How to grant stock options

An option grant is not a promise in an offer letter. It is a board action with a strike price set on a specific date against a specific 409A valuation, recorded in the option ledger and reflected in the cap table on the same day. The procedure below documents the steps that turn a hiring commitment into a defensible, diligence-ready grant.

| When | On the date of the board resolution authorizing the grant |

|---|---|

| Authorized by | The board of directors, under a shareholder-approved equity plan |

| Strike price | At least the fair market value on the grant date (409A in the US) |

| Recorded in | Option ledger, cap table, board minutes, plan rollforward |

- The grant date is the date of the board resolution, not the offer letter or start date

- The strike price must equal the 409A fair market value on the grant date

- ISO designation has specific eligibility conditions; defaults to NSO if any condition fails

- Options are tracked in the option ledger and represented on the cap table as outstanding, not issued, equity

- Grants beyond the available pool are not effective until the pool is increased

On this page

Steps

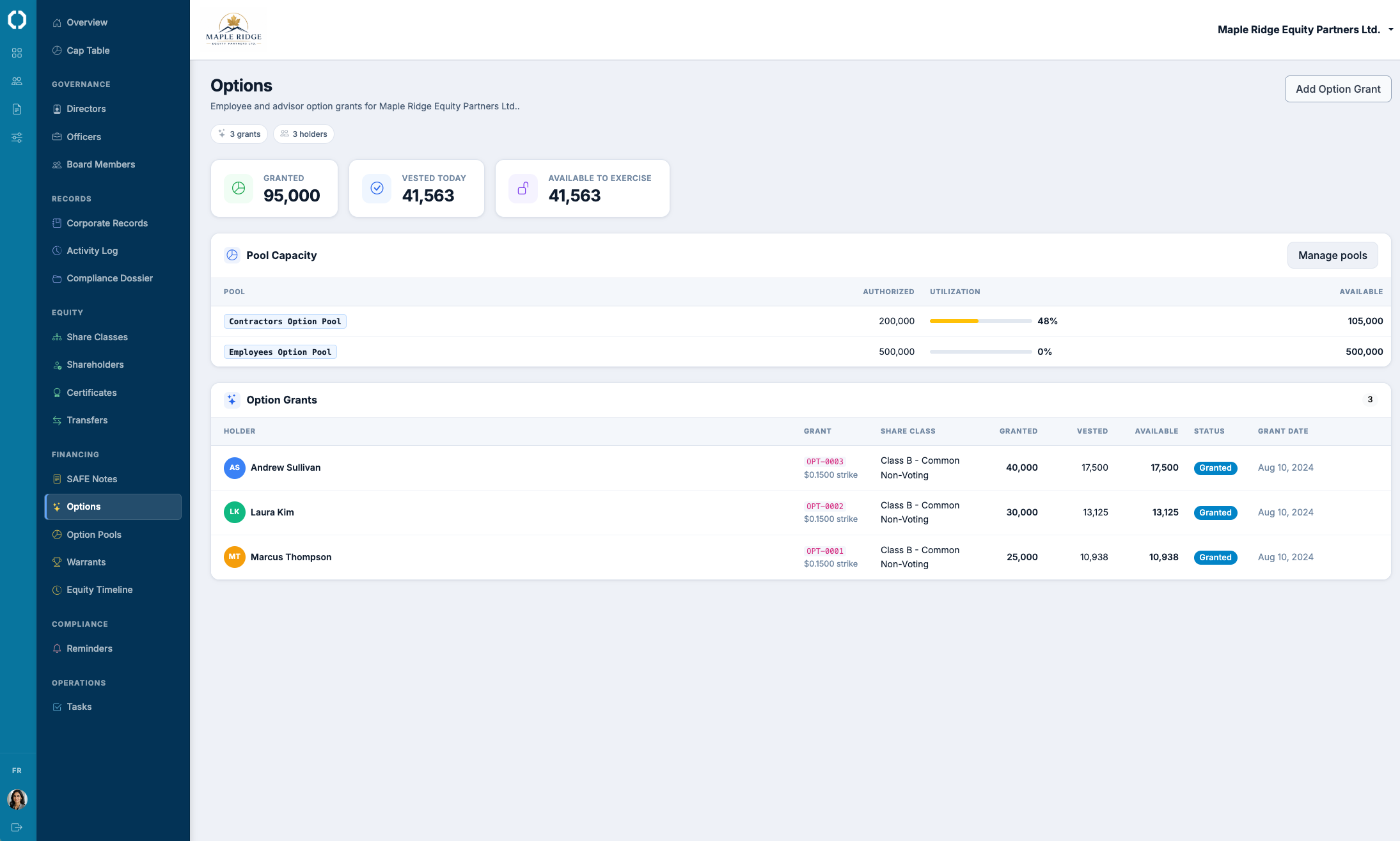

Confirm the option pool has sufficient unissued shares

Before any grant can be authorized, the option pool must have enough unissued (and unforfeited) shares available to cover the grant. The available pool is the authorized pool less the sum of outstanding grants and exercised options. Granting beyond the available pool is void until the pool is increased, which requires board (and usually shareholder) approval to amend the plan. See how to plan an option pool for sizing decisions.Obtain a current 409A valuation

The strike price of an option granted to a US taxpayer must be at least the fair market value of the underlying share on the grant date. For a private corporation, fair market value is established by a 409A valuation prepared by a qualified independent appraiser. The valuation must be current: typically valid for twelve months, or until a material event (priced round, secondary, business change). Granting at a strike below the 409A fair market value triggers immediate income inclusion and a 20% additional tax under Internal Revenue Code section 409A.Pass the board resolution authorizing each grant

