Cap table management for startups

Every founder has a cap table, even the ones who think they do not. It might be three names in a spreadsheet, but the moment you issue founder shares, grant options, or take a SAFE, you are managing the record of who owns the company. Done well, the cap table is a single source of truth that makes financings and exits fast. Done casually, it drifts from the legal records and becomes the thing that slows or sinks a deal. This guide explains what a cap table is, what belongs on it, why the share register underneath it is the real source of truth, and how to keep it clean from incorporation to your first priced round.

| What | The record of who owns the company, on a fully-diluted basis |

|---|---|

| Built from | The share register, the legal source of truth |

| Includes | Shares, options and the pool, SAFEs, warrants, notes |

| Breaks when | Kept in a spreadsheet apart from the register |

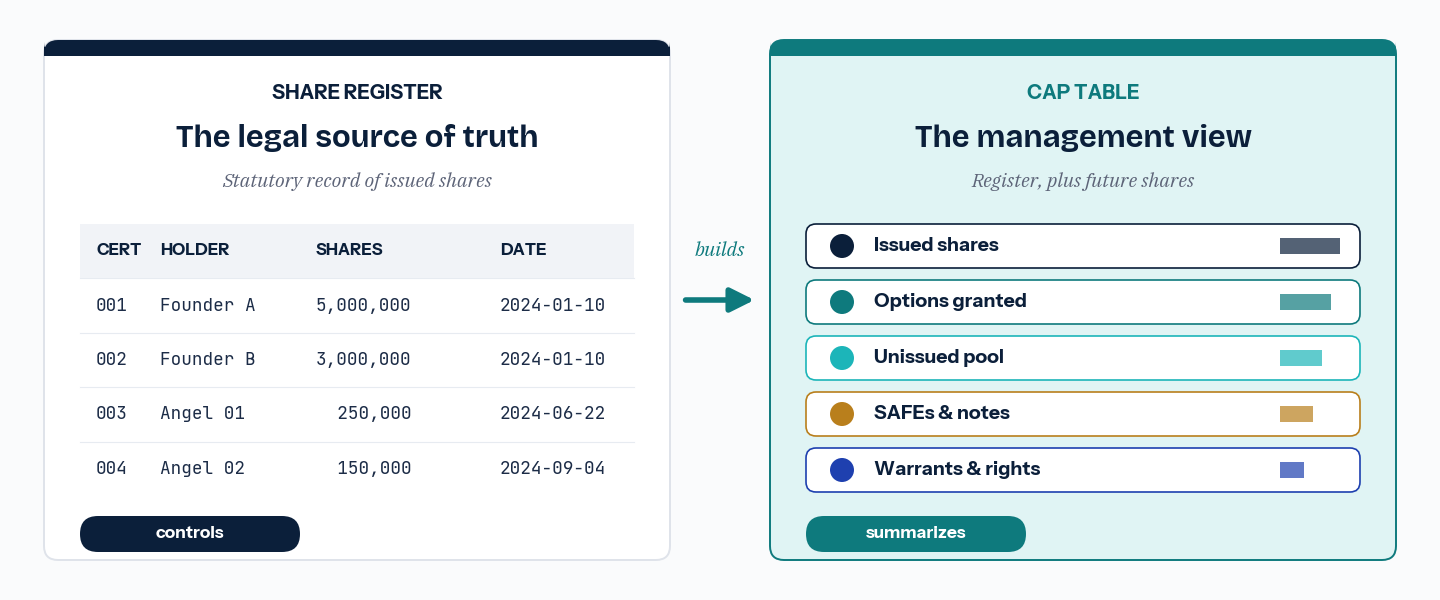

- The cap table is the management view of ownership; the share register is the legal source of truth

