The Diligence Failure Taxonomy

Seven structured ways corporate records fail under diligence. For each: the conditions that produce the failure, the documents that betray it, the typical remediation path, and the diligence outcome if remediation isn't possible in time. A companion reference to the Corporate Records Maturity Framework.

Executive summary

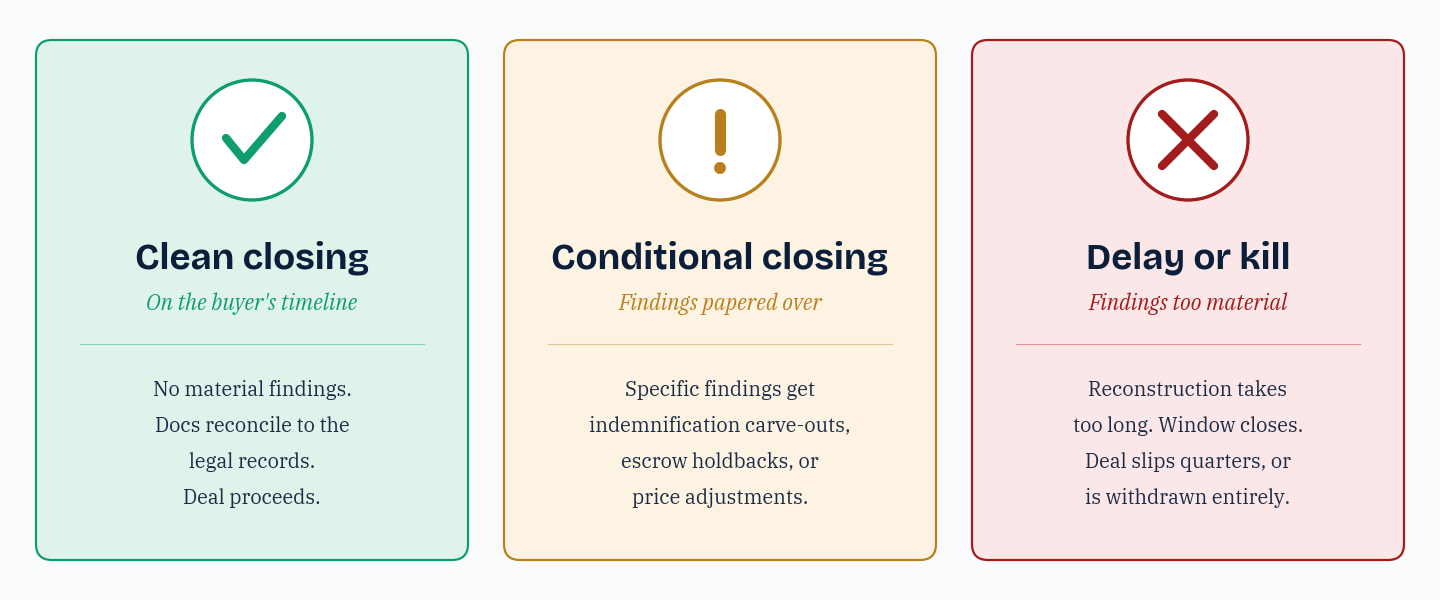

Diligence engagements end in one of three places: clean closing on the buyer's timeline, conditional closing with indemnification carve-outs or escrow holdbacks tied to specific findings, or transaction delay or kill from a finding too material to paper over. The findings that produce each outcome are not uniformly distributed. A small number of failure patterns explain most observed bad outcomes.

