The Corporate Records Maturity Framework

A five-stage model for evaluating how a private corporation manages its records, from ad-hoc to diligence-ready. For each stage: observable signals, common failure modes, and the operational playbook for moving up. A shared vocabulary for founders, counsel, boards, and operators.

Executive summary

Corporate records discipline is bimodal: a corporation either holds up under a diligence review or it does not. The transition between the two states is not gradual in any observable sense, but it is gradual in operational reality. The Corporate Records Maturity Framework names the intermediate states and the work required to move between them.

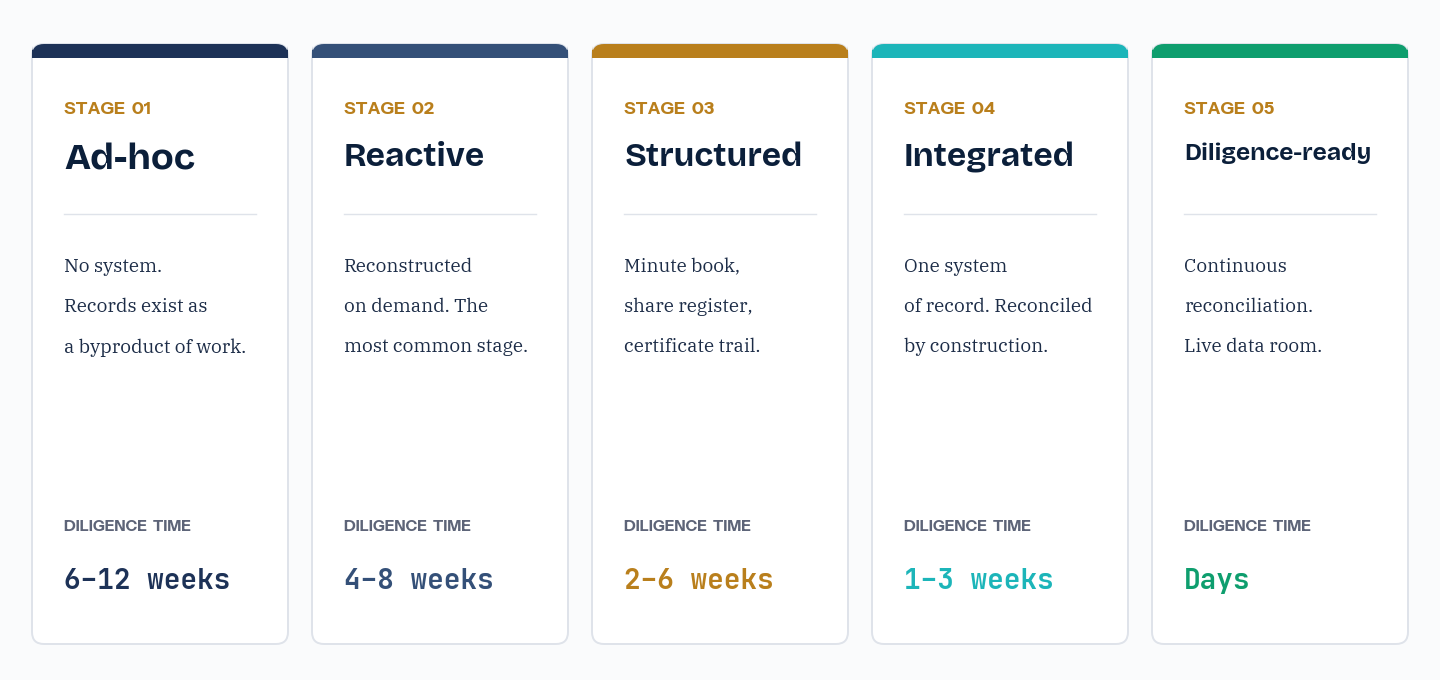

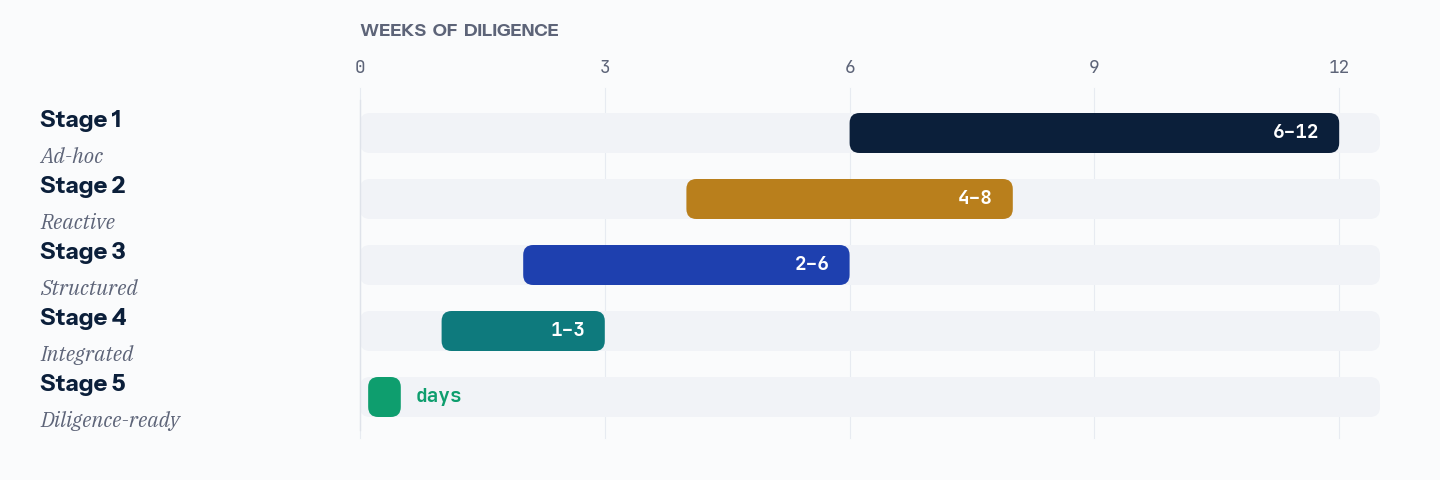

The framework defines five stages. Stage 1 (ad-hoc) describes the absence of any system. Stage 2 (reactive) describes the reconstruction-on-demand pattern that most private corporations occupy. Stage 3 (structured) describes the existence of a minute book, share register, and certificate discipline. Stage 4 (integrated) describes a single system of record that reconciles across artifacts. Stage 5 (diligence-ready) describes continuous reconciliation with sub-30-day data room production.

The framework is not a survey result; it is a taxonomy. Its value is as a shared vocabulary for assessing a corporation's current state and a structured playbook for moving up.

Why a maturity framework now

Three structural shifts have changed the cost-benefit calculus for corporate records discipline in the last five years.

First, financing diligence is faster and more thorough. Modern data-room software lets diligence counsel work through documents in parallel, with searchable archives that surface inconsistencies a human reviewer would miss. A gap in the records bundle that would have been overlooked in a 2015 financing is routinely flagged in a 2025 one.

Second, beneficial-ownership reporting is now a sustained compliance obligation, not an episodic one. The US Corporate Transparency Act, Canadian Individual with Significant Control rules under the CBCA and OBCA, and the UK People with Significant Control regime all require ongoing maintenance of records that previously sat at the edge of attention. Penalties have moved from theoretical to enforced.