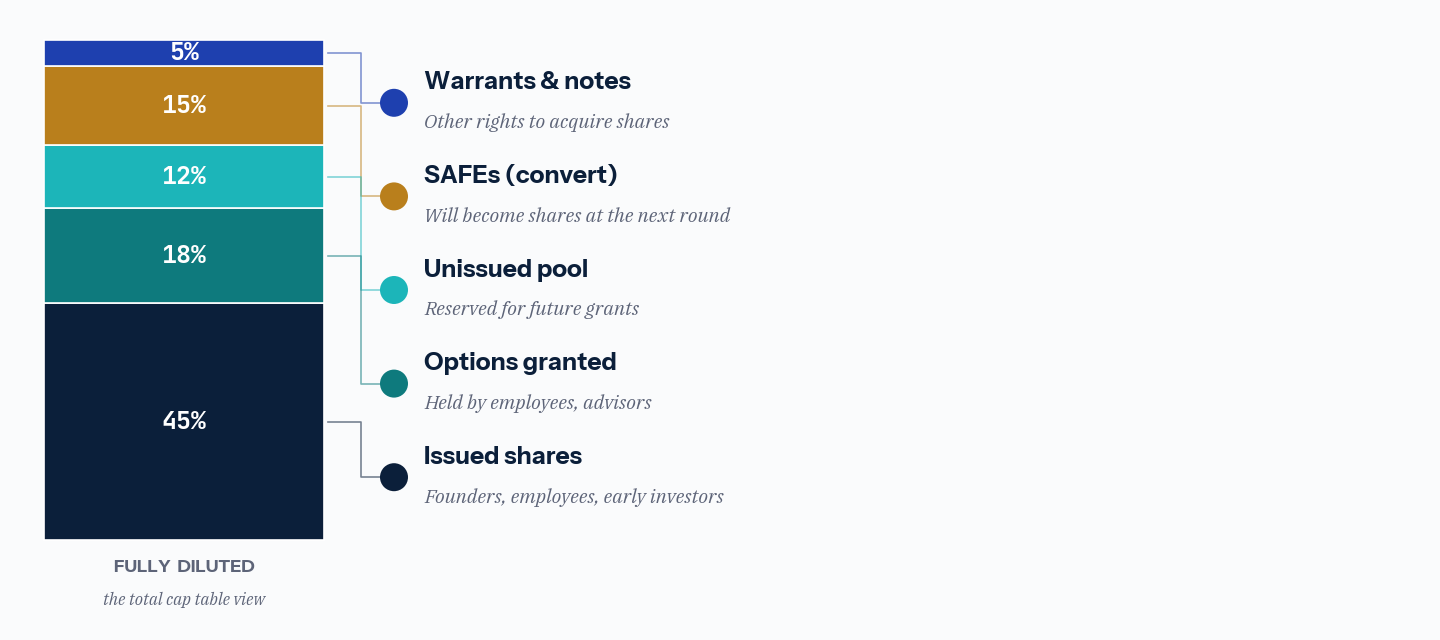

- A clean cap table is fully diluted: issued shares plus options, the pool, SAFEs, and notes

- Every issuance, transfer, grant, and conversion must trace back to an authorizing record