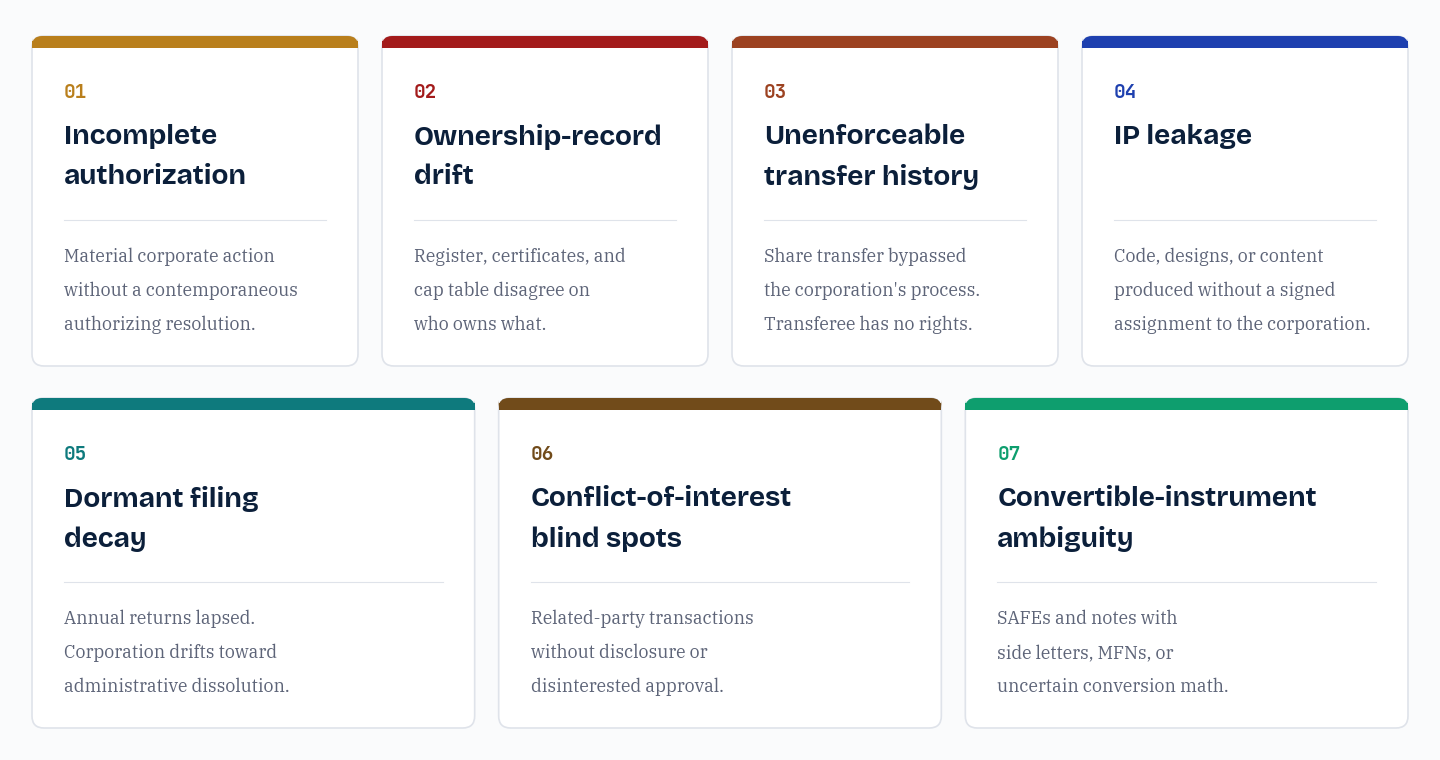

The Diligence Failure Taxonomy organizes those patterns into seven categories: incomplete authorization, ownership-record drift, unenforceable transfer history, intellectual-property leakage, dormant filing decay, conflict-of-interest blind spots, and convertible-instrument ambiguity. Each is a category, not an instance. The same corporation can host more than one; corporations at lower stages of the Corporate Records Maturity Framework tend to host most of them.

The value of a taxonomy is in pattern recognition. A diligence team that has seen the failure modes can identify them quickly. A corporation that has read the taxonomy can self-diagnose ahead of an engagement. The goal of this document is to make both groups faster at the same recognition.

The seven categories

Each entry below names the failure mode, describes the conditions that produce it, identifies the documents that surface the failure in diligence, and outlines the typical remediation path and outcome.

A material corporate action was taken without a contemporaneous authorizing resolution. The action stands operationally but lacks the legal evidence of board approval that diligence counsel requires. The most common version is option grants without resolutions.

Producing conditions

- Corporation operates with informal board governance during early stages

- Founder-CEO holds all roles and decisions are made unilaterally

- Counsel was not retained, or was used only for incorporation, not ongoing matters

- Board met but minutes were never drafted, or were drafted in summary form without operative resolutions

Surfacing documents

- Option-grant agreement with a grant date, but no board resolution at that date

- Officer signing material contracts without a resolution appointing them as officer

- Share issuance entered in the register without a corresponding authorizing resolution

Remediation

Ratifying resolutions executed by the current board, referencing the original decision date. Legally effective in most jurisdictions, but visibly retroactive and reduces counsel trust. Better than no resolution; far weaker than a contemporaneous one.