Third, the corporate-records software category has matured. Tools that maintain the register, the certificate, the cap table, and the authorizing resolution as a single integrated record now exist and are operationally viable for corporations at every stage. The transition from Stage 3 to Stage 4 (and from Stage 4 to Stage 5) is no longer constrained by tooling.

Together, these shifts mean that the gap between Stage 2 and Stage 4 has grown more consequential, and the cost of crossing it has fallen. A maturity framework is most useful at exactly this point: when the transitions are tractable but not yet universal.

The five stages

Each stage below is characterized by four dimensions: the observable signals that identify a corporation at this stage, the common failure modes that surface, the diligence outcome if a transaction were to begin today, and the advancement path to the next stage.

There is no system. Records exist as a byproduct of other work: a signed PDF in someone's email, a notarized document in a counsel's office, an unfiled certificate in a desk drawer. The corporation may be operationally functional, but its corporate-records artifacts cannot be located on demand.

Observable signals

- No identified minute book; records would have to be assembled from email and physical files

- No share register kept separately from the cap table (and often no cap table either)

- Founders may not have signed restricted-stock purchase agreements with the corporation

- No authorizing resolution exists for actions that happened (officer appointments, share issuances)

- Beneficial-ownership filings either not made or not tracked

Common failure modes

- Pre-formation IP not formally assigned to the corporation

- 83(b) elections (US) missed because no one tracked the 30-day window

- Founder shares issued without a written subscription agreement or proof of consideration

- The corporation may be technically dissolved for missed filings without anyone noticing

Diligence outcome

A real diligence request would require reconstruction from scratch, often with significant counsel involvement. Six to twelve weeks of work, with material findings likely. Transactions at this stage are often deferred while remediation occurs.