- Spreadsheets drift from the legal records, which is what diligence catches

- Build the cap table from the register, not in parallel with it

On this page

What a cap table is

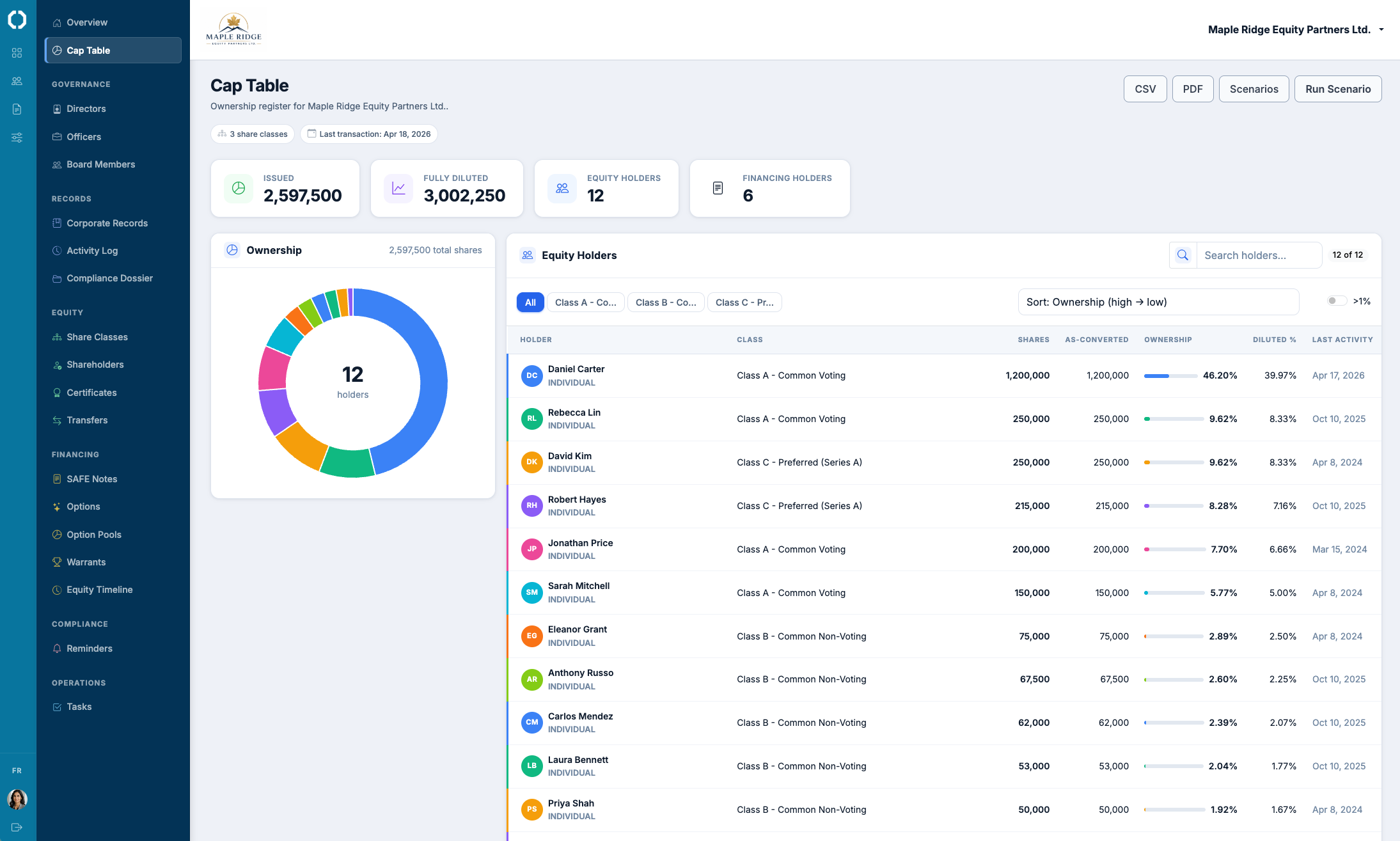

A capitalization table, or cap table, is the record of who owns the company and in what proportion. At its simplest it lists each holder, how many shares they hold, what class, and what percentage of the company that represents. As the company grows, it expands to capture everything that affects ownership: multiple share classes, stock options and the pool reserved for them, warrants, and convertible instruments like SAFEs and notes. The cap table is how a founder answers the most basic question about the business, who owns it, and it is the first document an investor or acquirer asks to see. The formal definition is in the glossary entry for the cap table.

What belongs on a cap table

A complete cap table accounts for every claim on the company's equity, issued or not.

- Issued shares by holder and class, the foundation, drawn from the share register.

- Stock options, both granted (held by employees and advisors) and the unissued option pool reserved for future grants.

