SAFE notes for Canadian startups

The SAFE became the default way early-stage startups raise their first money, fast, cheap, and standardized. It was also written for Delaware, which leaves Canadian founders with good questions: does it work here, how is it taxed, and what happens to my ownership when it converts? This guide explains what a SAFE is, how it differs from a convertible note, how caps and discounts and conversion actually work, the specific wrinkles that apply in Canada, and how to keep SAFEs straight in your corporate records and cap table.

| What | A contractual right to future shares, no interest, no maturity |

|---|---|

| Origin | Y Combinator, 2013; post-money version 2018 |

| Converts | At the next priced round, per the cap and/or discount |

| Canada | Fits a prospectus exemption; tax treatment less settled than US |

- A SAFE is a right to future shares: no interest, no maturity, not debt and not yet equity

- It converts at the next priced round, at the better of the valuation cap or the discount

- Post-money SAFEs fix the investor's percentage and put later dilution on the founder

- In Canada a SAFE still has to fit a securities exemption, and its tax treatment is less settled than in the US

- A SAFE sits off the share register but must be modelled on the cap table from day one

On this page

What a SAFE is

A SAFE, short for Simple Agreement for Future Equity, is a short contract in which an investor gives a startup money now in exchange for the right to receive shares later, when the company raises a priced round. Y Combinator introduced it in 2013 to replace the convertible note as a faster, cheaper instrument for the earliest money. There is no interest and no maturity date: the investor is betting on the company, not lending to it. The SAFE simply waits until a triggering event, almost always the next equity financing, and then converts into shares on agreed terms. For the formal definition see the glossary entry on the post-money SAFE.

