How to value a private corporation

Valuation in a private corporation is a triangulation across methods, not a calculation with a single right answer. The goal is a defensible range that founders and investors can negotiate within. For pre-revenue corporations, valuation is largely comparable-driven and stage-based. For revenue-positive corporations, comparable multiples and DCF become more useful. This guide covers the methods and how to combine them.

| When | Pre-financing planning, at term sheet, for 409A purposes, for tax planning |

|---|---|

| Output | Defensible valuation range, not a single number |

| Inputs | Comparable transactions, sector multiples, financial projections, market signals |

| Audience | Investors (priced rounds), tax authority (409A), buyers (M&A) |

- Pre-revenue valuations are largely comparable-driven; revenue-positive valuations use multiples and DCF

- Triangulate across at least 2-3 methods rather than relying on one

- Market signals (what investors are paying) dominate at the term-sheet stage

- 409A valuations have their own methodology and should not be conflated with negotiation valuations

- The valuation range is what matters; the single number is the negotiated outcome

On this page

Steps

Identify comparable transactions

Comparable transactions are the most-used input for private-corporation valuation. Identify 5-15 corporations that look similar to yours by sector, stage, revenue scale, growth rate, and geography. For each, find the latest financing round's valuation (PitchBook, Crunchbase, CB Insights, public reports). Adjust for the corporation's specific advantages or disadvantages. The result is a range of comparable valuations that bracket what the market is currently paying for similar corporations.Apply sector multiples for revenue-positive corporations

If the corporation has meaningful revenue, sector multiples become useful. ARR multiples for SaaS (varies widely; current market is 5-15x for growth SaaS, 2-5x for slower-growth or mid-market). Revenue multiples for marketplaces, fintech, healthcare each have their own ranges. The multiples are sector and stage dependent; published quarterly by firms like SaaS Capital, Bessemer, etc. Apply the relevant multiple to ARR or revenue, adjust for growth rate (faster growth merits higher multiple).Use cost-to-replicate for pre-revenue benchmarking

Cost-to-replicate is a sanity check, not a primary method. Compute: how much would it cost a well-funded competitor to replicate what the corporation has built? The output is a floor on valuation (the corporation should be worth at least its replacement cost, otherwise it's better to be the competitor). For pre-revenue corporations, this can validate that the valuation range is above the simple cost-to-build benchmark.Run DCF for revenue-positive, predictable corporations

Discounted cash flow becomes useful for corporations with predictable revenue and reasonable visibility into future cash flows (5+ years). Build a 5-10 year financial projection, calculate free cash flow each year, discount back to present at an appropriate rate (15-25% for venture-stage; lower for later-stage). Sum the discounted cash flows plus a terminal value to get the DCF valuation. DCF is highly sensitive to assumptions; the range from optimistic to pessimistic assumptions is often wide.Triangulate to a defensible range

Take the outputs from each method and overlay them. The intersection of the ranges is the defensible valuation zone. Typical pattern: comparables give a wide range, sector multiples narrow it, DCF (if applicable) provides a check. The single negotiation valuation is then chosen within the defensible zone based on competitive dynamics (multiple term sheets), founder ownership goals, and round size.Distinguish from 409A for tax purposes

The 409A valuation (used for option strike prices) is a separate exercise with its own methodology, typically done by an independent third party. The 409A valuation is usually lower than the negotiated round valuation because it applies a marketability and minority discount. A $50M post-money Series A might have a 409A FMV of $0.50/share for common stock when the preferred is priced at $2.00/share. Don't conflate the two; investors will not accept your 409A as the negotiation valuation, and the tax authority will not accept your negotiation valuation as 409A FMV.

Common mistakes

- Reverse-engineering valuation from dilution targets. Founder wants to own 60% after the round. Round size is $5M. Founder calculates: $5M / 40% = $12.5M post-money. This is dilution-driven, not value-driven. Investors don't pay valuations based on what the founders want to own; they pay based on what the market signals. A dilution-driven number that doesn't track to comparable valuations is harder to defend.

- Using the latest funding round of one comparable as the benchmark. One similar corporation just raised at $80M post-money. The founder targets $80M as their benchmark. But that corporation has 3x the revenue, 2x the growth rate, and a different sector dynamic. Using a single comparable is unreliable; the range across 8-12 comparables is more defensible.

- Ignoring stage signal in the multiple. A growth-stage SaaS comparable has a 12x ARR multiple. The founder applies it to their early-stage corporation. But early-stage SaaS multiples are typically much lower because of the higher risk. Multiples should be matched to stage as well as sector.