- Convertible instruments: SAFEs and convertible notes that will become shares at a future round.

- Warrants and any other right to acquire shares.

The most useful single number the cap table produces is the fully-diluted total: the share count as if every option, pool reservation, and convertible had turned into shares. Founders who look only at issued shares consistently overestimate how much of the company they own, because the dilution waiting in the pool and the SAFEs has not landed yet.

The register is the source of truth

The cap table is a summary, not the legal record. The legal record is the share register in the corporation's minute book, which lists issued shares by holder, class, and certificate number, and every issuance and transfer that produced them. The cap table is built from that register and then extended with the not-yet-shares. This ordering matters: when the cap table and the register disagree, the register controls, because it is the statutory record backed by board resolutions and certificates. A cap table maintained in parallel with the register, rather than derived from it, is the root cause of almost every ownership dispute and diligence problem. Keeping the share register current and building the cap table from it is the whole discipline. The relationship between the two records is covered further in our guide to corporate minute books.

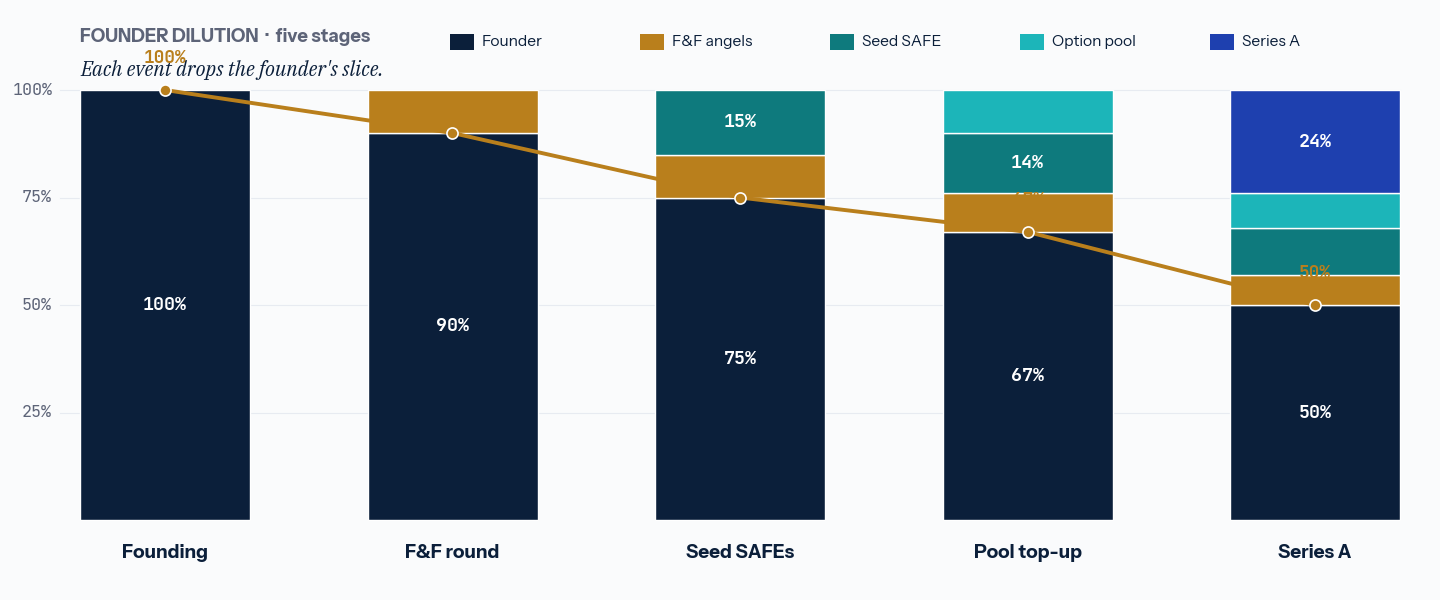

Dilution and how rounds change ownership

Dilution is what happens to existing owners when the company issues new shares: each existing holder owns the same number of shares but a smaller slice of a larger whole. It is not inherently bad, raising money at a higher valuation can leave a founder with a smaller percentage of a much more valuable company, but it has to be understood and modelled, not discovered. The events that dilute are a priced round, an option-pool top-up, and the conversion of SAFEs and notes, and they often happen together, which is what makes the arithmetic surprising. Model it before you sign: the cap table dilution calculator shows where each holder lands, and the guides on modelling founder dilution and running a priced round cover the mechanics.