Advancement to Stage 2

Engage corporate counsel to draft the foundational documents: articles certified by the registry, bylaws, founder restricted-stock purchase agreements, an initial board resolution, and a share register seeded with the founder issuances. This is typically a one-time engagement of $2,000–$8,000 depending on jurisdiction.

Records exist but are assembled in response to events. When a financing approaches or an audit begins, the corporation produces the bundle by reconstruction. Between events, the records age and drift relative to operational reality. Stage 2 is by far the most populous stage among private corporations.

Observable signals

- A minute book exists but is updated only when a major action requires it

- The cap table is maintained in a spreadsheet, separate from the share register

- Resolutions are drafted retroactively to cover prior decisions

- Certificate issuance is inconsistent; some are paper, some uncertificated, some never issued

- Annual filings are mostly current but with occasional misses

- Beneficial-ownership filings are made but may not reflect current state

Common failure modes

- Share register and certificates disagree on issued share counts

- Cap table reconciles to the register only at specific dates (round closings), drifts in between

- Authorizing resolutions exist but with date inconsistencies suggesting retroactive drafting

- Transfer history has informal gaps where shareholders transacted between themselves

Diligence outcome

Four to eight weeks of diligence work, with multiple findings that require ratifying resolutions, corrective filings, or indemnification carve-outs. Transactions usually close but with friction on the commercial terms. The pattern is recognizable to diligence counsel and tends to reduce trust on remaining negotiation points.

Advancement to Stage 3

Establish a single canonical minute book with chronological organization. Reconcile the share register to the certificate trail. Move the cap table to build from the register. Set a monthly or quarterly cadence for updating each. This is operational discipline, not a one-time project.

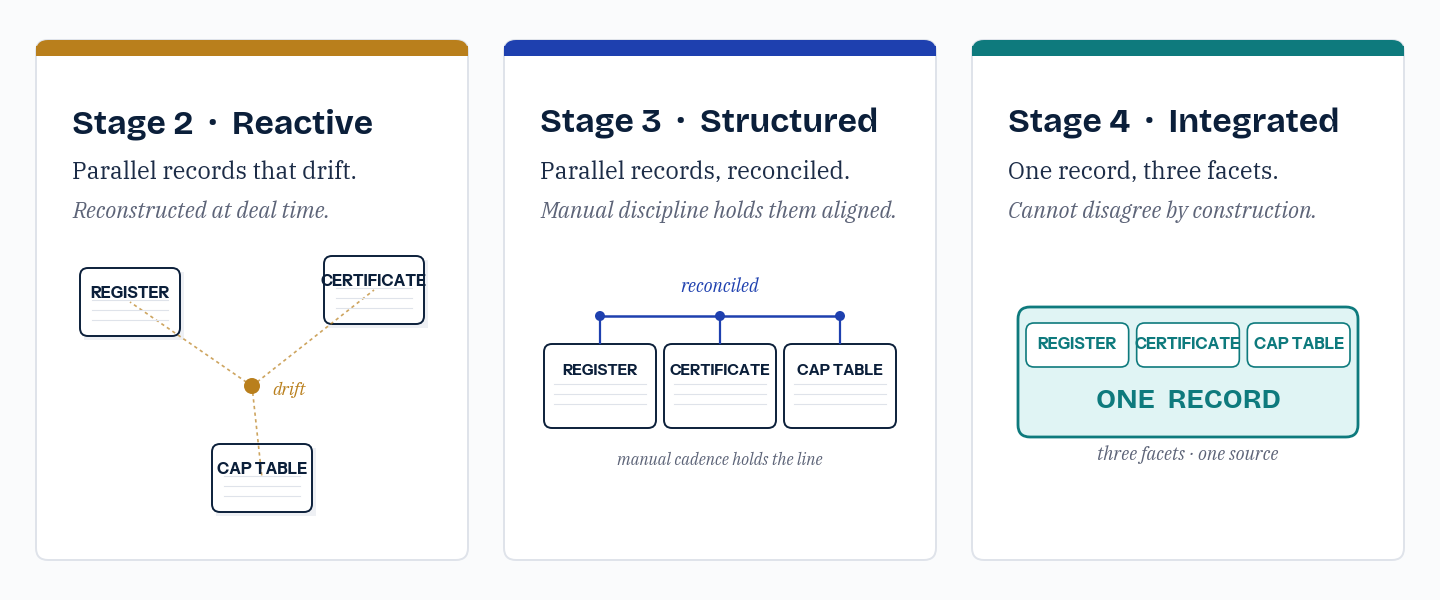

A minute book exists. The share register is maintained as the source of issued shares. Certificates are issued sequentially. Authorizing resolutions are drafted contemporaneously with the decisions they authorize. The corporation has crossed from records-as-byproduct to records-as-discipline, but the discipline is manual.

