How to plan an option pool

The option pool is the corporation's reserve of shares authorized for grant to employees, contractors, advisors, and (sometimes) directors. Sizing it is a balance: too small, and the corporation runs out of grant capacity and faces a pre-money top-up at the next round (which dilutes founders); too large, and the pool sits with unused capacity that suppresses founder ownership unnecessarily. Most corporations get the sizing roughly right once they connect the pool to a real hire plan.

| When | At incorporation and at each priced financing round (top-up) |

|---|---|

| Sizing basis | Hire plan for the next 18-24 months, plus a buffer |

| Documents produced | Equity incentive plan, board resolution reserving the pool, grant tracking |

| Top-up convention | Pre-money at financings: existing holders absorb the dilution |

- Size the pool from a hire plan with grant percentages per role, not from a rule of thumb

- Reserve the pool in the equity incentive plan with board approval; some jurisdictions also require shareholder approval

- The pool size is the maximum that can be granted; actual outstanding grants are typically lower

- At each priced financing, the pool is topped up pre-money (existing holders absorb the dilution)

- Unused pool capacity reverts to the corporation at exit or plan termination

On this page

Steps

Build the hire plan

Start from the operating plan: what roles is the corporation hiring in the next 18-24 months? For each role, what equity grant is competitive at the role's level and the corporation's stage? A common starting framework: C-level non-founder hires get 1-5% (post-Series A); VP-level get 0.5-2%; director-level get 0.2-0.7%; senior IC get 0.1-0.4%; mid-level IC get 0.05-0.15%. The exact percentages vary widely by sector, stage, and location. Sum the grants needed across the planned hires.Size the pool with a buffer

Sum the planned grants from the hire plan. Add a buffer of 15-25% for hires that aren't yet on the plan but will appear (executive substitutions, performance-driven supplemental grants, advisor grants). The resulting number is the target pool size, expressed as a percentage of post-money fully-diluted at the next financing event. Typical Series A target pools are 10-15% of post-money fully-diluted; pre-Series A pools are often smaller and topped up at Series A.Adopt the equity incentive plan

The board adopts an equity incentive plan that sets the pool size, the types of grants permitted (ISOs, NSOs, restricted stock), the vesting terms typically applied, and the administrative provisions. In most jurisdictions, the equity incentive plan needs both board and shareholder approval, especially if it permits ISOs (which require shareholder-approved plans under IRC § 422).Reserve the pool shares