The option pool

The option pool is the block of shares a company reserves to grant to employees and advisors. It sits on the cap table as reserved-but-unissued, and it dilutes like any other equity, which is why investors care exactly when and how it is sized. Investors typically require the pool to be created or topped up before their money goes in, so that the dilution from the pool falls on existing holders rather than on the new investor. That single convention has a large effect on founder ownership, and it is the part of a term sheet founders most often misjudge. Size it deliberately with the option pool planner and the guide on planning an option pool, and record each grant properly as covered in granting stock options.

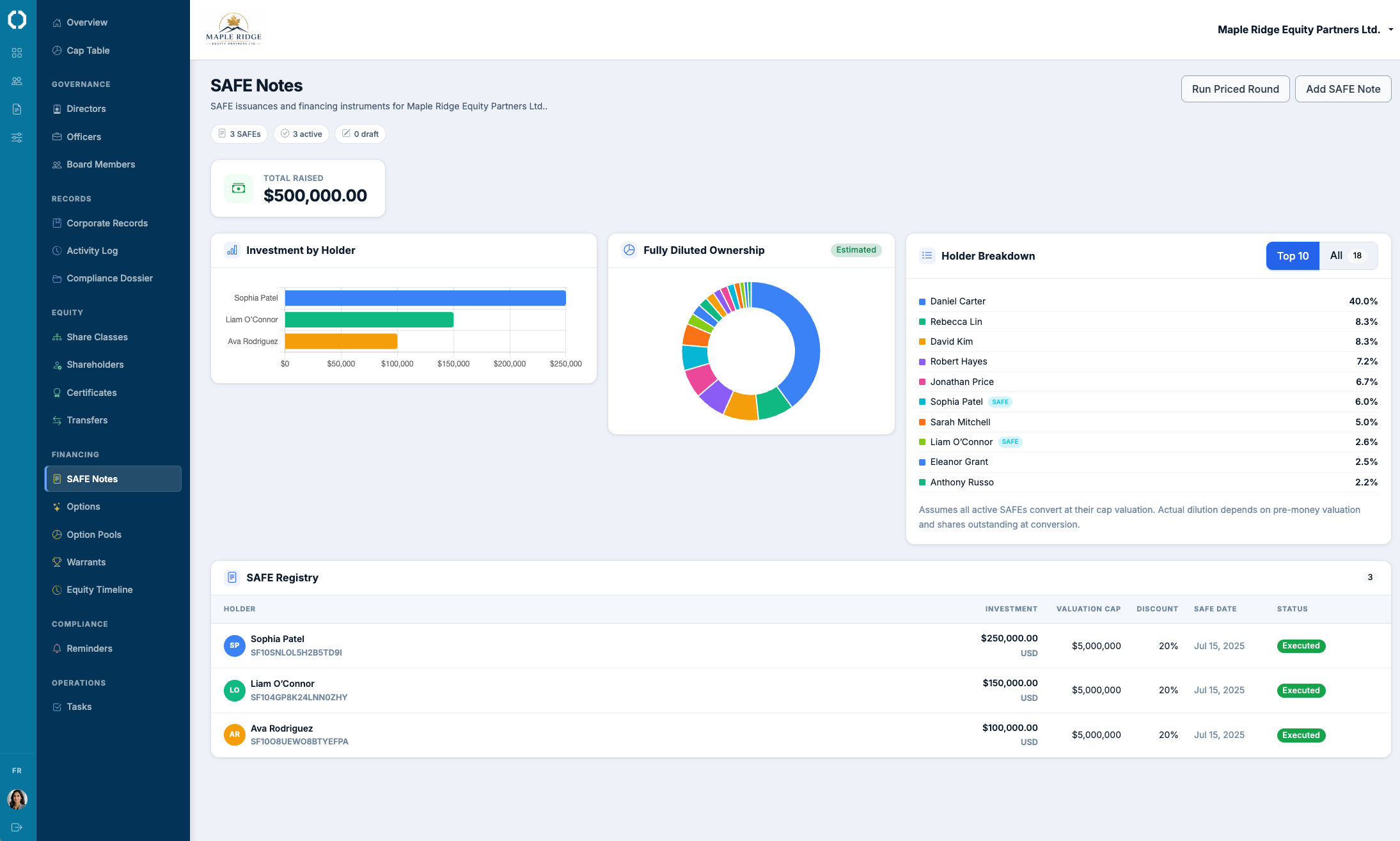

SAFEs and convertibles

SAFEs and convertible notes are money today in exchange for shares later, and they live on the cap table as future shares from the moment they are signed, even though no shares exist yet. The mistake founders make is treating them as invisible until conversion, then being surprised when a stack of SAFEs converts at the priced round and their percentage drops. Track each one by its amount, valuation cap, and discount, and model the conversion before the round so there are no surprises. The SAFE conversion simulator models the outcome, and our full SAFE notes guide for Canadian startups covers how they work and convert. When the round closes, the SAFE becomes issued shares on the register, and the cap table and the legal record line up again. The same modelling applies to liquidation preferences on preferred shares, which the liquidation preference waterfall tool lays out.

The cap table in diligence

In a financing or acquisition, the cap table is checked against the legal records line by line. The reviewer confirms that every share on the cap table traces to an authorizing board resolution, a subscription, and a register entry; that every option was granted under a board-approved plan; and that the SAFEs and notes are accounted for and convert as modelled. The cap table that reconciles cleanly to the share register and the minute book closes the round; the one that was kept in a spreadsheet and no longer matches the legal records turns into a remediation project at the worst possible time. Our guide on preparing for due diligence covers what reviewers pull and in what order.