Observable signals

- A clearly identified minute book holds the corporation's records in chronological order

- The share register and the certificates agree on issued share counts

- Resolutions are drafted within days of the decisions they authorize

- Annual filings are current across all jurisdictions

- Beneficial-ownership filings are current and match the share register

Common failure modes

- The cap table is still maintained separately from the register and may drift between updates

- Certificate verification by third parties requires phone calls or scanned-copy exchanges

- Audit trail is partial; signed documents have signatures but not full creation history

- Transfer-restriction compliance is checked at the time but rarely documented retrospectively

Diligence outcome

Two to six weeks of diligence work. Findings are usually procedural rather than substantive: a missing acknowledgement here, an informal transfer there. The records bundle survives with minor remediation. Most Stage 3 corporations close their first financing without significant diligence friction.

Advancement to Stage 4

Move from parallel records (register and cap table maintained side-by-side) to integrated records (cap table builds from register, transfers update both atomically). Introduce verifiable certificates (QR-linked to the register) and a per-record audit trail. This is the inflection where corporate-records software earns its keep.

A single system of record holds the register, certificates, resolutions, and cap table together, with reconciliation enforced by the system rather than by operator discipline. The corporation can produce a diligence bundle in days, not weeks, because the bundle exists continuously rather than being assembled on demand.

Observable signals

- Register, certificate, and cap table cannot disagree by construction; they are facets of the same record

- Every authorizing resolution traces directly to the action it authorized

- Certificates are verifiable by third parties without contacting the corporation

- Per-record audit trail shows creation, modification, and signature events with timestamps

- Transfer-restriction compliance is enforced by the system on every transfer attempt

Common failure modes

- Multi-entity portfolios (holdco-opco structures, subsidiary chains) maintained in parallel systems lose cross-entity visibility

- Pre-system records (legacy minute book contents from earlier stages) may not be fully migrated and create dual-system risk

- Compliance with jurisdiction-specific filings still requires operator attention; the system reconciles the records but does not necessarily file them

Diligence outcome

One to three weeks of diligence work, with findings typically limited to commercial-judgment items rather than records gaps. Financings, audits, and M&A diligence run on the buyer's timeline rather than the seller's reconstruction speed.

Advancement to Stage 5

Add continuous reconciliation monitoring (alerts when the register and cap table drift, when certificates are not verifiable, when resolutions are pending past their action). Add proactive compliance-calendar enforcement. Reduce data-room production time below 30 days by maintaining the data room continuously.

Records are diligence-ready continuously, not at points in time. The data room exists as a live artifact, refreshed automatically as the corporation operates. Compliance items are tracked and filed proactively. The diligence outcome is predictable in advance because the records are always producible.

Observable signals

- Continuous reconciliation across register, certificates, cap table, and resolutions

- Data room production in under 30 days, with most items available immediately

- Compliance calendar maintained at the corporation level with proactive alerts

- Multi-entity portfolios consolidated under a single integrated view

- Cross-entity dependencies (intercompany agreements, shared directors, ownership chains) explicitly modeled

Common failure modes

- System migrations (changes of provider, mergers between corporations using different systems) can briefly drop the corporation back to Stage 4 during the transition

- Changes in corporate counsel can introduce gaps if the new counsel doesn't engage with the existing system

Diligence outcome

Diligence on records is a verification, not an investigation. Most engagements complete on the buyer's timeline with minimal seller-side work. Stage 5 is the threshold where corporate-records discipline becomes a competitive advantage in dealmaking rather than a cost center.

How to assess your current stage

Pick the stage description that best matches your corporation's current operational reality. The framework is intentionally lenient on transitional cases: a corporation in the middle of advancing from Stage 2 to Stage 3 is most usefully classified as Stage 2 (the prior state) until the advancement is complete and durable.