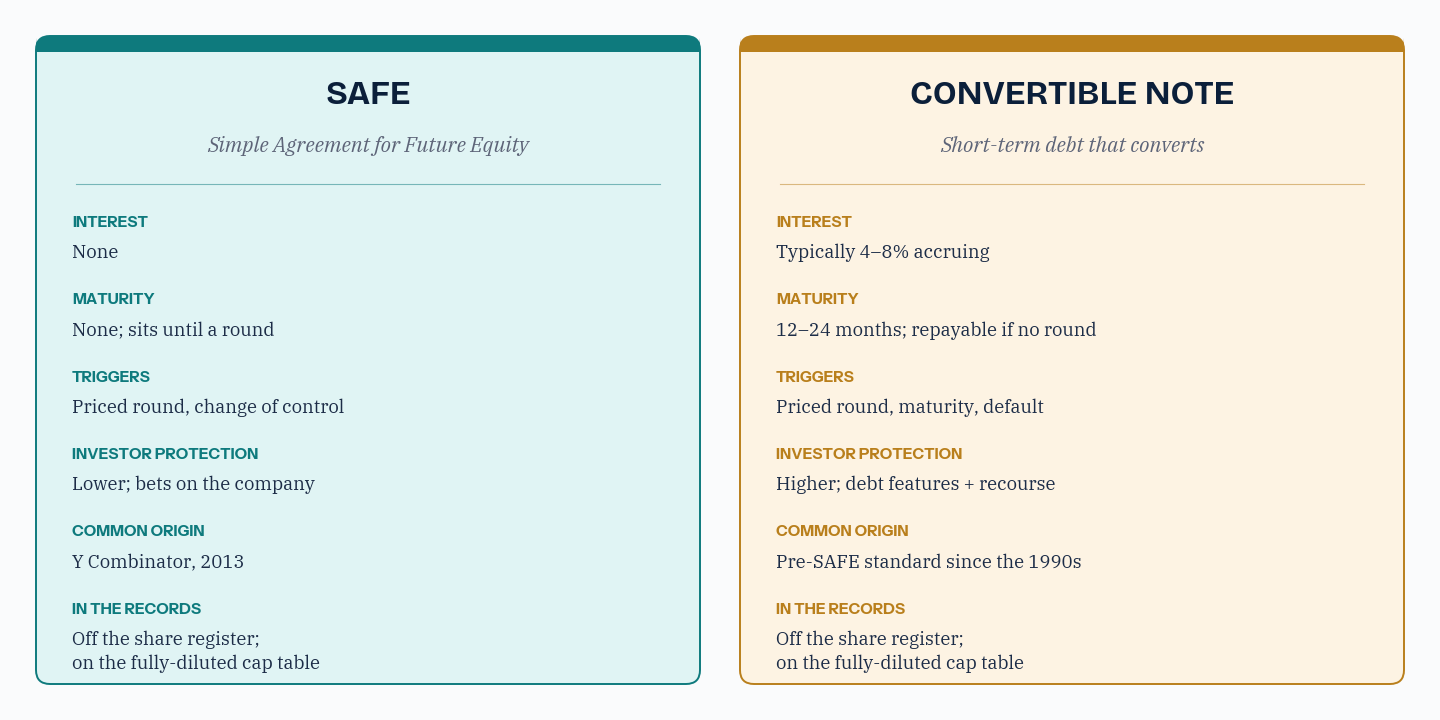

SAFE versus convertible note

The SAFE's closest relative is the convertible note, and the difference matters. A convertible note is debt: it carries an interest rate and a maturity date, and if the company has not raised by maturity, the note is technically repayable, which gives the investor leverage and the founder a deadline. A SAFE strips both features out. No interest accrues, and there is no maturity, so a SAFE can sit on the cap table indefinitely until a round triggers it. That makes the SAFE simpler and friendlier to founders, at the cost of giving the investor less protection. Many Canadian angels and some funds still prefer convertible notes precisely because the debt features give them recourse, so founders should expect to see both.