Spreadsheet versus system

Almost every cap table starts in a spreadsheet, and for the first handful of entries that is fine. The spreadsheet stops being fine when issuances, transfers, option grants, and SAFEs start happening in parallel with the legal records, because the spreadsheet is a copy, and copies drift. The failure is rarely a math error; it is that the spreadsheet and the corporate records tell different stories, and no one can say which is right. A cap table system solves this by deriving the cap table from the same register and resolutions that are the legal record, so there is one source of truth rather than two that disagree. If you are comparing options, our Carta and Pulley comparisons cover the landscape, and the difference that matters most is whether the cap table is tied to the corporate records or floats beside them.

Keeping it clean

The habits that keep a cap table trustworthy are unglamorous and decisive. Record every issuance and transfer on the register on the date it happens, with its authorizing resolution and certificate. Build the cap table from the register, never in parallel. Put every option, pool reservation, SAFE, and note on the fully-diluted view the day it exists. Model dilution before each round rather than reconstructing it after. And reconcile the cap table to the register and the certificates on a regular cadence so drift is caught in weeks, not discovered in diligence. Do those things and the cap table stops being a source of anxiety and becomes what it should be: the clear, current answer to who owns the company.

Octelligence builds the fully-diluted cap table from the live share register, so issued shares, options, the pool, SAFEs, and warrants all reconcile to the legal record and the certificates. Model priced rounds and SAFE conversions before you sign, and produce a diligence-ready cap table and corporate record as one indexed export.

See Cap Tables & FinancingCommon questions

Build the fully-diluted cap table from your live share register, model rounds and conversions before you sign, and export a diligence-ready record in one click.