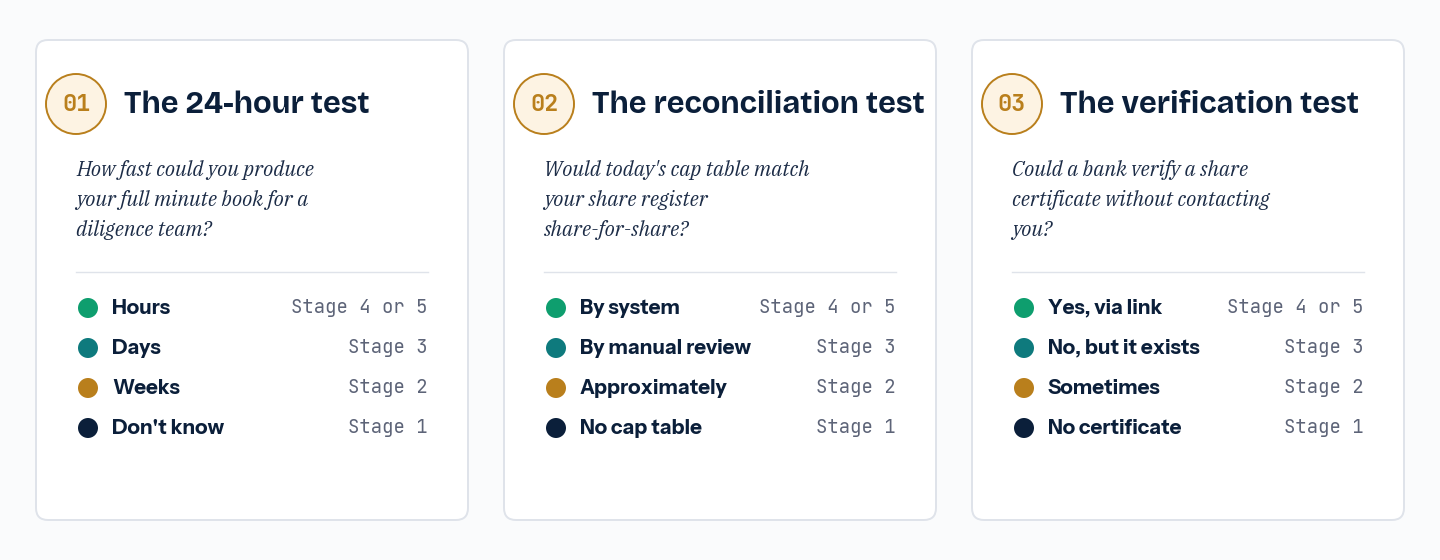

Three quick tests for self-assessment:

- The 24-hour test. If a diligence team asked for your full minute book tomorrow, how long would it take to deliver? Hours: Stage 4 or 5. Days: Stage 3. Weeks: Stage 2. Don't know: Stage 1.

- The reconciliation test. If you generated your cap table today, would it match your share register share-for-share? Yes, by system construction: Stage 4 or 5. Yes, by recent manual reconciliation: Stage 3. Approximately: Stage 2. The cap table doesn't exist: Stage 1.

- The verification test. If a bank asked to verify a share certificate without contacting the corporation, could they? Yes, via a verification link: Stage 4 or 5. No, but the certificate exists: Stage 3. Sometimes: Stage 2. No certificate exists: Stage 1.

For a more structured assessment, the diligence readiness assessment tool produces a per-category score that maps onto the framework: scores below 50% suggest Stage 1 or 2, 50–75% suggests Stage 3, 75–90% suggests Stage 4, above 90% suggests Stage 5. The corporate records health check is a faster but less detailed instrument.

The advancement playbook

Advancement is a project, not a posture. Each stage transition requires specific operational work, organized below as a sequenced playbook. The cost estimates are illustrative; jurisdiction, corporation size, and counsel choice all vary.

Stage 1 → Stage 2

- Engage corporate counsel to draft foundational documents (typically $2,000–$8,000)

- Articles certified by the registry; bylaws drafted; founder restricted-stock purchase agreements signed; consideration paid; 83(b) elections filed where applicable

- Initial board resolution covering officer appointments and any prior actions

- Share register seeded with founder issuances

- Typical duration: 2–4 weeks

Stage 2 → Stage 3

- Reconcile the share register to existing certificates, line by line; resolve any discrepancies in counsel

- Rebuild the cap table from the register and the schedule of outstanding options, warrants, SAFEs, and notes

- Surface and ratify any missing authorizing resolutions (officer appointments, share issuances, option grants)

- Bring all annual filings and beneficial-ownership filings current

- Establish a monthly or quarterly cadence for updating the register, cap table, and minute book