Outcome

If remediation is complete before closing, the deal generally proceeds. If multiple resolutions need ratification, the volume itself becomes a signal of poor governance and may reduce commercial terms (lower valuation, larger indemnification cap, longer survival period).

The share register, the issued certificates, and the cap table disagree on who owns what. Each artifact has its own internal consistency; reconciliation across all three reveals discrepancies that cannot be resolved without going back to the underlying authorizing documents.

Producing conditions

- Cap table maintained in a spreadsheet, separately from the register

- Certificates issued but the register was never updated, or vice versa

- Share counts adjusted in the cap table without a corresponding transfer or issuance event

- Founder shares issued at incorporation but registered later, with the dates drifting

Surfacing documents

- Certificate showing 1,000,000 shares; register entry showing 950,000 for the same holder on the same date

- Cap table reflecting an option pool of 1.5M shares; the board resolution authorizes 1.2M

- Fully-diluted percentages in the cap table that don't sum to 100% when computed independently

Remediation

Walk each line: register entry, certificate, cap table line, authorizing resolution. Identify which source is authoritative for each disagreement (the register controls under most corporation statutes; the resolution controls the register). Issue corrective resolutions and reissue certificates where needed. Expensive in time and counsel hours.

Outcome

Reconciliation is almost always achievable; the question is timing. A diligence engagement that begins with the corporation discovering drift mid-process risks delayed closing or, in fast-moving markets, lost deal terms when reconciliation extends past committed timelines.

A share transfer occurred between shareholders without going through the corporation's process. Old certificate not cancelled. Register not updated. Transfer restrictions in the shareholders' agreement not honoured. The corporation continues to treat the registered holder as the shareholder; the actual transferee has no rights against the corporation.

Producing conditions

- Founder transfers shares to a holdco or family trust without notifying the corporation

- Employee terminates and "sells" vested shares to a fellow employee without going through the company

- Shareholder dies; estate transfers shares to heirs without documenting the transfer

- Shareholder agreement requires ROFR offer; the offer was never made

Surfacing documents

- A current shareholder appears in correspondence but not on the corporation's most recent register

- Beneficial-ownership filing identifies an individual not on the share register

- The shareholders' agreement is dated 2018 with 5 signatories; the register shows 9 current holders

Remediation

For each informal transfer, reconstruct what happened, get the parties to ratify the transfer through proper documentation (stock power, board approval where required, certificate cancellation and reissuance), and update the register. Where transfer restrictions were not honoured, get written waivers from the parties whose rights were skipped, or unwind the transfer.

Outcome

Often the most painful failure mode because reconstruction requires cooperation from multiple parties who may no longer be aligned with the corporation. Buyers may require an indemnification carve-out for unrecovered transfer risk, or escrow holdbacks until each informal transfer is cleaned up.

Pre-formation IP wasn't assigned to the corporation. Or it was assigned but for inadequate consideration. Or an early contributor (advisor, contractor, co-founder who left) holds IP the corporation depends on. The corporation may not own its core technology.

Producing conditions

- Founders built the initial product before incorporating

- IP assignment language was missing from the founder restricted-stock purchase agreement

- Early contractor agreements lacked work-for-hire or assignment provisions

- A co-founder departed; the separation didn't include explicit assignment of contributed IP

Surfacing documents

- Founder RSPA without an IP assignment clause

- Early contractor invoices but no signed assignment or NDA

- Email or commit-log evidence of code or design contributions from someone who never signed an IP agreement

Remediation

Chase down each contributor and obtain a signed assignment retroactively, with stated consideration. For absent or uncooperative individuals, negotiate a quitclaim or settlement. In severe cases, refactor the affected code or design to remove the contested contributions, which is expensive and time-consuming.

Outcome

For technology companies, IP leakage is the single most likely failure mode to kill a transaction outright. Acquirers in particular are unwilling to assume ownership of technology with uncertain provenance. Smaller leakage can be addressed with indemnification; material leakage often cannot.

Annual returns missed in one or more jurisdictions. Beneficial-ownership filings out of date. Foreign qualifications lapsed. Securities filings missed for past private placements. Each individual miss is recoverable; the cumulative effect is a corporation that may technically be dissolved or out of compliance in ways the management team doesn't know.