- Confusing 409A with negotiation valuation. Investor asks for the corporation's last 409A. The founder hands over the 409A valuation expecting it to be the basis for the round. The investor laughs because 409A is a tax-purposes number with a heavy minority/marketability discount. Treat 409A and negotiation valuations as parallel artifacts, not substitutes.

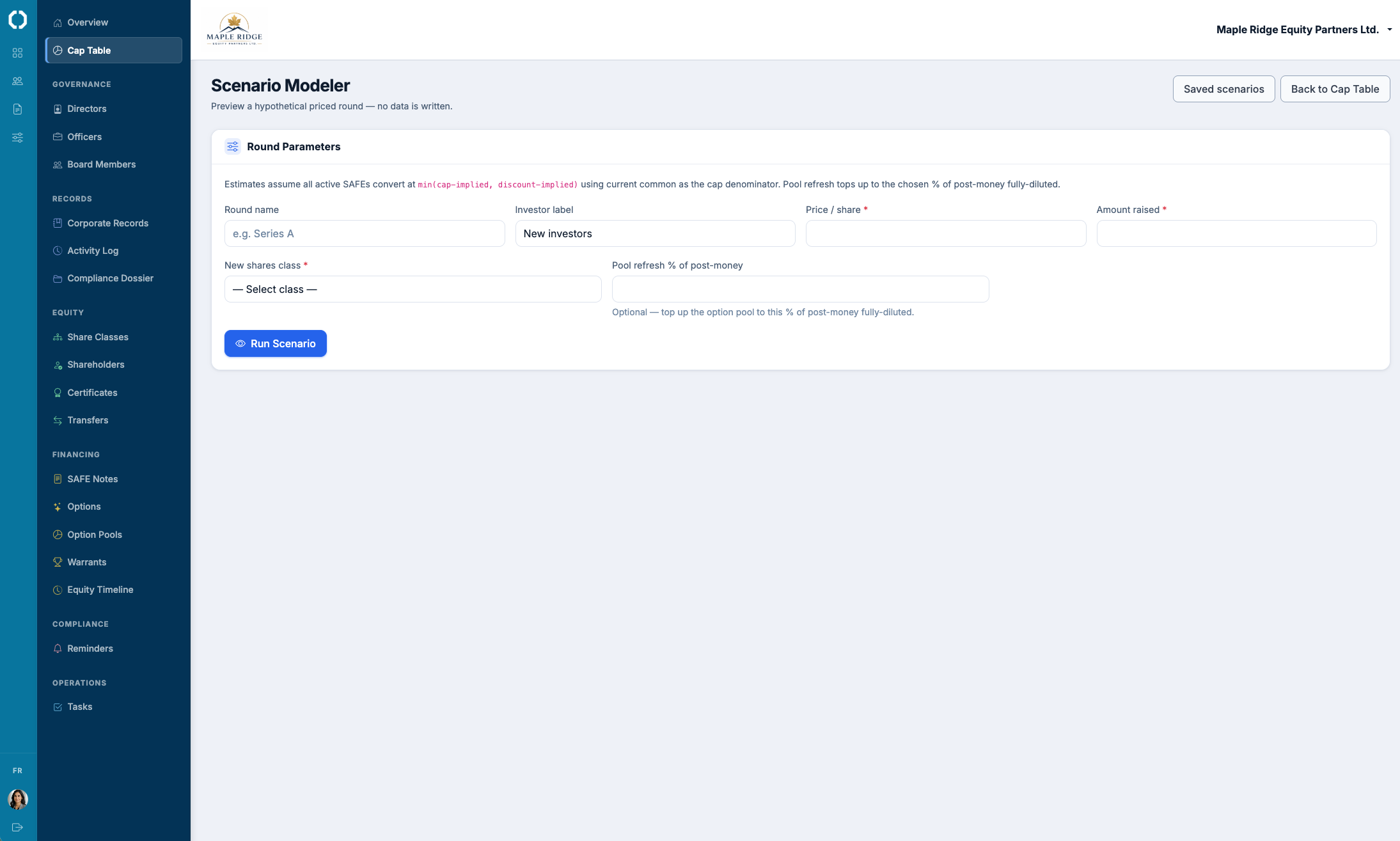

Octelligence's cap-table modeling supports priced-round scenarios with valuation inputs, option pool top-ups, and SAFE conversions all in one place. The valuation modeling output ties to the share register, so closing on the negotiated number is mechanical.

See Cap Tables & FinancingCommon questions

Pre-money pool top-up, SAFE conversion, and per-share price all computed off the live share register. The valuation maps to the math.