- Typical duration: 6–12 weeks

Stage 3 → Stage 4

- Move to integrated corporate-records software where the register, certificates, cap table, and resolutions live as facets of a single record

- Migrate the historical minute book contents into the system as a starting point

- Introduce verifiable certificates (QR-linked to the register) for new issuances and any reissuances

- Configure per-record audit trail with creation, modification, and signature timestamps

- Configure transfer-restriction enforcement so that restricted transfers cannot be registered without satisfaction

- Typical duration: 4–8 weeks (migration is the main constraint)

Stage 4 → Stage 5

- Configure continuous reconciliation alerts at the system level (drift between register and cap table, pending resolutions, expiring filings)

- Maintain the data room as a live artifact rather than an event-driven one

- For multi-entity portfolios, consolidate cross-entity visibility (intercompany agreements, shared directors, ownership chains)

- Operationalize the compliance calendar with proactive alerts at the corporation level

- Typical duration: ongoing operational discipline, not a discrete project

The eight procedure guides in How-to guides document the operational moves underlying each stage transition: issuing shares, transferring shares, passing resolutions, running annual meetings, and preparing for diligence.

Methodology and limitations

This framework is taxonomic rather than empirical. It describes observable stages and the work required to move between them; it does not claim a statistical distribution of corporations across stages, nor predict the probability of any specific corporation occupying any specific stage.

The framework's stage definitions are derived from observable patterns in private-corporation records work across Canadian, US, and UK jurisdictions, organized for analytical clarity rather than empirical fit. Different observers familiar with the same patterns might draw the boundaries differently; the framework's structure is one defensible choice, not the only one.

The framework deliberately omits stages above Stage 5. Corporations that achieve and sustain Stage 5 sometimes go further into proactive governance design, automated compliance verification, and continuous-audit posture. These higher states are real but uncommon enough that a five-stage model captures the operationally important distinctions for the population of private corporations the framework is intended to serve.

The framework also omits a treatment of public-company records. Public companies operate under additional disclosure regimes (SEC, OSC, FCA) that materially change the cost-benefit structure and the operational requirements. A public-company-adapted maturity framework would share the underlying structure but would require additional dimensions (disclosure controls, segregation of duties, audit committee oversight) that are not addressed here.

Frequently asked

Is this maturity model based on a survey?

No. It is a framework derived from observable patterns in private-corporation records work, organized into a five-stage progression. It is meant as a reference taxonomy for assessing where a corporation currently stands and what advancement to the next stage requires, not as a statistical claim about the distribution of corporations across stages.

How is this different from a diligence checklist?

A diligence checklist enumerates the documents and verifications a diligence team performs. The maturity framework characterizes the operational discipline a corporation has built; the same corporation may pass any given checklist item by chance, or by sustained practice. The framework focuses on the systemic state, the checklist on the immediate output.

Which stage do most private corporations occupy?

In our experience working across the private-corporation lifecycle, Stage 2 is by far the most populous, with Stages 1 and 3 a distant second tier. Stage 4 and Stage 5 are rare among early-stage and small private corporations and become more common in corporations that have completed at least one financing round and engaged corporate counsel sustainably. This pattern reflects the historical reality that records discipline is rewarded only intermittently (at transactions), not the underlying difficulty of advancing.

Can a corporation skip stages?

Yes, particularly Stage 2. A founder who incorporates with counsel and chooses a structured records system at formation can pass directly from Stage 1 to Stage 3 or even Stage 4. The reverse is rarer; corporations at Stage 4 or 5 generally retain those properties unless an acquisition or change of counsel disrupts them.

Does Stage 5 require software?

Practically, yes. The defining attributes of Stage 5, continuous reconciliation across register-certificate-cap-table-resolutions, sub-30-day data room production, and a complete audit trail per record, are achievable in a structured manual system in principle but require unsustainable effort in practice. Most Stage 5 operators use purpose-built corporate-records software.

How should I use this framework with my board or counsel?

Use it as a shared vocabulary. The framework gives a board, counsel, and operator team a way to agree on the corporation's current stage and what advancing one stage would cost in time and discipline. The advancement playbook is intended to be operationalized as a quarterly or annual project plan, not consumed as a passive reference.

Suggested citation: Octelligence Research, The Corporate Records Maturity Framework, February 2026. Available at octelligence.com/global/en/research/corporate-records-maturity-framework/.

Octelligence is built for the Stage 3-to-Stage 4 transition: register, certificate, cap table, and resolutions as a single integrated record, with QR-verified certificates and a per-record audit trail.