Producing conditions

- Corporation operates across multiple jurisdictions but didn't track foreign-qualification deadlines

- Change of corporate counsel or accountant created a handoff gap on compliance tracking

- FinCEN BOI requirement took effect in 2024; corporation never registered or stopped updating

- Multi-entity portfolio has uneven compliance discipline across subsidiaries

Surfacing documents

- Registry record showing "in default" or "dissolved for non-filing" status

- Most recent annual return dated several years prior

- Director listed on the corporate registry is no longer with the corporation

Remediation

File the catch-up returns with associated late fees. Reinstate dissolved entities through registry-specific procedures (which can take weeks). Bring beneficial-ownership filings current. Most jurisdictions accept retroactive compliance with penalty fees.

Outcome

Filing decay rarely kills transactions but routinely delays them. The reinstatement timeline becomes the closing timeline for affected jurisdictions. The cumulative late fees can be substantial; the reputational cost with diligence counsel is more material.

A director or officer had a material interest in a corporate transaction; the interest wasn't disclosed, or the conflicted person voted, or the transaction wasn't approved by a disinterested-director or shareholder vote. The resulting contract may be voidable. Often discovered when the acquirer's counsel maps the corporation's contracts against the directors' other affiliations.

Producing conditions

- Director also owns or works for a vendor or customer

- Officer holds shares in an entity the corporation contracts with

- Founder owns the building the corporation leases from

- Conflicts disclosure regime wasn't enforced; no formal conflicts register exists

Surfacing documents

- Vendor invoices where the vendor entity shares an officer with the corporation

- Lease agreement where the landlord is a related party

- Board minutes that don't record any conflicts disclosures over many years of operation

Remediation

Each conflicted transaction needs to be either ratified by disinterested directors or shareholders (after retroactive disclosure), shown to be fair to the corporation on independent evidence, or unwound. In some jurisdictions, retroactive ratification by disinterested parties is legally effective; in others, the transaction may need to be rescinded and re-negotiated.

Outcome

Conflict failures are often quietly material. Buyers may add specific representations about the absence of related-party transactions, with indemnification carve-outs sized to the value of the contested contracts. In serious cases (related-party leases priced above market, or insider self-dealing), the transaction may not close.

SAFEs, convertible notes, and warrants are on the cap table but the conversion mechanics aren't clear. Multiple SAFEs at different valuation caps stack ambiguously. Notes have interest accrual that wasn't tracked. Warrants have anti-dilution adjustments that weren't applied to prior rounds. The fully-diluted cap table cannot be computed deterministically.

Producing conditions

- Corporation raised multiple SAFE rounds at different terms without modeling conversion

- Convertible notes accrued interest that was never added to the principal in the cap-table tracking

- Warrants with cashless-exercise provisions that depend on a future fair-market value

- Anti-dilution provisions in earlier rounds that have triggered but weren't applied

Surfacing documents

- Cap table that doesn't include a conversion-modeling tab

- SAFE side-letters that aren't reflected in the standard SAFE terms

- Most-favored-nation clauses that have been triggered by later rounds but not propagated backward

Remediation

Build a deterministic conversion model for each instrument under each conversion scenario (priced round, acquisition, liquidation). Have counsel walk every side letter and MFN provision. Update the cap table with computed conversion-event share counts. Provide the model and source documents to the acquirer's diligence team.

Outcome

Diligence can usually resolve convertible ambiguity in days to a couple of weeks, with counsel involved. The risk is closing-price uncertainty: an acquirer wants to know exactly what they're buying, and ambiguity in the cap table directly affects the per-share price. Material ambiguity often results in escrow holdbacks tied to post-closing cap-table verification.