Each grant is authorized by board resolution. The resolution names the grantee, the number of options, the strike price (equal to the 409A fair market value), the vesting schedule, the grant date, the expiration date (typically ten years), and the designation as an incentive stock option (ISO), non-qualified stock option (NSO), or the non-US equivalent. The grant date is the date of the resolution, not the date of the offer letter or the date the agreement is countersigned. See how to pass a board resolution for the full board action.Designate the option type and document the eligibility rules

For US grants, the ISO designation requires the grantee to be an employee (not a contractor or director), the strike price to equal the 409A fair market value, the annual vesting value not to exceed $100,000 per grantee, and the grant to be made under a shareholder-approved plan. Options that fail the ISO conditions are treated as NSOs by default. For Canadian grants, the section 7 stock option deduction and the favourable capital-gains-equivalent treatment depend on the grant terms (employee status, strike price relationship to fair market value, share class qualifying as a prescribed share). For UK grants, the favoured tax treatment depends on whether the option qualifies as EMI, CSOP, or unapproved. See the ISO/NSO designation tool for the US categorization logic.Issue the grant notice and stock option agreement to the grantee

After the board resolution, the corporation issues a grant notice to the grantee that states the grant date, the number of options, the strike price, the vesting schedule, the expiration date, and the option type. The grant notice attaches the stock option agreement (the contract governing exercise, termination, change-of-control treatment, and other terms) and the equity incentive plan. The grantee countersigns to accept the grant. See the option grant notice template.Record the grant in the option ledger and the cap table

The grant is recorded in the option ledger on the grant date. The ledger entry includes the grantee, the grant date, the strike price, the number of options, the vesting schedule (commencement date, cliff, vesting frequency, total period), the expiration date, the option type (ISO/NSO/EMI/etc.), and a reference to the board resolution. The cap table reflects the grant as an outstanding option, distinct from issued shares. The option pool's available balance is decremented by the grant.Track vesting, exercises, and terminations against the ledger

From the grant date forward, the ledger tracks vesting accrual against the schedule, exercises against the vested-and-unexercised balance, and post-termination exercise windows when an employee leaves. Each exercise issues shares against the option, reducing the outstanding option count and the option pool's exercised balance. Forfeitures (unvested options on termination) return shares to the pool. See how to exercise stock options for what happens on exercise.

Jurisdiction notes

The grant mechanics are similar everywhere; the tax treatment is jurisdiction-specific:

- Delaware (DGCL). Options issued under DGCL § 157, which authorizes the board to issue rights and options to acquire stock. Consideration is governed by § 152 (sufficiency determined by the board). Plan approval and shareholder approval are corporate-law conditions for ISO qualification under IRC § 422. View jurisdiction guide

- California. Option grants to California employees are subject to Section 25102(o) of the California Corporate Securities Law of 1968, which exempts most grants from qualification if specific conditions are met (plan approval, eligibility limits, post-termination exercise window of at least 30 days for termination without cause or 6 months for death/disability). View jurisdiction guide

- Canada (CBCA). Options issued under CBCA s. 25 (issuance authority). Taxation of employee stock options under Income Tax Act s. 7. The 50% stock option deduction applies subject to the prescribed-share rules and the $200,000 annual vesting cap for non-CCPCs (CCPC options have separate, more favourable treatment). View jurisdiction guide

- Ontario (OBCA). Issuance under OBCA s. 25. Taxation parallel to federal (Income Tax Act s. 7). Ontario-incorporated CCPCs benefit from the CCPC stock option rules in the same way as federal corporations. View jurisdiction guide

- United Kingdom. Option grants must respect the share allotment authority under Companies Act 2006 s. 549 and pre-emption rights under s. 561 (typically disapplied for the option pool by special resolution). EMI options under ITEPA 2003 Sch. 5 provide the most favourable tax treatment for qualifying smaller companies; CSOP under Sch. 4 is the alternative for non-EMI-eligible grants; unapproved options have no statutory tax relief. View jurisdiction guide

Common mistakes

- Granting before a current 409A is in place. The offer letter promises options and the start date passes. Months later the board "approves" the grant and backdates it to the start date. The strike price set on the start date is now below a 409A valuation that has moved up. The grant is a 409A violation by construction.

- Treating the offer letter as the grant. The offer letter says "10,000 options at the next board approval." HR considers this the grant. The grantee considers this the grant. The board doesn't formally act for six months. The grant date is the board resolution date, not the offer letter date, and the intervening 409A drift is the grantee's tax problem.

- ISO designation without checking eligibility. The grant is marked ISO, but the grantee is a contractor, or the annual vesting value exceeds $100,000, or the plan has not been shareholder-approved. The grant is treated as an NSO by operation of law, but the option agreement and the grantee's tax return disagree.

- Grant not recorded in the option ledger. The board approves the grant. The grant notice is sent. No one updates the option ledger or the cap table. The pool's available balance still reflects the pre-grant figure. The next grant exceeds the pool without anyone noticing.

- Vesting schedule disagrees across documents. The board resolution says "four years, one-year cliff, monthly thereafter." The option agreement says "four years, quarterly." The ledger says "four years, monthly with no cliff." When the grantee leaves at month 13, three different vested balances are calculable.

Octelligence records each grant against the authorizing resolution, the 409A in effect on the grant date, and the option pool balance at the time. Vesting, exercises, and forfeitures update the cap table and the pool on the same record. The ledger produces the grantee summary, the board approval packet, and the diligence export from a single source.

See Cap Tables & FinancingCommon questions

Pool tracking, 409A linkage, vesting accrual, exercise mechanics, and a cap table that reflects the option layer without manual reconciliation.