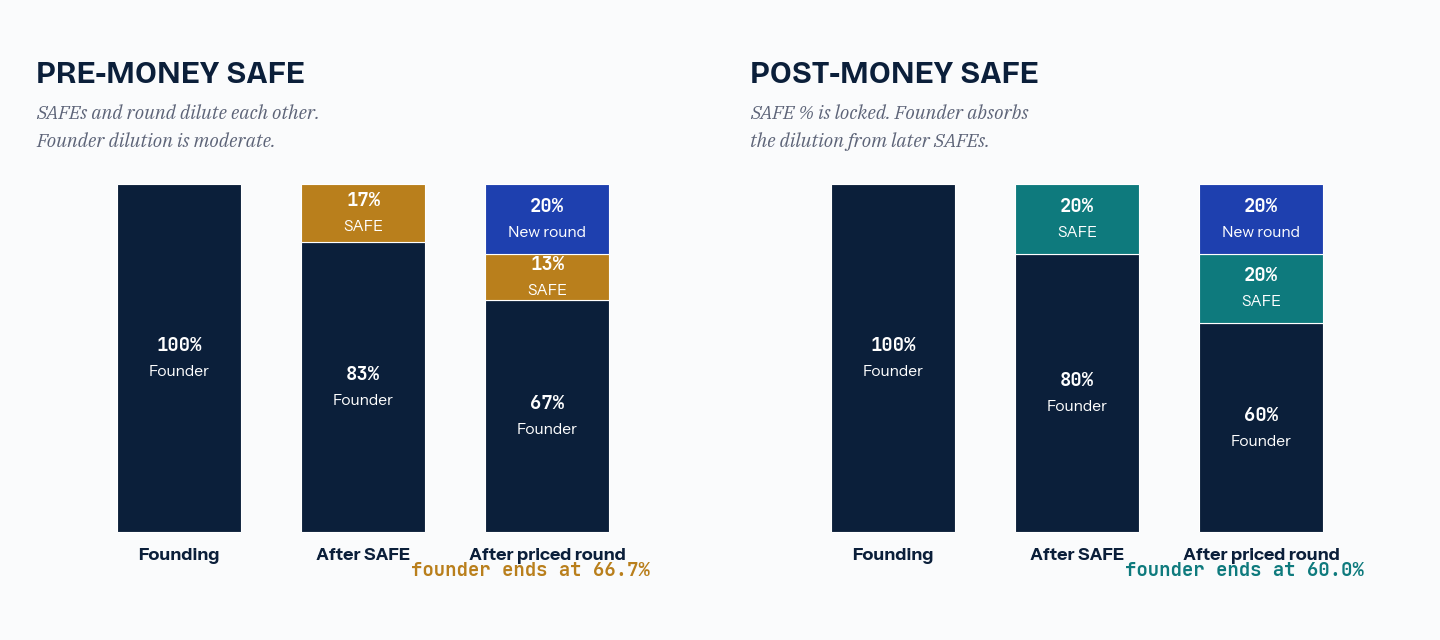

Pre-money versus post-money

There are two generations of SAFE, and confusing them is a common and expensive mistake. The original 2013 pre-money SAFE calculated the investor's ownership based on the valuation before the new money came in, which meant that when several SAFEs and the new round all landed together, they diluted each other in ways that were hard to predict. In 2018 Y Combinator released the post-money SAFE, which fixes the investor's ownership as a percentage of the post-money capitalization, measured after all the SAFEs convert but before the new priced-round money. The post-money SAFE is now the market standard. Its virtue is predictability: each investor knows their percentage. Its catch is that the dilution from every additional SAFE falls on the founders, not on the earlier SAFE holders, so stacking post-money SAFEs erodes founder ownership faster than many expect.

Valuation cap and discount

A SAFE rewards early money through two levers. The valuation cap sets a maximum company valuation at which the SAFE converts, so if the priced round happens at a higher valuation, the SAFE holder still converts at the lower capped price and gets more shares for their money. The discount rate gives the holder a percentage discount to the round price, commonly 10 to 20 percent. A SAFE may have a cap, a discount, both, or neither. When it has both, it converts at whichever produces the better price for the investor, which is almost always the cap in a round that has gone well. Some SAFEs also carry a most-favoured-nation clause, letting an early investor adopt better terms offered to a later one.

How a SAFE converts

Conversion happens at the priced equity financing. The mechanics: the company prices its round, the SAFE's conversion price is computed from its cap and discount, and the SAFE's investment amount is divided by that conversion price to produce the number of shares the holder receives. Those shares are then actually issued, which is the moment the SAFE stops being a contract and becomes equity on the register. With one SAFE the arithmetic is simple; with several SAFEs at different caps and discounts converting at once, alongside the new money and often an option-pool top-up, it becomes the kind of calculation that is easy to get wrong by hand. Our procedure for converting a SAFE walks the steps, and the free SAFE conversion simulator and multi-SAFE batch simulator model the result before you commit.

Dilution and the cap table

The single most important habit with SAFEs is to treat them as real ownership from the day they are signed, even though no shares exist yet. A SAFE is not on the share register, but it represents shares that will be issued, and those shares belong on the fully-diluted cap table. Founders who track only issued shares feel rich until the priced round, when a stack of post-money SAFEs and a fresh option pool convert at once and their percentage drops sharply. Model it forward instead: the cap table dilution calculator and the option pool planner show where you actually land, and the guides on modelling founder dilution and raising on SAFEs cover the playbook.

The Canadian wrinkles

The SAFE was written for Delaware, and three things deserve a Canadian founder's attention.

- Securities law. Issuing a SAFE is distributing a security, so it has to fit a prospectus exemption under Canadian securities rules, most often the accredited investor exemption or the private issuer exemption. The US SAFE template references US securities law and should be adapted to the Canadian regime; this is light legal work, not a rewrite.

- Tax treatment. The tax characterization of a SAFE in Canada is less settled than in the US. Because a SAFE is not a share, holding-period analyses, including eligibility for the lifetime capital gains exemption on qualified small business corporation shares, generally run from the shares issued on conversion rather than from the SAFE's signing date. Get advice early, because the timing can matter a great deal at exit.

- Not a shareholder yet. A SAFE holder is not a shareholder until conversion, so they are not on the share register, do not vote, and are not counted in the significant-control analysis on the basis of the SAFE alone. That status flips at conversion, and the records have to flip with it.

None of these makes the SAFE unworkable in Canada; they just mean the document and the tax plan deserve a Canadian lens. For the broader records differences between the regimes, see Delaware vs Canadian corporate records.