How the failures cluster

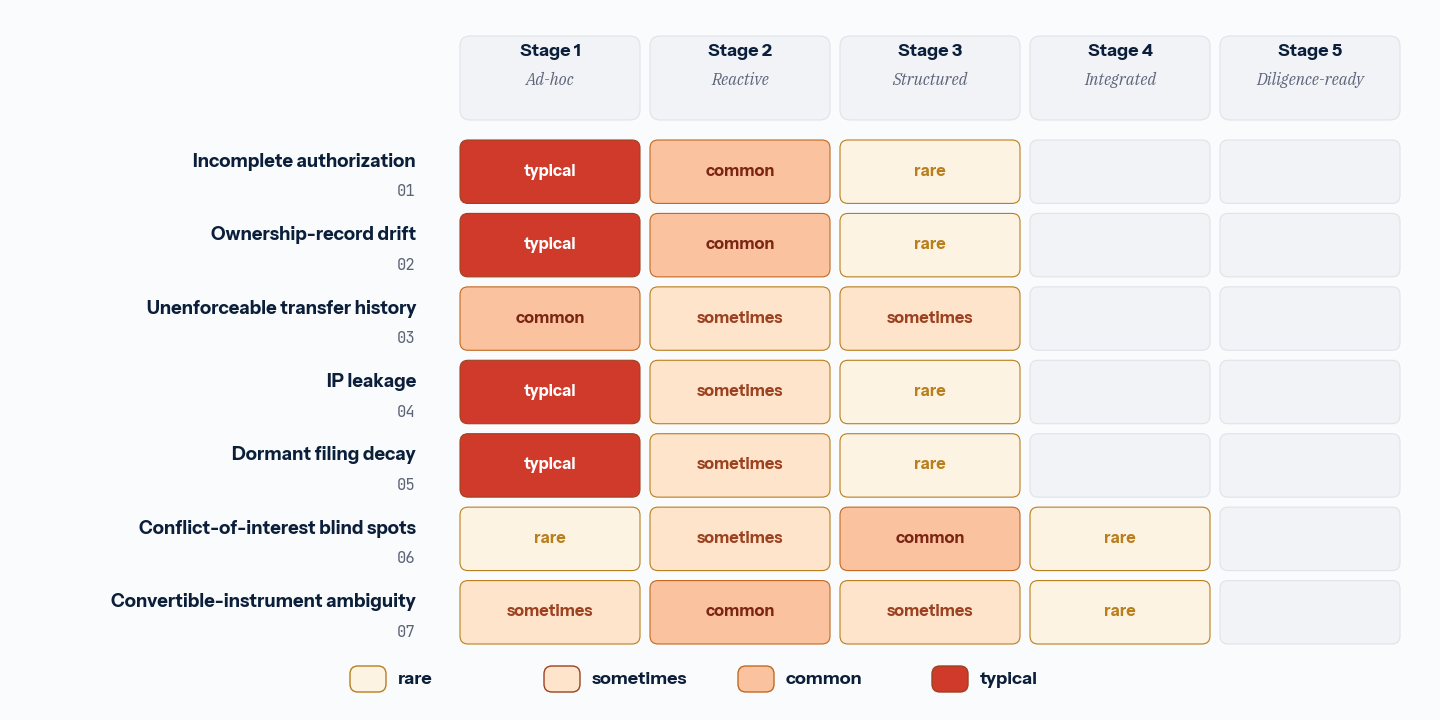

The seven categories are conceptually independent but practically correlated. Failures 1, 2, and 7 tend to co-occur: a corporation that doesn't draft contemporaneous resolutions also tends to maintain an ad-hoc cap table that doesn't model convertibles. Failures 3, 4, and 5 co-occur differently: corporations operating without sustained corporate-counsel engagement tend to host all three. Failure 6 is the outlier and depends on the specific composition of the board.

Mapped to the Corporate Records Maturity Framework: corporations at Stage 1 typically host failures 1, 2, 4, and 5 simultaneously. Stage 2 corporations typically host 1, 2, and 7. Stage 3 corporations may host failure 6 (because they have formal board structure but inconsistent conflicts discipline) and residual cases of failure 3 from earlier stages. Stage 4 and 5 corporations rarely host any of the seven failures in a material form.

