places in Mature, not Institutional. The floor rule prevents the aggregate from masking material weakness in a single dimension.

Who runs the scoring

The framework is designed to be runnable in three modes:

- Self-assessment. The corporation's secretary, CFO, or counsel runs the assessment using the corporation's own records. Time required: typically 60 to 90 minutes for a corporation in Structured tier or above; longer for Emerging because the records take longer to locate.

- Counsel-led assessment. Outside counsel runs the assessment, typically as part of a pre-financing or pre-acquisition records review. Time required: typically two to four hours, including reconciliation work.

- Diligence-team assessment. The investor's or acquirer's diligence team runs the assessment as part of the standard records review. Time required: typically aligned with the existing diligence schedule, with the framework providing a structured scoring output alongside the standard diligence work.

The free self-assessment tool automates the scoring for a self-assessment run.

Advancing between tiers

The framework is most useful when it identifies the highest-leverage move from the current tier to the next. The standard moves at each tier transition:

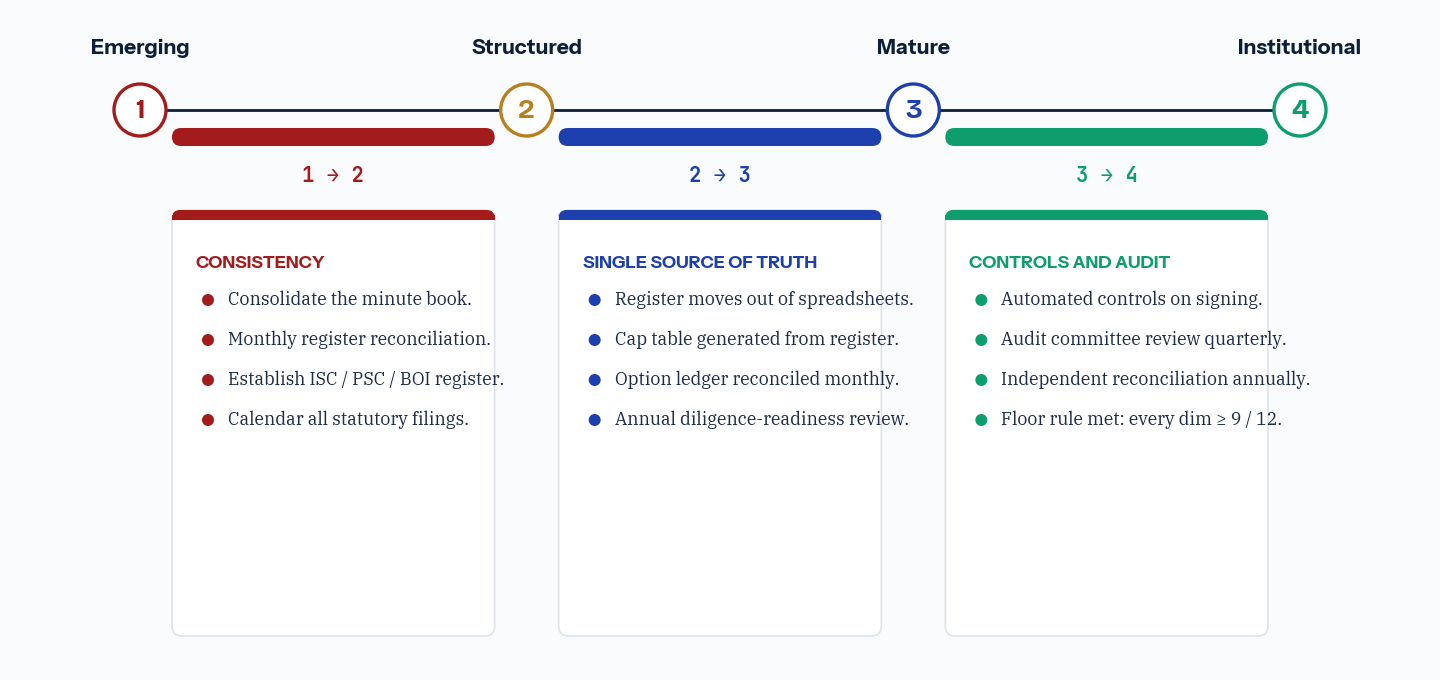

From Emerging to Structured

The leap from Emerging to Structured is about consistency, not technology. The corporation does not need a digital system to be Structured; it needs to consistently maintain the records it already produces. The standard moves:

- Consolidate the minute book into a single location (digital folder, physical book, or both) and bring it current with any missing resolutions

- Set a monthly reconciliation between the share register and the issued certificates; document the reconciliation date

- Establish a beneficial-ownership register in the corporation's primary jurisdiction (ISC under CBCA, PSC under UK, BOI under US CTA, transparency register under OBCA)

- Calendar the annual return, the director-change reporting window, and any other recurring statutory filing

- Run the diligence preparation procedure as a self-review even when no transaction is imminent

From Structured to Mature

The leap from Structured to Mature is about reconciliation cadence and single-source-of-truth discipline. The corporation moves from "we keep good records" to "our records are reconciled to each other in real time." The standard moves:

- Move the share register from a spreadsheet to a system where each entry references the authorizing resolution and the certificate (digital corporate records system, transfer agent, or counsel-managed system)

- Reconcile the share register to the cap table monthly; the cap table is generated from the register, not maintained in parallel

- Reconcile the option ledger to the cap table and to the equity plan's authorized pool monthly

- Maintain the beneficial-ownership register alongside the share register, with updates triggered by share-register changes

- Conduct a diligence-readiness review annually with a documented date and findings

From Mature to Institutional

The leap from Mature to Institutional is about controls, automation, and multi-stakeholder governance. The standard moves:

- Implement automated controls on signing authority, register changes, and resolution drafting (system-level workflow, not spreadsheet hygiene)

- Constitute an audit committee or equivalent that reviews records quarterly with documented findings

- Engage independent reconciliation (outside counsel or external corporate-services provider) at least annually

- Achieve the floor rule: every dimension at 9 out of 12 or above

- Pre-produce the diligence packet and keep it current; treat diligence as continuous rather than transaction-triggered

Related frameworks and resources

The Governance Maturity Framework is part of Octelligence Research's open-methodology body of work on private-corporation governance. Related artifacts:

- The Corporate Records Maturity Framework: deeper five-stage model for the Corporate Records dimension specifically, with observable signals at each stage

- The Diligence Failure Taxonomy: the patterns of records failure most often surfaced in financing and M&A diligence

- Cross-Jurisdiction Governance Comparison: side-by-side governance requirements across CBCA, DGCL, OBCA, and Companies Act 2006

- Governance Maturity Self-Assessment: interactive 28-question tool that runs the framework's scoring against your corporation's records

- Governance Maturity Benchmark 2026: the first benchmark study applying the framework across illustrative private corporations

The free self-assessment tool runs the framework's scoring against your corporation's records and links each gap to the relevant how-to guide or template.