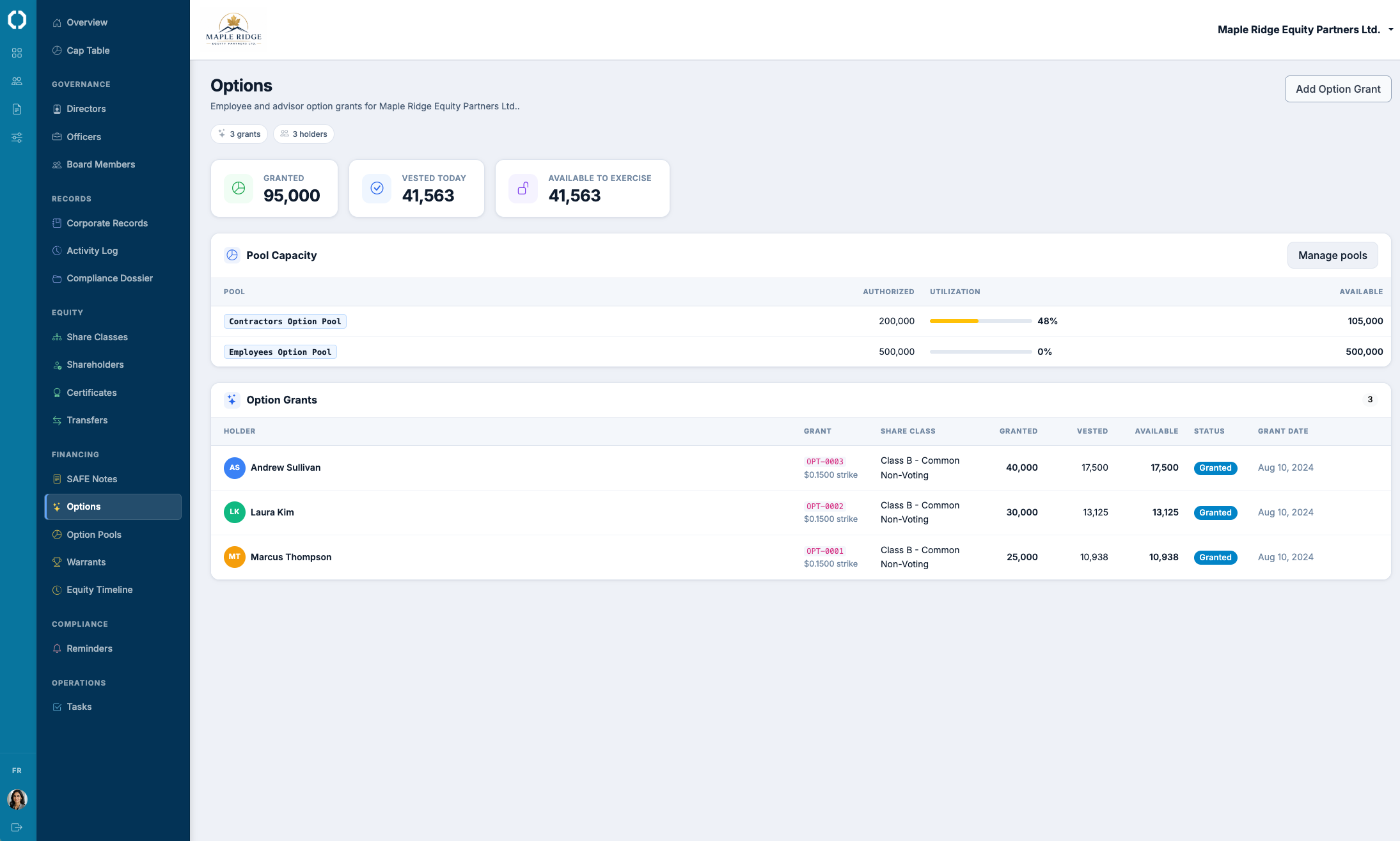

The shares reserved under the plan are typically authorized-but-unissued shares of common stock. The board resolution adopting the plan increases the number of shares reserved for issuance under the plan. In some structures, the plan reserves a percentage rather than a fixed number, but fixed numbers are more common and operationally simpler.Track grants against the pool

Every option grant draws from the pool. The corporation tracks: the total pool size, the cumulative shares granted, the cumulative shares exercised, the cumulative shares forfeited (returned to the pool), and the resulting available-for-grant balance. The board approves each grant individually (or a slate of grants); see pass a board resolution for the resolution mechanics. Grants without contemporaneous board resolutions are the most common option-pool failure mode in diligence.Top up the pool at the next financing

At the next priced financing, the investor typically requires the pool to be increased to a target percentage of post-money fully-diluted (commonly 10-15%). The top-up is, by convention, pre-money: existing holders (founders, prior investors) absorb the dilution from the new pool, not the new investor. This is a meaningful component of founder dilution at a priced round and should be modeled before signing the term sheet. See run a priced round for the closing mechanics.

Common mistakes

- Pool sized by rule of thumb rather than hire plan. Founders pick a 10% pool because "that's what people do." When the hire plan demands 14% over the period to the next round, the pool runs out and a mid-period top-up is needed, with a dilution event the founders didn't anticipate.

- Grants without contemporaneous board resolutions. Options are promised to a new hire on Day 1. The board resolution is supposed to be drafted but isn't. Six months later, the diligence team asks for the grant resolution. Now the corporation needs a ratifying resolution that retroactively approves a grant with a strike price (which under 409A requires the strike price to reflect FMV at the grant date, not the ratification date). This is unwinding work that's expensive to redo.

- Strike prices not refreshed against 409A valuations. Each grant's strike price must equal or exceed FMV at the grant date. FMV is determined by a 409A valuation that's refreshed at least every 12 months or after a material event (priced round). If the 409A is stale, the strike price may be too low, triggering tax penalties. Refresh the 409A at the right cadence and use the current valuation for each grant.

- Mixing grant types incorrectly. ISOs and NSOs have different tax treatments and eligibility (ISOs require employee status, $100k/year vesting cap, etc.). Granting ISOs to contractors or above the $100k limit converts them to NSOs by operation of law, often unexpectedly. The grant tracking should distinguish ISO from NSO and respect the eligibility rules.

Octelligence tracks the option pool with every grant tied to a board resolution, every strike price tied to a 409A valuation, and every forfeiture flowing back to the available-for-grant balance. The pool reconciles to the cap table automatically.

See Cap Tables & FinancingCommon questions

Sized from the hire plan, tracked against board resolutions, refreshed at the right 409A cadence, and reconciled to the cap table on every grant.