Recording SAFEs in your records

Because a SAFE is not a share, founders often file it and forget it, which is how cap tables drift. The discipline is straightforward. Keep the signed SAFE and its subscription paperwork in the minute book, authorized by the board where required. Track the SAFE's amount, cap, discount, and date on the cap table as an outstanding convertible, not as issued shares. Then, at conversion, run the calculation, issue the shares, record them on the share register with their certificate and class, and file the conversion documents, so the SAFE that lived as a contract becomes a clean entry in the equity record. Our guide to corporate minute books covers where each of these documents belongs.

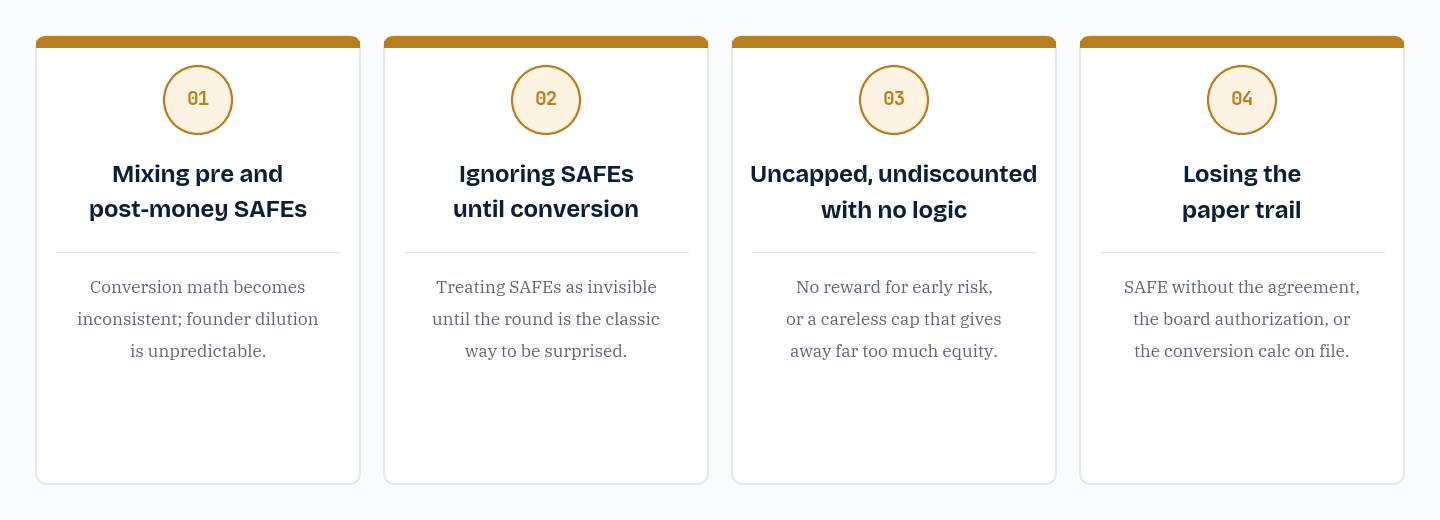

Common mistakes

- Mixing pre-money and post-money SAFEs. Raising on both generations at once makes the conversion math inconsistent and the founder's ownership unpredictable. Pick one, almost always post-money, and stay with it.

- Ignoring SAFEs until the round. Treating outstanding SAFEs as invisible until conversion is the classic way founders get surprised by their own dilution.

- Uncapped, undiscounted SAFEs with no logic. A SAFE with neither a cap nor a discount gives the early investor no reward for early risk, and one with a cap set carelessly can hand away far more of the company than intended.

- Losing the paper. A SAFE that converts without the signed agreement, the board authorization, and the conversion calculation on file is a diligence problem waiting at the next round.

Octelligence tracks every SAFE with its cap, discount, and date as a first-class instrument on the fully-diluted cap table, models the conversion before the round, and on conversion issues the shares, updates the share register, and files the documents in the minute book. The cap table and the records stay in sync from the first cheque to the priced round.

See Cap Tables & FinancingCommon questions

Keep SAFEs on the cap table from the first cheque, model the conversion before you price the round, and turn them into clean register entries when they convert.