Self-diagnosis

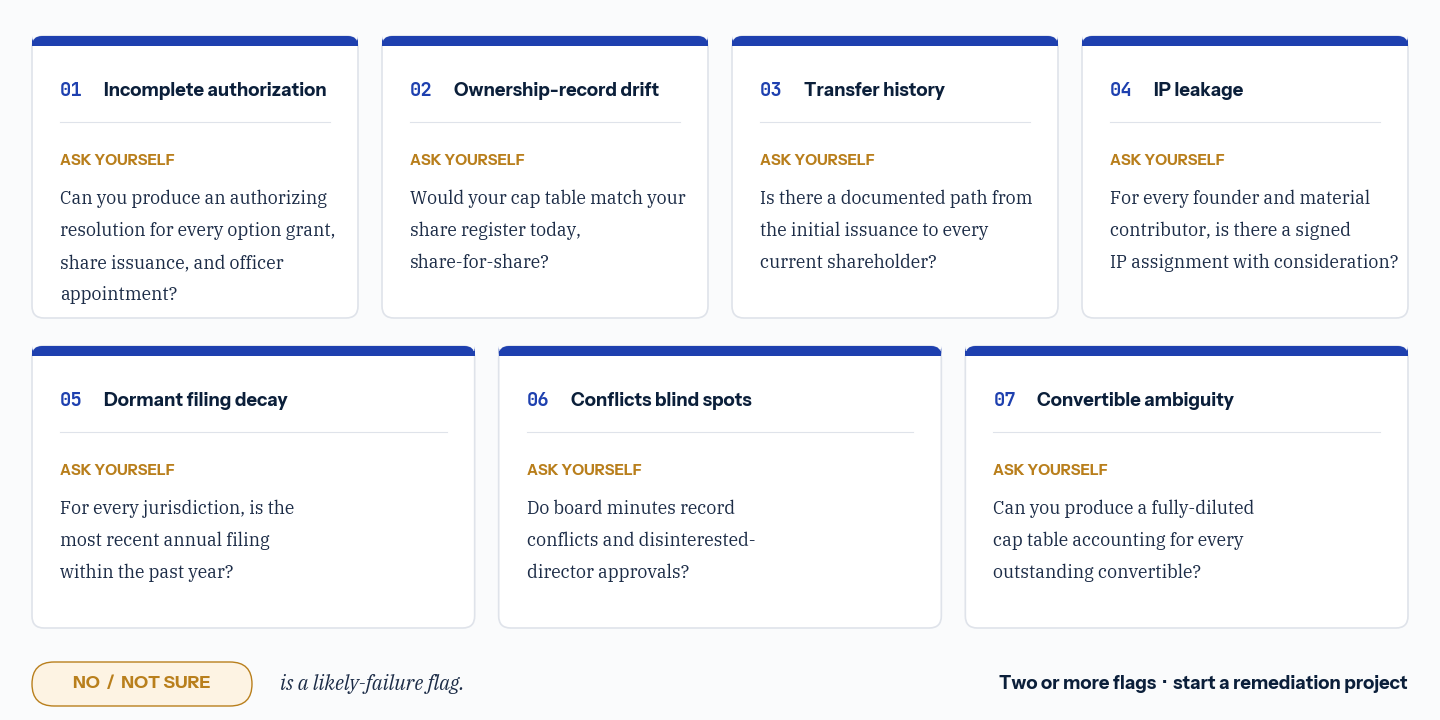

For each of the seven categories, the diagnostic questions a corporation can answer for itself:

- Failure 1. Can you produce an authorizing resolution for every option grant, every share issuance, and every officer appointment in the corporation's history?

- Failure 2. If you generated your cap table today, would it match your share register on the current date, share-for-share?

- Failure 3. For every shareholder on your current register, is there a documented path from the corporation's initial issuance to the current ownership?

- Failure 4. For every founder and every material contributor, is there a signed IP assignment with stated consideration?

- Failure 5. For every jurisdiction the corporation is incorporated or qualified in, is the most recent annual filing within the past year?

- Failure 6. Do your board minutes record conflicts disclosures, and for every related-party transaction, is there evidence of disinterested-director approval or fairness?

- Failure 7. Can you produce a fully-diluted cap table that accounts for every outstanding convertible under defined conversion assumptions?

A "no" or "not sure" answer to any of these is a likely-failure flag. Two or more flags suggests a remediation project before the next financing or M&A engagement opens. The Diligence Readiness Assessment tool covers these questions in structured form with category-level scoring.

Conclusion

The seven failure modes are not exhaustive. Specific industries (regulated financial services, healthcare, defense) layer on industry-specific compliance failures. International corporations layer on cross-border regulatory failures. But across the population of private corporations served by general corporate-records discipline, the seven categories cover the substantial majority of bad diligence outcomes.

The point of naming them is to make recognition faster. A diligence team that sees a missing resolution recognizes failure 1 and asks for the remediation. A corporation that has read the taxonomy can run failure-mode-by-failure-mode self-diagnosis ahead of an engagement and address what it finds. Both groups are better served by a shared vocabulary.

Suggested citation: Octelligence Research, The Diligence Failure Taxonomy, April 2026. Available at octelligence.com/global/en/research/diligence-failure-taxonomy/.

Octelligence's structured records make most of the seven failure modes unreachable: every action has its authorizing resolution; register, certificates, and cap table cannot disagree; transfers go through the system or they don't go through.